Global| Oct 05 2007

Global| Oct 05 2007Euro-Area Banks Tighten Lending Policies, According to Latest ECB Survey

Summary

For the last 5 years, the European Central Bank (ECB) has conducted a quarterly survey of senior bank lending officers at a representative sample of European banking institutions. Ordinarily, the survey takes place during the first [...]

For the last 5 years, the European Central Bank (ECB) has conducted a quarterly survey of senior bank lending officers at a representative sample of European banking institutions. Ordinarily, the survey takes place during the first month of each quarter with reference to the prior quarter ("past 3 months") and the outlook for the current quarter ("next 3 months"). This time, however, the survey was advanced by a month to gain an earlier reading on the impact of the recent turmoil in world credit markets. The results do suggest that this situation has indeed had an impact.

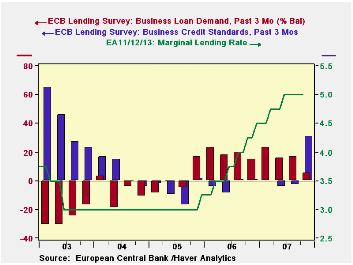

Banks reported a sharp turn in lending policy toward businesses. They had been in a trend of gentle easing of credit standards since the middle of 2004, with readings in most quarters ranging from 0 to -10, where negative numbers indicate that more banks are easing than tightening up on lending practices and credit availability. In July, this measure was -3 but in this survey, just two months later (late September), it was +31 as many more banks shifted toward lending restraints on business customers. Details show this move was more potent for large companies (-1 to +33) as against small and medium-size firms (-7 to +15). It also hit long-term loans (-4 to +30) over short-term (-2 to +16). The survey also inquires about banks' expectations for their strategy in the coming three months; they look for about the same degree of tightening during Q4, at +28.

Businesses' demand for loans continued to expand in the latest survey, but at fewer banks than before. The demand reading was +17 in the July survey and averaged +19 in 2006. This latest figure is just +5, although bankers look for +11 in coming months.

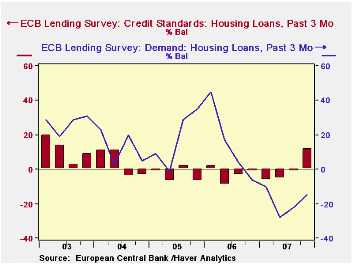

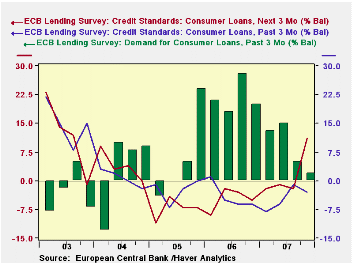

Trends on loans to households differ. Banks report that they have tightened somewhat on home purchase lending, from a -1 rating in July to +12 in September; they expect slight further firming on credit conditions in the next few months, to +15. In contrast, they continued easing up on consumer credit and other loans, from -1 before to -3 most recently. They do, though, expect to tighten noticeably during Q4, to +11.

The bankers say that household loan demand is fairly weak, but this is also not a recent development. Demand for home purchase loans has been shrinking since Q4 2006, and in the latest two quarters has actually become somewhat less negative. The worst reading was April's -28, with a relative improvement to -22 in July and -15 in this latest survey. More weakening is anticipated, though, to -29 in the next 3 months. Other household lending has shown marginal gains in these last two quarters, although much less than earlier, as highlighted in the graph. A tiny net reduction is expected for the remainder of the year.

This survey shows significant alterations in credit policies, then, in the very most recent months, along with slowing credit demands. These new trends are mostly expected to continue. The main intended use for this survey is a source of information for the ECB policymakers, and these results would seem to describe that lending institutions themselves are tightening credit, even without any further rate change by the ECB since June.

| ECB Lending Survey, Net %-ages | Next 3 Months, Oct 2007 | Past 3 Months | |||||

|---|---|---|---|---|---|---|---|

| Oct 2007 | July 2007 | 2006 | 2005 | 2004 | 2003 | ||

| Credit Standards: + = Tighten, - = Ease | |||||||

| Business Loans | 28 | 31 | -3 | -3 | -7 | 7 | 40 |

| Housing Loans | 15 | 12 | -1 | -3 | -3 | 4 | 12 |

| Consumer Credit | 11 | -3 | -1 | -4 | -3 | 1 | 15 |

| Loan Demand | |||||||

| Business Loans | 11 | 5 | 17 | 19 | 1 | -8 | -26 |

| Housing Loans | -29 | -15 | -22 | 15 | 18 | 13 | 27 |

| Consumer Credit | -1 | 2 | 5 | 22 | 6 | 4 | -3 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates