Global| Nov 21 2016

Global| Nov 21 2016CFNAI Diffusion Index Weakens in October

Summary

The CFNAI Diffusion Index weakened in October, declining to -0.35 from September's -0.16, according to the Federal Reserve Bank of Chicago. The components of the index all show weakness relative to trend except for the employment [...]

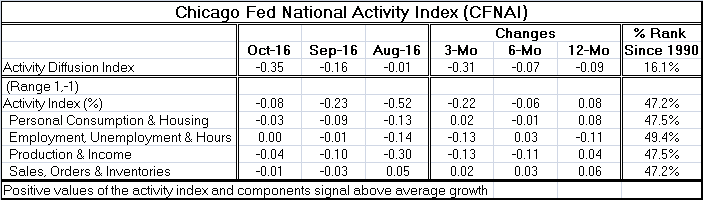

The CFNAI Diffusion Index weakened in October, declining to -0.35 from September's -0.16, according to the Federal Reserve Bank of Chicago. The components of the index all show weakness relative to trend except for the employment complex where the reading is neutral (pointing to trend growth). The index and all components were negative in September and all but one (sales orders and inventories) were negative in August as well.

The CFNAI Diffusion Index weakened in October, declining to -0.35 from September's -0.16, according to the Federal Reserve Bank of Chicago. The components of the index all show weakness relative to trend except for the employment complex where the reading is neutral (pointing to trend growth). The index and all components were negative in September and all but one (sales orders and inventories) were negative in August as well.

Over three months, there is deterioration in the diffusion index and its activity reading as well as for three of the four components. Over three months, the consumption/housing complex has improved slightly as have sales/orders/inventories. Over six months, there are declines in the diffusion index, the activity index and in two of four of the components. The consumption/housing complex indicates weakening along with production/income. Strengthening slightly is the employment complex and sales/orders/inventories. Over 12 months, the overall diffusion index is weaker, but the weighed activity index change is positive signaling improving growth. Only one component (the employment complex) signals weakening growth compared to 12-months ago.

Furthermore, I rank each of the indices over all values since January 1990. On this basis, all indices are below their median scores for that period (median occurs at diffusion rank =50). The employment complex stands in its 49th percentile, just short of its average reading on that period - remember that in October the employment complex index indicates trend growth. Still, the October reading is slightly below the median since 1990. The other sectors as well as the activity index show a standing in the 47th percentile of their historic ranges since 1990. These indices already are normalized to center on average growth. So this ranking index does not add as much explanatory power as it does with some other data analysis. Still, the point here is that however long the period that the average growth statistics are drawn from, compared to conditions since 1990, all sectors lag that average and the diffusion index is especially weak, in the lower 16 percentile of its historic queue of data.

The CFNAI is based on some 85 underlying indicators. As such its message is a powerfully broad one as each of these indicators is assessed relative to its average performance. Meanwhile, Fed officials seem determined to hike rates by yearend...once again. Once again they seem to have put the cart before the horse and decided through which rose-colored glasses they would be vetting the data in order to come to the conclusion that has already been decided. It's not really the ideal way to make policy, but here we are a year later and the Fed is still doing things backwards. Decision first, data second... No preset course of action...right. The CFNAI tells us what I have been saying by looking at a host of other data for some time. The economy (most sectors) is below average and momentum is fading; yet, the Fed sees conditions right to hike rates. Let me add that all inflation metrics are below target and the acceleration of inflation has stopped or slowed and OPEC is having a hard time cobbling together a coalition to support or to advance oil prices. Sounds like a real inflation risk environment to me, how about to you?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates