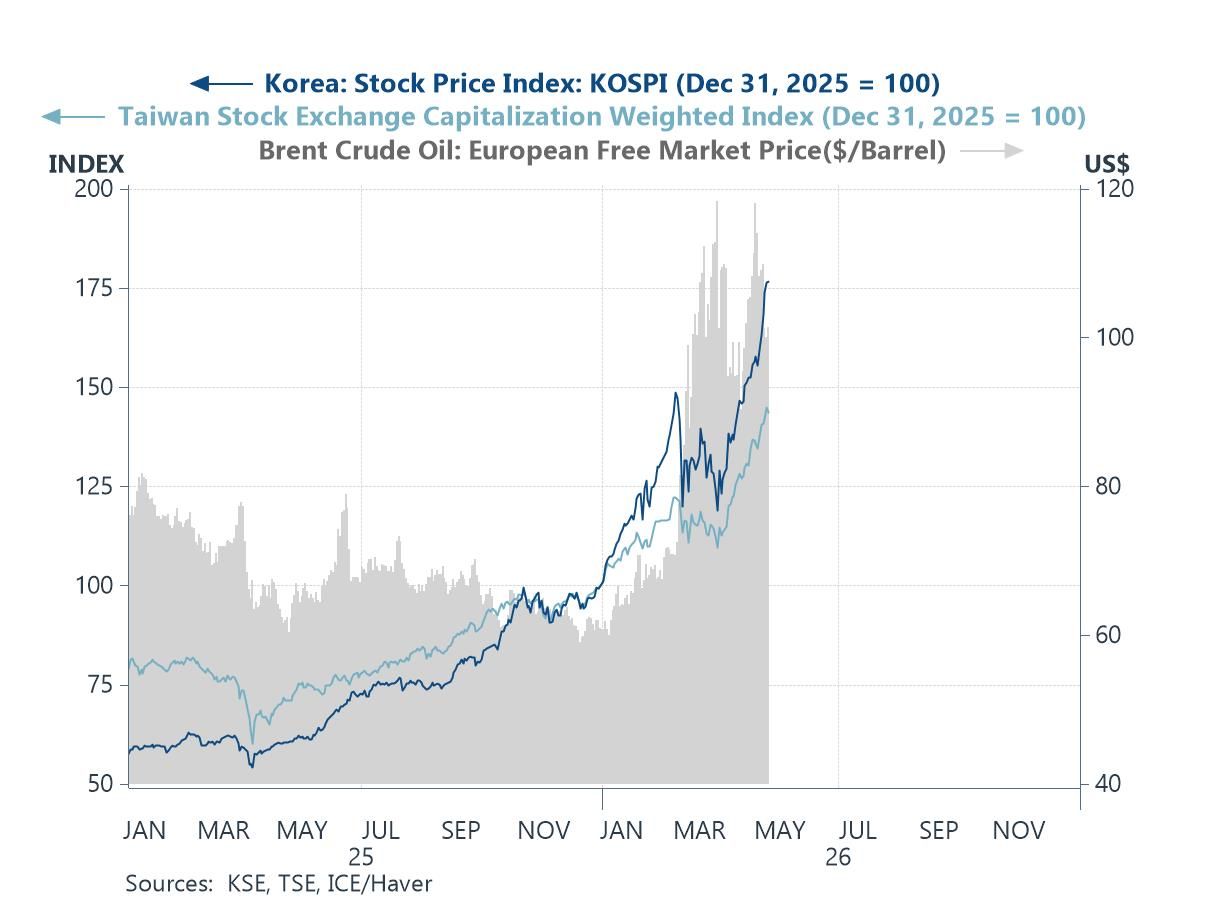

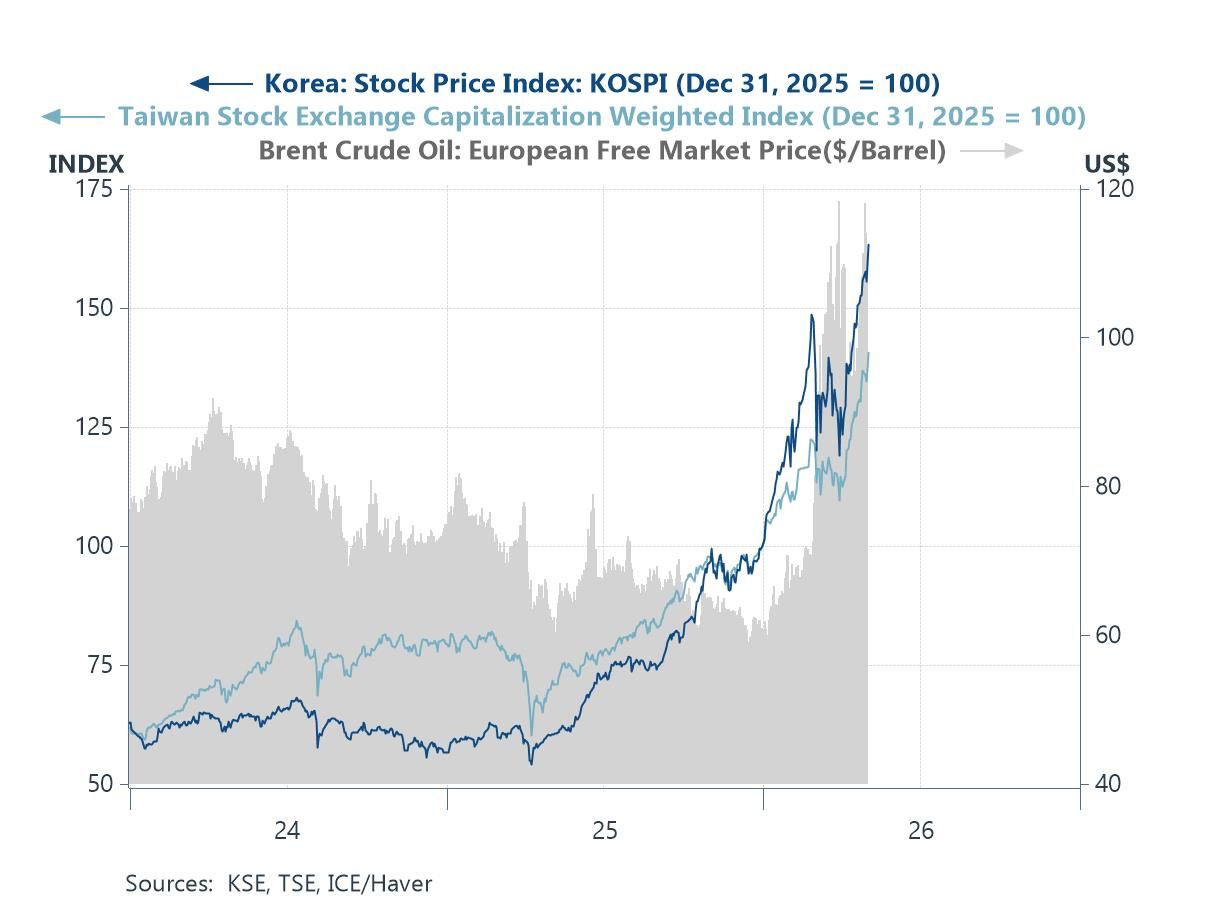

Asia

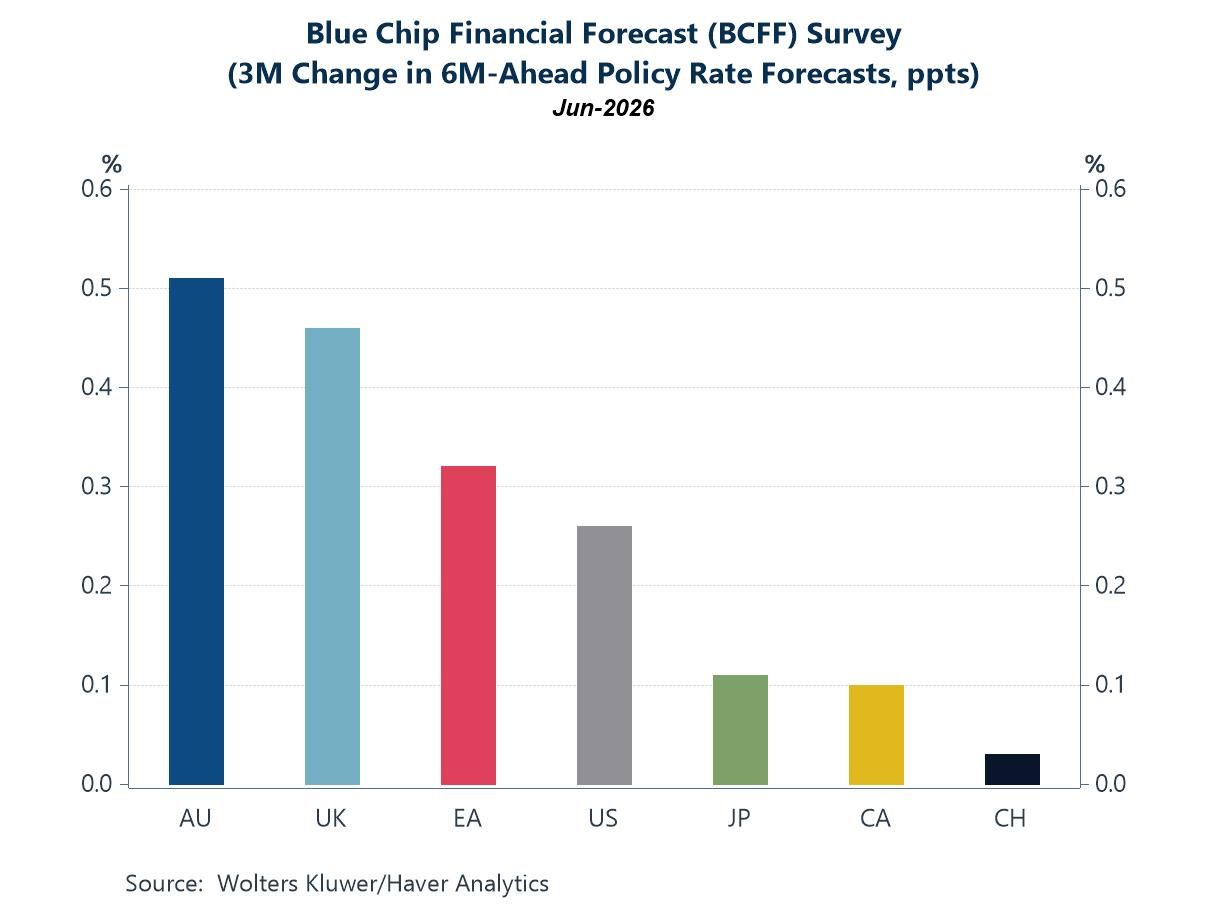

AsiaIn this week's Letter, we dive into the latest Blue Chip Financial Forecast (BCFF) survey results in light of key developments around Asia and the broader world economy. We find that, despite the recent flare-up in US-Iran tensions, panellist expectations for policy rates remain little changed, bar the US (chart 1). Central banks are still seen as likely to continue diverging significantly across regions in response to the volatility in global oil prices (chart 2). The latest on the US-Iran conflict brings hopes of another deal on the horizon, as part of a broad on-again, off-again pattern. Those hopes have sent crude oil prices lower, albeit with flows through the Strait of Hormuz remaining at a trickle (chart 3). As global oil supply remains constrained, one key area to watch is Chinese crude oil imports (chart 4), which have slumped since the conflict broke out. There is no telling when Chinese buying will recover, if ever, and if so, by how much. Moving to Japan, and taking these developments into account, the Bank of Japan held its policy rate steady at its recent meeting. Inflation risk is still flagged as being tied to the upside (chart 5). That may threaten to upend real wage gains this year, should a price flare-up materialise extensively enough. Yen intervention talk has also returned to the fore, with the US and Japan confirming recent intervention moves. Both have signalled that more may come if needed, although the yen remains squarely within its longer-term weakening trend (chart 6).

Blue Chip Financial Forecasts Last week, we published the August 2026 Blue Chip Financial Forecast survey results. Despite the flurry of recent headline developments around the world, we found panellist expectations only modestly changed from last month. In particular, views of 12-month ahead policy rates were little changed or unchanged for every economy bar the US (chart 1). US expectations now point to slightly higher policy rates than a month ago. Among the economies covered by the survey, the highest expected 12-month ahead policy rates still relate to Australia, followed by the US and the UK. At the other end, the lowest expected rates relate to Japan and Switzerland. The slightly higher expected US policy rate may well incorporate, among other factors, the recent re-escalation in US-Iran tensions and the inclinations of new Fed Chair Warsh. We return to those tensions in a later section below.