Global| May 30 2017

Global| May 30 2017EMU Sentiment Drops As Sector and Country Trends Turn Mixed

Summary

The EMU sentiment index fell to 109.2 in May from 109.7 in April. The Industrial sector and construction sector held their readings steady month-to-month. The sector diffusion indexes saw consumer confidence pick up in May, rising to [...]

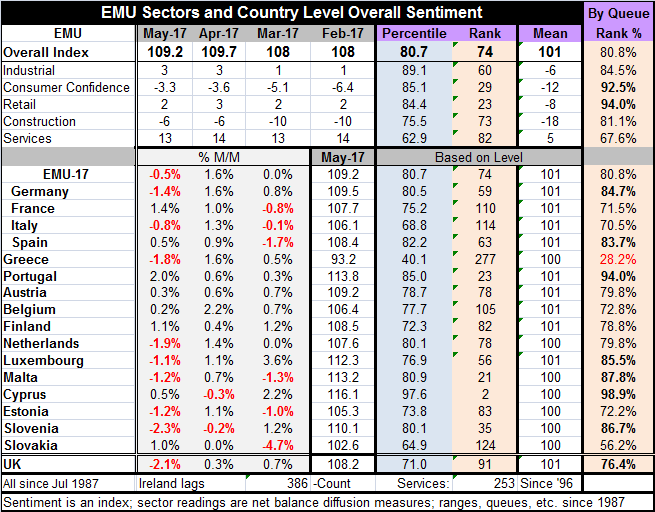

The EMU sentiment index fell to 109.2 in May from 109.7 in April. The Industrial sector and construction sector held their readings steady month-to-month. The sector diffusion indexes saw consumer confidence pick up in May, rising to -3.3 from April's -3.6. Retailing continued its slippage, dropping to 2 in May from 3 in April. Services are also weakened slightly, declining to a 13 reading in May from 14 in April.

The EMU sentiment index fell to 109.2 in May from 109.7 in April. The Industrial sector and construction sector held their readings steady month-to-month. The sector diffusion indexes saw consumer confidence pick up in May, rising to -3.3 from April's -3.6. Retailing continued its slippage, dropping to 2 in May from 3 in April. Services are also weakened slightly, declining to a 13 reading in May from 14 in April.

In addition to sectors convoluting in May, the country level data also turned scattershot. Eight of 16 reporting nations showed month-to-month drops in their respective sentiment gauges. This is after only two of them saw setbacks last month. The countries showing monthly drops in May include Germany and Italy, the first and third largest, respectively, economies in the EMU. All four of the largest economies have at least one sentiment drop in the last three months; Italy has two.

Still, the percentile standing of the country level sentiment gauges remains strong. Of these 16 reporters, seven have queue percentile standings in the top 20% of their historic queue of data or higher. Only Greece is below the 50% market that designates the median for each nation. After Greece, Slovakia at a 56.2 percentile standing, is the next weakest. The EMU may have slowed down a bit in May, but the metrics for the region as well as the various member states are uniformly good with only Greece as an exception.

Viewed by sector, the standings also are quite good. The overall sentiment gauge for the EMU has an 80th percentile standing. The industrial sector has an 84th percentile standing. Construction has an 81st percentile standing. Consumer confidence and the retail sector each have readings in their respective 90th percentiles; they have been stronger less than 10% of the time. The sector showing some relative weakness is services with a 67th percentile standing, still well above its median.

On balance, the EMU has been doing well. The surprise from yesterday may have been Mario Draghi's assertion that despite the improved performance the EMU still needs the assistance of a stimulative monetary policy. Of course, that will not make the Bundesbank happy. But Draghi seems to be plugged into the global economy and learning its lessons. There we find Japan with structural issues using lots of stimulus and still not able to bring forth inflation. More recently, the U.S. showed signs for turning higher and while growth is still clearly in gear the U.S. inflation progress has backtracked revealing oil as the likely driver of the upturn rather than any home-grown macroeconomic force. Moreover, EMU money growth has just slowed.

In the U.K., inflation is overshooting, but growth is slowing as Brexit is taking the wind out of its sales. Mark Carney's stimulus in the aftermath of the Brexit vote was appropriate and the inflation fallout out from the pound's drop is going to dissipate in a puddle of weaker economic growth. With growth weakening, Prime Minister Theresa May is losing her large lead as the elections approach.

In the U.S., the plan to hike rates is probably still intact for June, but beyond that the vision for Fed policy is unclear as U.S. data has slowed and inflation's uptrend has reversed. The Fed remains short of its target as does the ECB when oil is stripped away.

The bottom line may be that the rise in global growth is less than meets the eye. While there has been some revival in the last several months, the EMU is having its first setback in a while and certainly the first since optimism set in. The U.S. data have been showing weakness (less strength) for a bit longer. Meanwhile, as OPEC struggles to firm oil prices, inflation everywhere is taking a bit of a holiday and doing so while already on the tepid side of the ledger. No wonder Mr. Draghi wants to play it safe and wait for a clearer signal to endorse a policy switch.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief