Global| Sep 30 2019

Global| Sep 30 2019EMU Unemployment Rate at Its Lowest since 2008

Summary

The unemployment rate in the EMU has fallen in August and the ongoing drop speaks to the ongoing economic expansion- not withstanding concerns to the contrary. However, the chart reminds us that any rise in the unemployment rate is an [...]

The unemployment rate in the EMU has fallen in August and the ongoing drop speaks to the ongoing economic expansion- not withstanding concerns to the contrary. However, the chart reminds us that any rise in the unemployment rate is an event to be feared. Unemployment rates are the largest of battleships among economic data; they carry their momentum relentlessly and are difficult to turn. But having said that, once they begin to turn the process is also hard to reverse and the turning operation usually goes on to set a new trend. In this case, that would be a most unfavorable development, to higher unemployment rates and to the likely onset of recession.

The unemployment rate in the EMU has fallen in August and the ongoing drop speaks to the ongoing economic expansion- not withstanding concerns to the contrary. However, the chart reminds us that any rise in the unemployment rate is an event to be feared. Unemployment rates are the largest of battleships among economic data; they carry their momentum relentlessly and are difficult to turn. But having said that, once they begin to turn the process is also hard to reverse and the turning operation usually goes on to set a new trend. In this case, that would be a most unfavorable development, to higher unemployment rates and to the likely onset of recession.

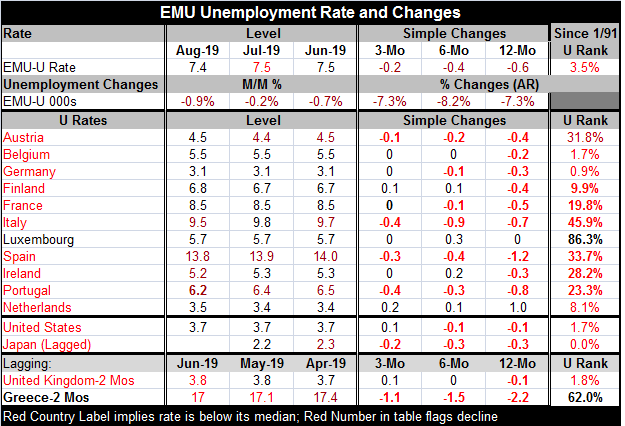

The EMU unemployment rate fell to 7.4% in August from 7.5% in July following two months at the 7.5% level. In August 2018, the rate sat at 8.0%; it has fallen by 0.6 percentage point over 12 months, an average of a one tenth drop every two months. And the declines in real time have been steady more or less on that schedule making this month's drop expected, or the very least no surprise. The reading was last at 7.4% in May 2008. May 2008 ended a string of nine months in which the unemployment rate had fluctuated between 7.3% and 7.4%. Lumping 7.3% and 7.4% together, this is as low as the EMU unemployment rate has been. That is perhaps an ominous observation.

Having offered up that observation, it is not going to be surprising to observe also that all but two of the EMU members in the table (Luxembourg and Greece, two small countries) have unemployment rates below their historic medians. In fact, after Luxembourg (86.3%) and Greece (62.0%) standings, the next highest percentile-standing unemployment rate is in Italy at its 45.9 percentile standing, below its median which has a standing at the 50th percentile in all ranges. After Italy, the next highest standing is Spain (33.7%). All the rest of the unemployment rates are in at least the lower one-third of their respective historic queues of unemployment experiences, some much lower.

Of course, the extremes find Germany in its lower 0.9%. Belgium, tracking Germany, is in its lower 1.7%. The United States and the United Kingdom are in their lower 2 percentiles and Japan is at its low rate for the period. The falling unemployment rate has finally been the rising tide that lifts all boats. And while the Germans are nervous about further ECB stimulus (as I suppose they should be…with their own jobless rate at its all-time low of 3.1%), many other European countries still would seem to have plenty of slack

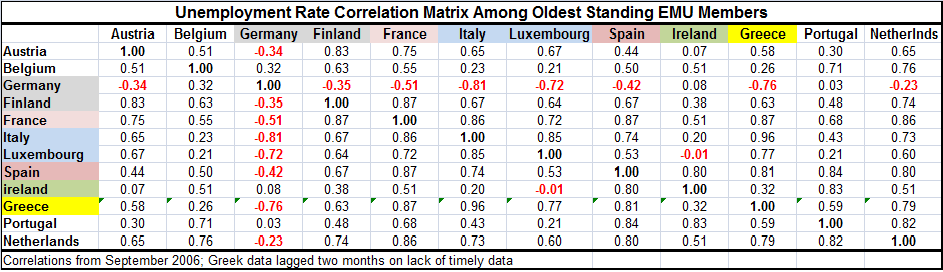

The correlation matrix between the unemployment rates of the various EMU long-time members shows that German and other member interests have not exactly been aligned. The German unemployment rate is NEGATIVELY correlated with eight fellow EMU members with tiny insignificant positive correlations between Germany and Ireland and Germany and Portugal. The only clear substantial positive correlation is with Belgium (a correlation of 0.32). What has made the unemployment rate low in Germany has generally made it higher elsewhere and vice versa! So much for EMU member interests being aligned in a union: with one common tariff position against the rest of the world, a common currency and with harmonized rules inside. This result has a lot to do with Germany's taking control of the EU after the global recession hit and putting its own stamp of strict adherence on how things were run in the EU. This approach put countries on austerity diets that were painful as Germany grew and reduced its own unemployment rate. In response, Germany lost control of events in the EMU as the ECB became much more stimulative than Germany wanted.

This same exercise performed on year-over-year changes in unemployment rates finds Germany with five negative or very low positive correlations (below 0.1) with Luxembourg, Spain, Ireland, Greece and Portugal in the low correlation group. Changes in unemployment rates for Germany correlate the highest with Austria, France and Finland. If we look at the average correlation among annual unemployment rate changes of each countries to the rest of the 11 members in the table, Germany has the second lowest average correlation, second only to tiny, idiosyncratic, Luxembourg. There is an issue here that countries seem to benefit very differently policies. The upshot is that it matters who controls policy. Germany, having sucked all the progress it can get of stimulus, is now opposed to it with increasing candor as a new ECB head comes into the picture.

Note that not all countries have data back to January 1991; some present correlations for shorter periods.

Note that not all countries have data back to January 1991; some present correlations for shorter periods.

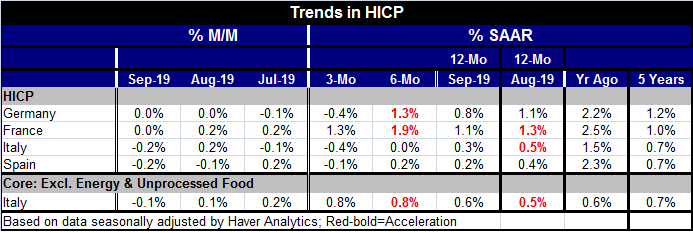

Interestingly, as Germany begins to fret anew about the lack of monetary discipline, the inflation results in the EMU continues to show inflation low and decelerating at least from three-months to six-months as well as over 12-months from what is was 12-months ago. And there are no price-reducing impacts from recession in the mix either, at least not yet. Germany's fretting is all doctrinal and divorced from real world trends and events except those that do not conform to Germanys view of how policy should be run.

However, Germany itself is facing serious challenges. Germany's vaunted auto sector is still reeling under the mileage cheating scandal and only just facing class action lawsuits from diesel-powered vehicle owners. Top corporate officials have been indicted. What's worse is that the new push to electric vehicles is a shift to a technology that will be much less labor intensive and that could have negative repercussions in Germany. Germany has been adept at scouting and developing new markets and selling very high quality goods abroad. But now trade is impacted and global growth is slowing. The German export sector has become a drag on growth instead of a leader. And what's worse is that Germany itself seems to face a need for a great deal of investment and rethinking its purpose before it will be able to turnaround. Maybe Germany will finally find itself with more in common with its fellow EMU members after all on the road ahead.

As Germany intensifies its opposition to stimulus, inflation gets lower

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief