Global| Apr 29 2016

Global| Apr 29 2016Euro Area Unemployment Drops to 4.5-Year Low

Summary

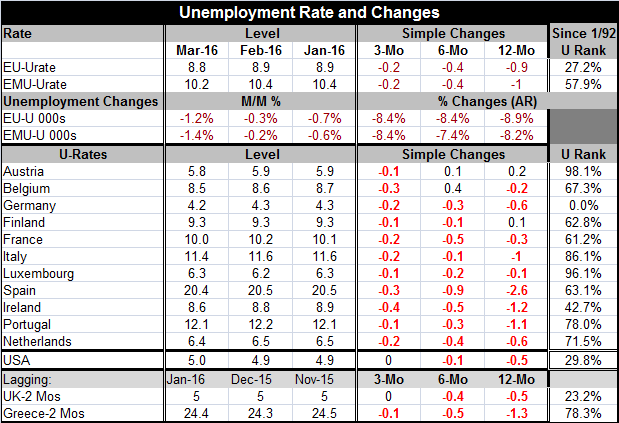

EMU unemployment fell to 10.2% in March after being stuck at 10.4% for three consecutive months. The EU rate fell to 8.8% in March after being steady at 8.9% in each of the two previous months. Most impressive is the cross-sectional [...]

EMU unemployment fell to 10.2% in March after being stuck at 10.4% for three consecutive months. The EU rate fell to 8.8% in March after being steady at 8.9% in each of the two previous months. Most impressive is the cross-sectional uninterrupted string of unemployment rate declines as all 11 early reporters listed in the table show three-month drops and only one shows a one-month rise (Luxembourg). All but two also show declines over six-months and all but two show declines year-over-year. However, as impressive as that is, the levels of the national unemployment rates are still quite different across countries and still too high. Germany continues to show the lowest unemployment rate since reunification, down to 4.2% in March. Since 1992 the only other (beside Germany) EMU member with its unemployment rate below its median on that period is Ireland. The average percentile standing of EMU members' rate of unemployment apart from Germany for this period is in the 72nd percentile. That is unemployment rates are still in the top 30% of most countries' ordered queue of results since 1992. The standing for the EMU as a whole is in its 57th percentile, a much lower standing because of the inclusion of the German results and Germany's super-low unemployment rate.

EMU unemployment fell to 10.2% in March after being stuck at 10.4% for three consecutive months. The EU rate fell to 8.8% in March after being steady at 8.9% in each of the two previous months. Most impressive is the cross-sectional uninterrupted string of unemployment rate declines as all 11 early reporters listed in the table show three-month drops and only one shows a one-month rise (Luxembourg). All but two also show declines over six-months and all but two show declines year-over-year. However, as impressive as that is, the levels of the national unemployment rates are still quite different across countries and still too high. Germany continues to show the lowest unemployment rate since reunification, down to 4.2% in March. Since 1992 the only other (beside Germany) EMU member with its unemployment rate below its median on that period is Ireland. The average percentile standing of EMU members' rate of unemployment apart from Germany for this period is in the 72nd percentile. That is unemployment rates are still in the top 30% of most countries' ordered queue of results since 1992. The standing for the EMU as a whole is in its 57th percentile, a much lower standing because of the inclusion of the German results and Germany's super-low unemployment rate.

EMU Growth

The news on unemployment is good for March and the news for EMU Q1 growth is good too, as the euro area today posted growth of 0.6% in Q1 2016. Still, its year-on-year pace has been stuck at 1.6% for the last four quarters. This was a better result than expected, but it is still a region with substantial challenges. Encouragingly, the latest GDP figures show that the euro area's economy is now bigger than it was before the start of the financial crisis eight years ago. While that is good news, it is also true that it has taken eight years to claw back to where it once was.

Across EMU

Also reporting GDP early were Belgium, France, Spain, and the U.K. (an EU member). Among these reporters, none showed a pick up in the year-on-year rate of growth compared to what each had posted in Q4 2015. Belgium, France and Spain each showed a slight downtick in the pace of year-over-year growth in Q1 while for the U.K. the year-on-year pace was unchanged at 2.1%.

EMU Inflation

The early inflation reading for the EMU is out today as well and the EMU is back in the soup with prices falling on balance over 12-months. Yes, deflation is back, but so far only in a very small way (-0.2% over 12-months). Core HICP inflation is at 0.8% over 12-months, but it is showing signs of further deceleration from 12-month to six-month and from six-month to three-month. France, Italy and Spain each show prices are lower on balance over 12-months. Germany shows a tiny 0.1% uptick over 12-months.

Looking Ahead

The eurocoin index, a construct from the Bank of Italy and the Centre for Economic Policy Research, stepped down to a 0.28 reading in April from 0.34 in March. This gauge, tracking current growth trends in the EMU, is pointing to some reduction in growth currently. Today has been unusual in terms of the number of important reports that have been dumped on our doorstep.

Consumption in EMU

Consumer spending has been important in the EMU. It has been the leading sector according to the sector queue percentile standings of the EU Commission indices we reported on yesterday. As we end Q1, German retail sales dropped by 1.1% month-to-month in real terms in March after being flat in February. German sales are losing momentum. In France, consumer spending grew less than expected, rising by 0.2% in March from February. Since consumption and the services sector really have been driving growth in the EMU, these are going to be trends to keep an eye on.

A Coat of Many Colors

Today's economic reports range far and wide across the economic spectrum in the EMU and also globally. The yen hit an 18-month high. Taiwan remains in recession as GDP fell for the third consecutive quarter. Oil reached a new 2016 high. Among the smaller EMU countries, Latvia is in recession and Estonian and Latvian retail sales slowed. Lithuanian GDP rose in Q1.

The drop in unemployment rates for the EMU and across the EMU is an unimpeachable piece of good news. The acceleration in quarterly GDP in EMU is also good news. But the still-high levels of unemployment in much of the EMU are reminders of challenges ahead as inflation crosses over back to the land of deflation, however brief this visit might be. Few are crowing about the new EMU growth figures as harbingers of better times ahead. There are really more warnings being launched about how hard it will be to keep this pace up. Realistically it is a day of some good economic news for Europe, but still a day to dig in and work for a better tomorrow. There no reason here to celebrate or to pop any Champaign corks. Challenges lie ahead as well as lurk in the here and now.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief