Global| Jul 30 2019

Global| Jul 30 2019German Confidence Slips for the Third Month in a Row

Summary

German confidence slipped lower for the third month in a row, continuing a run of weakening that began after February 2018 and despite a failed attempt at rebounding in February 2019. There is an expedited trail of decay since March [...]

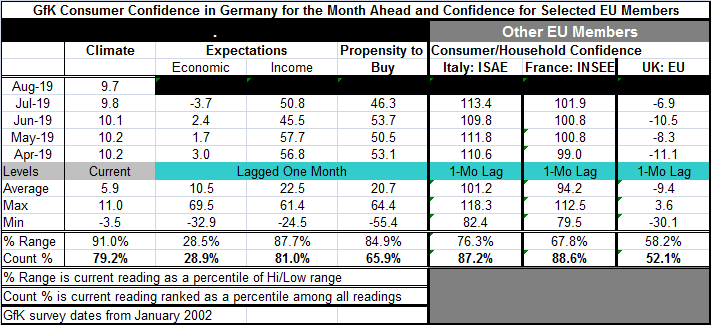

German confidence slipped lower for the third month in a row, continuing a run of weakening that began after February 2018 and despite a failed attempt at rebounding in February 2019. There is an expedited trail of decay since March 2019. Germany’s weakening trend in confidence overall extends back 1.5 years. The overall consumer climate reading has a 79th percentile queue standing. The headline is down some 11% from its peak in this cycle.

German confidence slipped lower for the third month in a row, continuing a run of weakening that began after February 2018 and despite a failed attempt at rebounding in February 2019. There is an expedited trail of decay since March 2019. Germany’s weakening trend in confidence overall extends back 1.5 years. The overall consumer climate reading has a 79th percentile queue standing. The headline is down some 11% from its peak in this cycle.

The components for this survey lag by one month. Two of them economic expectations and ‘propensity to buy’ weakened on the month as of July. Income expectations moves higher.

Income expectations have an 81st percentile queue standing, in line with the overall climate standing. But economic expectations fell into negative territory and have a 28.9 percentile standing, well below its historic median (which occurs at a ranking of 50). The propensity to buy index has a 65.9 percentile standing, above its median but still a moderate reading.

The propensity to buy index was last weak in October 2015. The economic index is at its weakest mark since November 2015. The climate reading is at its weakest since April 2016. The German confidence metrics are beginning to find comparability with readings from much earlier in this cycle when the German economy was struggling more.

Comparisons to other European economies show 87 and 88th percentile standing for confidence in Italy and France respectively. In the UK confidence moved up to a 52 percentile standing, barely above its median.

The UK is fighting its battle over Brexit and it has a new Prime Minister to do that. Boris Johnson is confronting the EU over its no further negotiation position. Johnson claims that he will let a hard Brexit occur before he accepts the status quo. He is still fighting over the Irish backstop. All of this helps to keep matters uncertain, but with a new leader and clear focus the British consumer may have a new hope.

It is not clear if Germany’s standing as Europe’s most solid economy is being challenged or not. France, an economy that had been doing better and gaining momentum until the Yellow Vest protests emerged, saw its GDP in Q2 slow to a 0.2% gain from a 0.3% gain in Q1 (annualized: 0.8% from 1.2% previously). French household spending also fell in June. In Sweden, there was an unexpected (but small) decline in GDP logged in Q2. In Asia, Japan posted a large decline in industrial production. On balance, there is still a lot of shifting around for growth among its sources. There is a lot of unevenness and evidence of erratically weak growth and of fading retail sales. On the whole, Europe does look like it is slowing and it looks like it is losing its usual anchor for growth, the German economy. Meanwhile, all eyes are on central banks. Japan rolled the dice on an unchanged but flexible policy. It continues to say it sees inflation coming back to its 2% target. On Wednesday, the Fed is expected to cut rates, a small step to make sure that inflation gets back to its 2% target. Global monetary policy is in flux and we can’t be sure to which policies central banks ready to commit or if they have the right focus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates