Global| Sep 24 2013

Global| Sep 24 2013German Ifo Improves...But Barely

Summary

Germany's Ifo business climate gauge rose to 8 in September from 7.7 in August, marking its sixth straight monthly increase. The all-sector climate gauge sits in the 81.4 percentile of its historic queue implying that it's higher than [...]

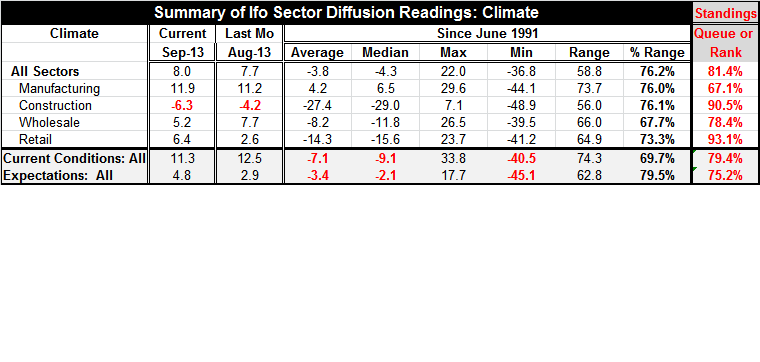

Germany's Ifo business climate gauge rose to 8 in September from 7.7 in August, marking its sixth straight monthly increase. The all-sector climate gauge sits in the 81.4 percentile of its historic queue implying that it's higher than this only about 19% of the time. The index was last stronger in April 2012 at a level of 11.8. And, it was substantially stronger from July 2010 to July 2011 with diffusion values in the twenties.

Germany's Ifo business climate gauge rose to 8 in September from 7.7 in August, marking its sixth straight monthly increase. The all-sector climate gauge sits in the 81.4 percentile of its historic queue implying that it's higher than this only about 19% of the time. The index was last stronger in April 2012 at a level of 11.8. And, it was substantially stronger from July 2010 to July 2011 with diffusion values in the twenties.

Improvement in the Ifo was expected this month, however, improvement was expected to be larger. Manufacturing continues to show gains as its diffusion gauge rose to 11.9 in September compared to a level of 11.2 in August. The construction sector, however, slipped to -6.3 from -4.2. Wholesaling also slipped to 5.2 from a level of 7.7 in August. The surprising strength this month came from the retail sector where the climate index rose to +6.4 from +2.6 in August.

Looking at the various sector rankings right now, retailing has the relative strongest performance. The retail index sits in the 93.1 percentile of its historic range implying that it's higher only about 7% of the time. Despite its overall negative reading construction is the next strongest sector as its index is stronger than this only about 10% of the time. Wholesaling is stronger than its September index only about 22% of the time. Manufacturing is stronger than its September value about one third of the time.

You can gain some understanding of the relative strength of the various sectors by comparing their September values to the average values of the median values in the table. Everything except manufacturing has an average and median value over this period (since mid-1991) that is negative. The German economy seems to be showing improvement in all sectors except that this month there is some backtracking in construction and wholesaling while the improvement in manufacturing is modest by recent standards.

In July the month-to-month improvement manufacturing was even less than it was this month. There is some evidence that improving trend the manufacturing is slowing down - rather than accelerating as many seem to think.

Current conditions overall incurred a setback this month to 11.3 from 12.5 in August. The current conditions index stands just above and 79th percentile and is stronger than its current level only about 21% of the time. Expectations, which continued to improve this month rising to 4.8 in September from a level of 2.9 in August, stand in the 75th percentile of their historic queue and are higher about 25% of the time.

These Ifo metrics obviously are positive and would be the envy of any other country in the European Monetary Union. However, the rate of progress of the various components appears to have slowed and for several key components there some backtracking this month. Importantly, the expectations index continues to press ahead. And perhaps, hopefully, for the rest of the monetary union, the sharpest improvement is in the retail sector in Germany although Germany is not exactly a voracious importer of consumer goods.

My sense of the Ifo report this month is somewhat less positive. Key sectors continue to have upward momentum. One month's worth of setback is hardly reason for pessimism. That, of course applies to the overall current conditions index, the construction sector, and the wholesaling sector. However, the gains in manufacturing are slowing down and the German economy is not going to be carried by an improvement in retailing.

However.improvement in retailing has to have some basis; German consumers are not going to be substantially more upbeat unless there really is something solid improving in the economy. So that's the thing to look for in the months ahead. The question is whether conditions in the other sectors have become more solid despite slower improvement in some cases or monthly backtracking in September. Is it accumulated trend improvement that's being reflected in retailing, or is retailing giving us a rogue positive reading in September that will not be sustained?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates