Global| Mar 31 2016

Global| Mar 31 2016German Retail Sales Slip But Real Sales Retain Momentum

Summary

Europe, where consumer is king...yes I said Europe It is no secret that Europe has been driven by its services sector nor is it a secret that retailing has been the strongest of the sectors in the EU Commission indicator framework. [...]

Europe, where consumer is king...yes I said Europe

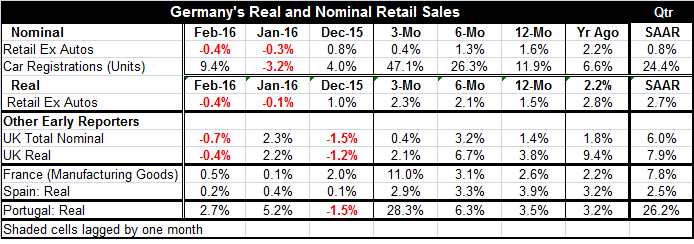

It is no secret that Europe has been driven by its services sector nor is it a secret that retailing has been the strongest of the sectors in the EU Commission indicator framework. That means that a setback in retailing is a more serious event than it might otherwise have been in the past. In other times, we would expect the industrial sector to be driving growth with retailing filling in. This time it's different. With that as background, German retail sales (ex-autos) both nominal and real fell in February for the second consecutive month.

Europe, where consumer is king...yes I said Europe

It is no secret that Europe has been driven by its services sector nor is it a secret that retailing has been the strongest of the sectors in the EU Commission indicator framework. That means that a setback in retailing is a more serious event than it might otherwise have been in the past. In other times, we would expect the industrial sector to be driving growth with retailing filling in. This time it's different. With that as background, German retail sales (ex-autos) both nominal and real fell in February for the second consecutive month.

German retail sales trends

While this drop may not completely overturn the German growth apple cart, it is not welcome. Momentum in retail sales is still in place. Nominal retail sales ex-autos are slowing down from 12-month to six-month to three-month. But for real (inflation adjusted) retail sales, there is still persistent acceleration over these same horizons. In the quarter-to-date, nominal sales are up at a 0.8% pace while real retail sales are up at a 2.7% pace. These metrics are for ex-auto sales two months into the quarter with growth calculated over the Q4 base.

Autos are still hot

Auto registrations in Germany are still hot. Unit registrations were up by 9.4% in February; over three months, they are up at a 47.1% annual rate. They are up at a 24.4% annual rate in the quarter-to-date. German auto registrations seem to be suffering not all from the black eye Volkswagen received over its troubles with its environmental testing.

Less robust looking ahead, however

However, we need a caveat here. It is that retail sales growth rates, while `accelerating in real terms,' top out at 2.3% over three months (annualized) and at 2.7% in the quarter-to-date. Since sales have fallen for two months running, the next (three-month) retail sales growth figures will not have the benefits of the 1% real (0.8% nominal) gain in December to push them ahead. So momentum may turn out to be more challenged than it seems. That will depend on March sales.

Germany is more solid than strong and no locomotive

Germany is the solid economy of Europe. Since it runs a trade and current account SURPLUS, it is hardly an engine of growth. Germany tends to export more than it imports which means it feeds off domestic demand in its trade partner economies instead of offering opportunities for foreign countries to benefit from German consumer strength (on a net basis). Of course, some bilateral trade flows may differ from that aggregate condition. But in addition to the fact that Germany is not an engine of growth, its growth rate also is not as strong as it is consistent. Germany benefits European growth more by `being a large weight in the European average' than by exciting growth in the countries around it.

Beyond Germany in Europe

Turning to other EU/EMU early reporters of retail sales, we find the U.K. and Spain each with nominal or real flows that show sequential slowing. Both of these countries still show solid to strong sales gains in the quarter-to-date. France and Portugal show sales (generally) accelerating; Portuguese sales are especially strong in the quarter-to-date.

Europe on balance

On balance, while there is some scattered weakness in February sales for Germany and in the U.K., the other early reporters show sales that are continuing to plow ahead in either nominal or real terms or both. Quarter-to-date sales seem to be relatively solid across these reports with question marks mostly above Germany because of its two sales declines in January and in February. Fortunately, Germany is no bellwether in this regard.

European consumer confidence does not reassure

On another front, EMU wide consumer confidence continued to decline in March and has been slipping since December. Each of the Big-Four EMU economies has seen a net drop in confidence from its December level and the U.K. (an EU member) has too. Today the Eurocoin index, an indicator of European growth, showed its weakest reading in 11 months. The U.K. GfK confidence reading steadied month-to-month, in another topical report released today, at its lowest level in more than one year. The picture of consumer confidence in Europe is not all that reassuring.

Germany and spending on migrants

Despite the recent irregular results, German spending should be somewhat underpinned by spending to bolster the migrants it is caring for. We will have to look in the official statistics to see how care is being provided and funded to see which German accounts are going to register this spending. Spending on migrants may simply go down as government spending even though it will be spending on consumer goods and services to sustain migrants such as for food shelter and clothing. In that case, the German retail sales may not reflect it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates