Global| Dec 27 2019

Global| Dec 27 2019Japan's Activity Gauges Paint a Picture of Withering Growth or Worse

Summary

Japans' retail sales rebounded but only part way after a horrific decline in the wake of its consumption tax hike. On October 1, the government raised the consumption tax from 8% to 10%. While retail sales had risen by 7.2% in [...]

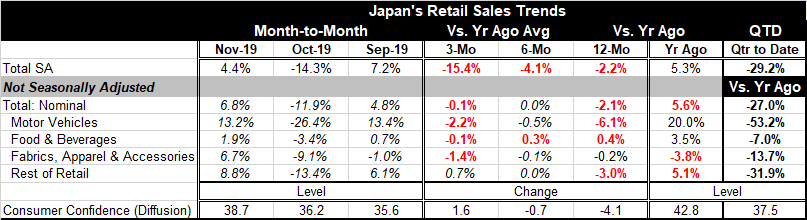

Japans' retail sales rebounded but only part way after a horrific decline in the wake of its consumption tax hike. On October 1, the government raised the consumption tax from 8% to 10%. While retail sales had risen by 7.2% in September ahead of the well-telegraphed hike, sales proceeded to drop by 14.3% in October. Now in November sales have rebounded by a disappointing 4.4%. Since August, sales are lower 4.9%. In the quarter-to-date, sales are plunging at a 29.2% annualized rate. But if consumers got a two-month head start on pre-purchasing ahead of the hike, sales are actually up by 0.4% from July. July itself was a month in which sales fell (the industry data have the shortcoming of being not seasonally adjusted). However, if we peruse the year-on-year data, we also see strong year-on-year sales gains in August preceded by a rise of only 1.9% year-on-year in July. On balance, it looks like pre-purchasing was mostly a one-month phenomenon. This interpretation puts retail sales on a weakening path more than on an ambiguous path. Durable goods do not appear to have been purchased in size more than one-month ahead of the imposition of the tax. As a result, the three months of percentage changes leave us with a very weak collective retail sales result. The sales tax hike was only a hike of two percentage points, but that also meant that the 'tax' itself was rising by 25% from what it had been.

Japans' retail sales rebounded but only part way after a horrific decline in the wake of its consumption tax hike. On October 1, the government raised the consumption tax from 8% to 10%. While retail sales had risen by 7.2% in September ahead of the well-telegraphed hike, sales proceeded to drop by 14.3% in October. Now in November sales have rebounded by a disappointing 4.4%. Since August, sales are lower 4.9%. In the quarter-to-date, sales are plunging at a 29.2% annualized rate. But if consumers got a two-month head start on pre-purchasing ahead of the hike, sales are actually up by 0.4% from July. July itself was a month in which sales fell (the industry data have the shortcoming of being not seasonally adjusted). However, if we peruse the year-on-year data, we also see strong year-on-year sales gains in August preceded by a rise of only 1.9% year-on-year in July. On balance, it looks like pre-purchasing was mostly a one-month phenomenon. This interpretation puts retail sales on a weakening path more than on an ambiguous path. Durable goods do not appear to have been purchased in size more than one-month ahead of the imposition of the tax. As a result, the three months of percentage changes leave us with a very weak collective retail sales result. The sales tax hike was only a hike of two percentage points, but that also meant that the 'tax' itself was rising by 25% from what it had been.

The retail situation in the quarter-to-date shows motor vehicle sales has hardest hit with food and beverages the least affected followed by fabric, apparel and accessories.

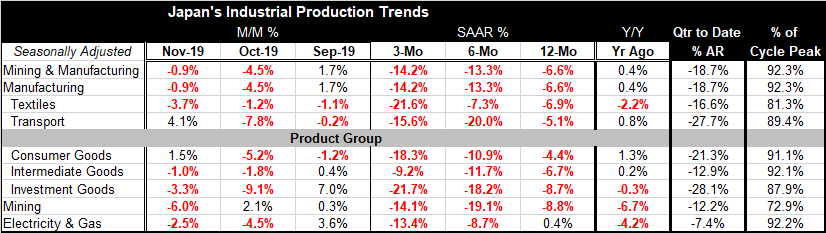

Over the same period, Japan's industrial production data show weakening in train with a large drop in October and a follow-up drop in November. Manufacturing output is falling at a 14.2% annual rate over three months, a touch faster drop than over six months and a much faster drop than over 12 months. On a quarter-to-date basis, IP in manufacturing is falling at an 18.7% rate.

Japan is caught between the Scylla and Charybdis of the U.S.-China trade war and the domestic consumption tax hike it would not postpone again. One is clobbering retail sales; the other is impacting industrial output. There is nowhere to hide. Japan is hoping beyond hope that the U.S.-China trade deal (phase-One) is consummated quickly and has a significant impact. As we look to the New Year, everyone had hopes. Some are realistic and some are not...

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief