Global| Feb 07 2003

Global| Feb 07 2003Nonfarm Payrolls Up Twice Expectations

by:Tom Moeller

|in:Economy in Brief

Summary

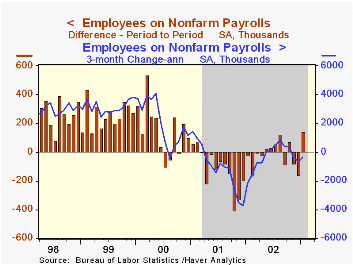

Nonfarm payrolls rose roughly twice Consensus expectations for a 70,000 worker rise. The decline in December payrolls was deepened by about half from a 101,000 decline reported last month. The rise in January payrolls was the largest [...]

Nonfarm payrolls rose roughly twice Consensus expectations for a 70,000 worker rise. The decline in December payrolls was deepened by about half from a 101,000 decline reported last month.

The rise in January payrolls was the largest since November 2000 and may have reflected difficulty in seasonally adjusting employment in the retail and construction industries.

Diffusion indexes for nonfarm payrolls suggested genuine labor market improvement. The one-month index rose to 50.1, the highest level since May and the three month diffusion index also rose to 45.4. These indexes are leading indicators of employment growth.

The unemployment rate fell unexpectedly to 5.7%. Employment rose 1,097,000 (0.8%) following three months of decline. The labor force rose 688,000.

Amongst industries, the number of factory sector jobs continued down, falling 16,000 (-3.0% y/y). It was the smallest monthly decline in manufacturing jobs since July. The one-month diffusion index for the factory sector improved sharply to 44.1, the highest level since July. Construction jobs rose 21,000 (-0.7% y/y) following an upwardly revised December gain. Jobs in service producing industries rose 143,000 (0.5% y/y). Retail hiring rose 101,000 (-0.6% y/y). Services rose 35,000 and government employment rose 4,000.

Aggregate hours worked rose 0.3% following three months of decline. The index of aggregate hours worked (employment times hours worked) started 1Q03 slightly ahead of 4Q02.

Over the last ten years there has been a 54% correlation between the quarterly change in aggregate hours worked and real GDP. That correlation is down from 89% in the 1980s. The decline is due to the recent acceleration in productivity growth.

Average hourly earnings were unexpectedly weak.

The nonfarm payroll employment figures are based on reports provided to the US Labor Department by businesses, while the figures from which the unemployment rate is derived are based on a survey of US households.

| Employment | Jan | Dec | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Payroll Employment | 143,000 | -156,000 | -0.1% | -0.9% | 0.2% | 2.2% |

| Manufacturing | -16,000 | -80,000 | -3.0% | -5.5% | -4.2% | -0.4% |

| Average Weekly Hours | 34.2 | 34.1 | 34.1 | 34.2 | 34.2 | 34.4 |

| Average Hourly Earnings | 0.0% | 0.3% | 2.7% | 3.2% | 4.0% | 3.8% |

| Unemployment Rate | 5.7% | 6.0% | n.a. | 5.9% | n.a | n.a. |

by Tom Moeller February 7, 2003

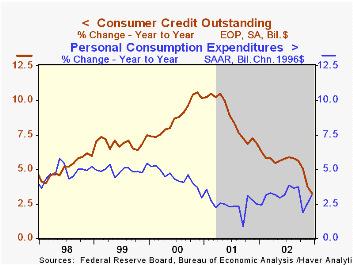

Consumer credit outstanding fell unexpectedly in December. Consensus expectations had been for a $4.5B rise. The preliminary report of a decline in November was revised to positive due to a raised figure for revolving credit. The gain in consumer credit outstanding last year was the weakest since the recession year of 1991.

Revolving credit plummeted 1.2%, the sharpest one month drop since 1974. The annual gain in 2001 was the weakest on record.

Nonrevolving credit managed a 0.4% gain following a drop in November, but for the quarter, growth of 0.5% was the weakest since 1998.

| Consumer Credit Outstanding | Dec m/m | Nov m/m | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Total | $-4.0B | $-0.1B | 3.3% | 3.3% | 6.9% | 10.2% |

| Revolving | $-8.4B | $1.7B | 1.6% | 1.6% | 5.0% | 11.5% |

| Nonrevolving | $4.4B | $-1.8B | 4.4% | 4.4% | 8.3% | 9.2% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates