Global| Sep 26 2013

Global| Sep 26 2013Truth Is Found in Global Money and Credit Trends; Money Growth Tells Story of Revival in UK and Japan; Credit [...]

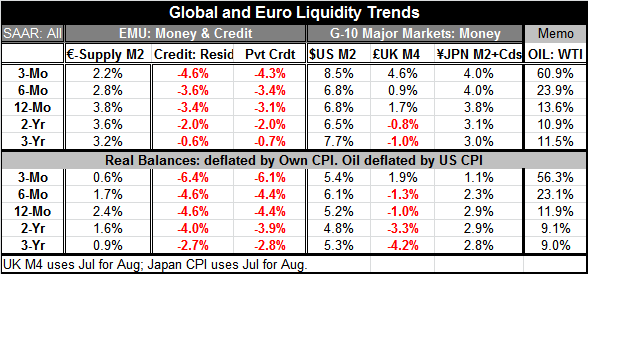

Summary

Money growth rates in the UK, the US and Japan show clear evidence of either continuing or improving growth in the respective economies. In the US, nominal money growth has been steady, vacillating between six and eight and one-half [...]

Money growth rates in the UK, the US and Japan show clear evidence of either continuing or improving growth in the respective economies.

In the US, nominal money growth has been steady, vacillating between six and eight and one-half percent at an annual rate over the last 12-months, two years, and three years as well as over last three- and six-months. Real money growth in the US is vacillating in a narrow range between roughly 4% and 6% on these same horizons.

In the UK, nominal money growth has transitioned from negative growth rates of about 1% at an annual rate to positive rates of growth just under 2% over the last year to steadier menu of positive growth rates over three- and six-months. Real money growth in the UK has showed progressively smaller annual rates of decline from three years to two years to one year, with the most recent three month growth rate producing a positive 2% annual rate of increase.

In Japan nominal money growth has accelerated mildly. Nominal money growth rates have transitioned from about 3% over two and three years to 3.8% over 12 months and 4% over three- and six-months. Real money growth in Japan has been declining to some extent from growth rates just under 3% over three years two years in one year to 2.3% at an annual rate over six-months and 1% at an annual rate over three-months. Slower growth in real balances in Japan is not so disturbing because one of the things generating this is less deflation and more price stability. Improvement in nominal money growth suggests that Japan is after all on the right track. We expect the decline in real balance growth in Japan to reverse because of other policies put in place.

The chart on nominal money growth shows that US money growth has been the strongest among this group of countries since early 2011. US money growth during that period has bubbled up and has since stabilized. Japan's money growth has accelerated slightly after a long period of stability. The UK's money growth boomed ahead of and during the financial crisis and then busted with substantial negative rates of growth; UK money growth has only recently turned to positive rates of growth. In the European Monetary Union broad money growth had slightly accelerated until the last few months when a modest deceleration has appeared. But when we look at the growth of money supply in the European Monetary Union and compare it to credit growth a darker picture emerges.

From late 2009 to early 2010, the drop in money and credit growth in EMU began to reverse. Money growth picked up through late 2011 and then it accelerated until just recently. But credit growth has become the fly in the ointment.

Credit growth went on a steady increase, mimicking the rise in money growth, until later in 2011. But, since then, credit growth has been declining and has actually been contracting since late 2012 (since late 2010 on some measures). The deviation in the growth rates of money versus credit is something we have written about for quite some time. The deviation is surprising and has been enduring. Such a divergence, however, is not sustainable.

What's beginning to happen in the European Monetary Union is that the decline in credit is continuing apace on its negative path. but, the growth in money supply is beginning to give way. Despite what had been a lot of optimism on the European Monetary Union's fortunes and some better performance in terms of several economic variables including the widely watched PMI data, the underlying situation in the Monetary Union is NOT getting better.

In a study just released this past week European banks were cited as being short on capital. It's not surprising that when banks and are short on capital, they are not lending. The ECB has done what it can do-and perhaps more than it should-to try to breathe life back into the Monetary Union. What has happened is that its attempts to extend itself continue to be blocked by the Bundesbank. Meanwhile, in the private sectors of the various European economies, hard times continue and bank lending is not supportive.

The downdraft in terms of economic growth has abated and reversed in a number of European countries. However, competitiveness issues, related to being locked in a currency union with several super-competitive countries - and with a number of very uncompetitive countries - will continue to take its toll. The message from the chart on EMU money supply growth versus loan growth is to be wary about being too optimistic about the near-term economic data coming out of the European Union. Europe still has significant problems it needs to fix. Sustainability in growth requires growth in both money and in credit. EMU is not there yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.