Global| Jan 12 2018

Global| Jan 12 2018U.S. Retail Sales Were Solid in December with Upward Revisions to October and November

by:Sandy Batten

|in:Economy in Brief

Summary

Total retail sales posted a solid 0.4% m/m (5.4% y/y) increase in December on top of strong upwardly revised rises in October and November. The initially reported 0.5% m/m increase in October was revised up to a 0.7% m/m rise, and the [...]

Total retail sales posted a solid 0.4% m/m (5.4% y/y) increase in December on top of strong upwardly revised rises in October and November. The initially reported 0.5% m/m increase in October was revised up to a 0.7% m/m rise, and the initially reported 0.8% m/m increase in November was revised to a 0.9% m/m increase. The December reading was roughly in line with the consensus expectation from the Action Economics Forecast Survey--for a 0.5% m/m increase. Excluding sales of motor vehicles and parts, retail sales also rose 0.4% m/m (6.3% y/y), in line with expectations, and again there were meaningful upward revisions to the already solid October and November increases.

With the significant upward revisions to October and November and solid December reading, the quarterly performance of consumer spending in the fourth quarter of 2017 was quite strong. Total retail sales were up 2.7% q/q (not annualized) in the fourth quarter while sales excluding autos rose 2.6% q/q. With headline CPI inflation at 0.9% q/q in Q4, today's report points to extremely solid gains in real consumer spending in last year's fourth quarter and indicates that consumer spending should make a meaningful positive contribution to overall GDP growth in the fourth quarter.

For 2017 as a whole, retail activity was generally stronger than in 2016. Total sales rose 4.2% in all of 2017 versus a 3.2% increase in 2016. Excluding autos, sales were up 4.3% in all of 2017 versus 3.0% in 2016.

The department store/non-store retailer divergence continued in December. Sales at department stores fell 1.1% m/m (+0.5% y/y) while sales at non-store retailers were up 1.2% m/m (12.7% y/y). The widely considered harbinger of discretionary retail activity--sales at food services and drinking places--rose a solid 0.7% m/m (4.2% y/y) in December.

In the detail, the December increase was generally widespread as had been the November rise. Of note, apart from the decline in department store sales, clothing sales declined 0.3% m/m (+2.4% y/y) and sales at sporting goods, hobby, book & music stores slumped 1.6% m/m (-0.1% y/y) in December.

The retail sales data can be found in Haver's USECON database. The Action Economics forecast is in the AS1REPNA database.

| Retail Spending (% chg) | Dec | Nov | Oct | Dec Y/Y | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|

| Total Retail Sales & Food Services | 0.4 | 0.9 | 0.7 | 5.4 | 4.2 | 3.2 | 2.6 |

| Excluding Autos | 0.4 | 1.3 | 0.5 | 6.3 | 4.3 | 3.0 | 1.4 |

| Non-Auto Less Gasoline | 0.4 | 1.2 | 0.5 | 5.8 | 3.7 | 3.9 | 4.2 |

| Retail Sales | 0.3 | 0.9 | 0.7 | 5.6 | 4.4 | 2.9 | 1.9 |

| Motor Vehicle & Parts | 0.2 | -1.0 | 1.4 | 2.3 | 4.0 | 4.1 | 7.3 |

| Retail Less Autos | 0.3 | 0.5 | 0.5 | 6.7 | 4.5 | 2.5 | 0.4 |

| Gasoline Stations | 0.0 | 3.0 | 0.2 | 9.1 | 8.8 | -5.7 | -17.6 |

| Food Service & Drinking Places Sales | 0.7 | 0.5 | 0.5 | 4.2 | 2.8 | 5.9 | 8.1 |

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

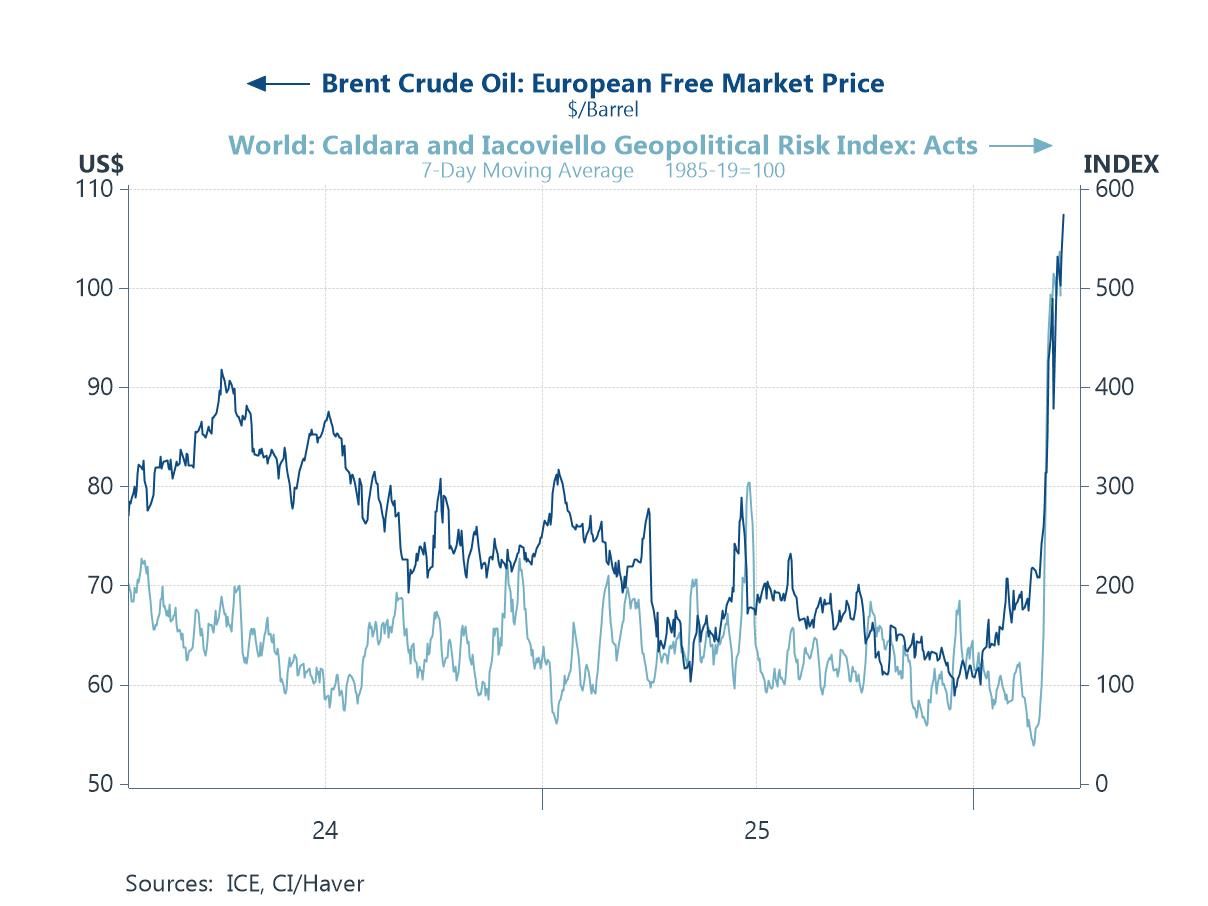

Global| Mar 19 2026

Global| Mar 19 2026Charts of the Week: Energy Shock — Early Signals, Uncertain Fallout

by:Andrew Cates