Global| May 04 2006

Global| May 04 20061Q U.S. Productivity Improved, Profits' Implication Good

by:Tom Moeller

|in:Economy in Brief

Summary

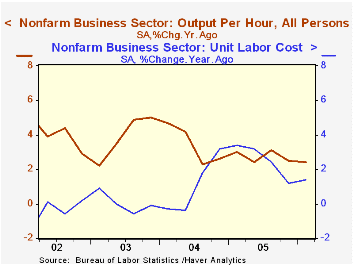

Non-farm labor productivity growth last quarter improved to 3.2% from the 0.3% decline during the final quarter of 2005. The increase beat Consensus expectations for a 2.8% rise and also represented improvement from the average [...]

Non-farm labor productivity growth last quarter improved to 3.2% from the 0.3% decline during the final quarter of 2005. The increase beat Consensus expectations for a 2.8% rise and also represented improvement from the average quarterly growth rates during 2004 (2.7%) and 2005 (2.5%).

Output growth surged to 5.8% (4.1% y/y) from just 1.5% during 4Q. That surge was on the back of only a 2.5% (1.7% y/y) rise in hours worked after a 1.8% increase the prior quarter.

Unit labor cost growth of 2.5% was slower than the 4Q increase but nevertheless represented an acceleration in labor cost pressures from a quarterly average of 1.3% during 2005.

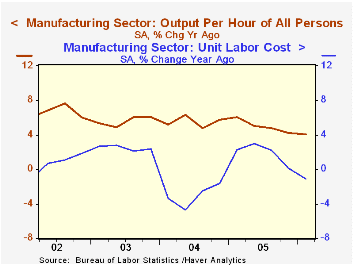

Factory sector productivity grew 4.2% (4.1% y/y), right on the firm 4.3% quarterly pace of last year. Compensation grew just 1.5% (3.0% y/y). Therefore unit labor costs in the factory sector declined for the third of the last four quarters, off 2.6% (-1.1% y/y) during 1Q06.

A Leaner, More Skilled U.S. Manufacturing Workforce from the Federal Reserve Bank of New York is available here.

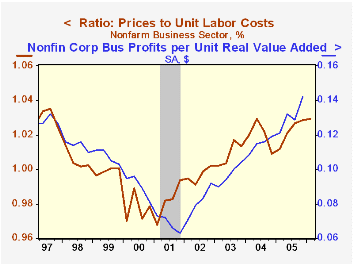

The implicit price deflator for the nonfarm business sector rose 2.8% (3.1% y/y) after a 3.6% jump during 4Q05.The rise lifted the ratio of prices to unit labor costs to near the highest level since 1997. During the last ten years there has been an 81% correlation between this ratio and corporate profit margins.

In Why Did U.S. Market Hours Boom in the 1990s?, the Federal Reserve Bank of Minneapolis examines the impact of longer hours worked on productivity & profits. The paper can be found here.

| Non-farm Business Sector (SAAR) | 1Q '06 | 4Q '05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Output per Hour | 3.2% | -0.3% | 2.4% | 2.7% | 3.4% | 3.9% |

| Compensation per Hour | 5.7% | 2.7% | 3.8% | 5.4% | 4.6% | 4.0% |

| Unit Labor Costs | 2.5% | 3.0% | 1.4% | 2.5% | 1.1% | 0.0% |

by Tom Moeller May 4, 2006

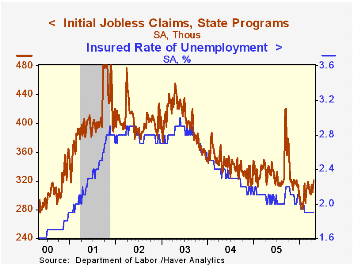

Initial claims for jobless insurance rose 5,000 last week to 322,000 from an upwardly revised level the prior period. Consensus expectations had been for 310,000 claims.

The increase pulled the level of claims filed last month up to 314,000. The 1.6% increase versus March was the third m/m rise since the January low when just 286,000 claims were filed.

The four week moving average of initial claims rose to 314,250 (-4.4% y/y).

Continuing claims for unemployment insurance rose for the third consecutive week. The 21,000 increase followed a downwardly revised 14,000 increase the prior week.

The insured unemployment rate remained at 1.9%, where it's been since early February.

Assessing the impact of job loss on workers and firms from the Federal Reserve Bank of Chicago can be found here.

| Unemployment Insurance (000s) | 04/29/06 | 04/22/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Initial Claims | 322 | 317 | -5.6% | 332 | 343 | 403 |

| Continuing Claims | -- | 2,462 | -5.5% | 2,663 | 2,923 | 3,530 |

by Carol Stone May 4, 2006

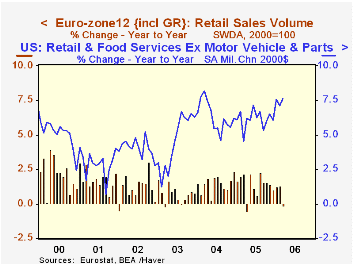

Retailers in several diverse regions are seeing mixed demand, according to data available today for February and March. In the EuroZone12 (the grouping that includes Greece throughout), sales were down 0.8% in March after a 0.1% decrease in February. The March drop carried the total down 0.2% below the year-ago amount. As seen in the table below, retailing in the major European nations has hardly been robust over recent years, and these latest data indicate that the trend is not improving. Food stores are the leader in the downward movement, but sales volume at nonfood stores is also weakening.

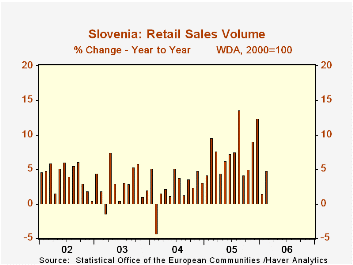

Just on the south side of the Euro-Zone, Slovenia's retail sector looks fairly mixed. Total sales fell in both January and February, but some of February's weakness is due to quirks in the arithmetic of combining the food and nonfood segments into a common index. Each of these categories actually increased, food stores by 2.0% and nonfood outlets by 1.3%. Food recovered somewhat from a steep 13.5% fall in January. In general, though, consumers in Slovenia have been increasing their spending in stores, with 2005 showing total growth of 7.6%.

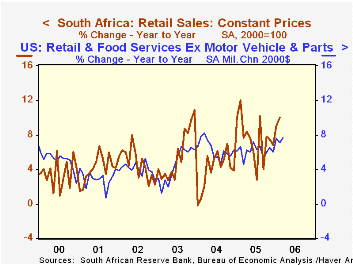

Significantly further south, retail trade in South Africa seems to be going strong. After a hesitation in January, sales in February expanded 3.8%, putting the year-on-year gain at 10.4%.

All of these retail sales figures are seasonally adjusted and adjusted for inflation. They also exclude motor vehicles. To give these data some context, we consulted some US information, the retail sales dataset prepared by the BEA, which includes comparable adjustments. These sales were flat in March and eased by 0.2% in February. So they've slowed too, then, in the last couple of months, although they remain a hefty 7.6% ahead of a year ago. Thus, while European consumers appear to be dragging, in other select regions, they have been spending at a good clip. Now that gasoline prices have taken off again, it will be interesting to see what the reaction of these other spending patterns will be.

The EuroZone data are contained in Haver's EUROSTAT database as is that for Slovenia. Other Slovenia data are in EMERGECW, and South Africa in EMERGEMA. The US series is from those compiled by the BEA from the original Census data; these appear in USECON in the menu just beneath the main Census entry and also in USNA in the Underlying Detail tables.

| Mo/Mo & Yr/Yr % Changes, SA* | Mar 2006 | Feb 2006 | Jan 2006 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| EuroZone12 | -0.8 | -0.1 | 0.5 | -0.2 | 1.3 | 1.5 | 0.7 |

| Food | -1.0 | -0.1 | 0.8 | -0.9 | 0.7 | 1.2 | 1.3 |

| Nonfood | -0.5 | -0.1 | 0.2 | 0.5 | 1.8 | 1.7 | 0.2 |

| Slovenia | -- | -1.1 | -5.3 | 4.8 | 7.6 | 2.6 | 3.0 |

| Food | -- | 2.0 | -13.5 | -1.7 | 7.4 | 3.3 | -1.3 |

| Nonfood | -- | 1.3 | 0.4 | 12.7 | 7.1 | 2.6 | 8.0 |

| South Africa | -- | 3.8 | -1.0 | 10.4 | 6.7 | 9.7 | 4.9 |

| United States** | 0.0 | -0.2 | 2.2 | 7.6 | 6.1 | 6.3 | 4.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates