Global| Aug 30 2019

Global| Aug 30 2019EMU Inflation Trends Lower on Weak August

Summary

EMU inflation is subdued in August on the heels of flat headline and core prices in July. The headline HICP rose by 0.1% in August while the core rate was flat for the second month in a row. Despite clear weakness in prices, a [...]

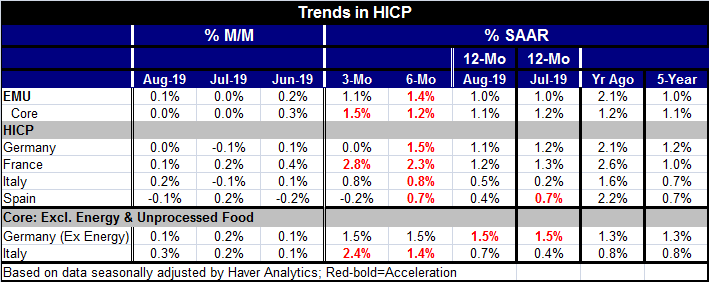

EMU inflation is subdued in August on the heels of flat headline and core prices in July. The headline HICP rose by 0.1% in August while the core rate was flat for the second month in a row.

EMU inflation is subdued in August on the heels of flat headline and core prices in July. The headline HICP rose by 0.1% in August while the core rate was flat for the second month in a row.

Despite clear weakness in prices, a headline that is up by only 1% over 12 months and a core rate that is up by only 1.1% over 12 months, core inflation has been, in fact, accelerating in the EMU. It is up at a 1.2% annual rate over six months and at a 1.5% annual rate over three months. While the 12-month results look weak, they are in fact exactly what the five-year AVERAGE has been for headline and core price increases in the euro area.

By country (among the four largest members), the HICPs saw the largest monthly gain for August in Italy with a 0.2% increase and the weakest as a 0.1% decline in Spain. Over three months, all annualized inflation rates for Germany, France, Italy and Spain are below 1% except for France. Year-over-year France and Germany have HICP inflation rates of 1.2% and 1.1%, respectively. Italy and Spain have rates of 0.5% and 0.4%, respectively.

Only Italy reports core inflation early. Its core rise is 0.3% in August and it shows a progression of core inflation rising by 0.7% over 12 months, at a 1.4% pace over six months and at a 2.4% pace over three months. For Germany, we present an ex-energy metric. It is up by 0.1% in August and sequentially remains dead steady at a pace of 1.5%.

Inflation in the EMU clearly is undernourished. Price weakness is persistent across the EMU. And the undershooting is significant with inflation running at about half the targeted pace and having averaged that low for a five-year period. The graph shows how inflation has tended to flare on occasion but has not been successful at sustaining a 2% increase. Since 2013, these three countries have only had a passing acquaintance with inflation.at 2%.

And the future is difficult. The U.S.-China trade war is continuing to spin out global weakness as collateral damage. Germany’s spurt in retail sales in June came undone in July. Italy’s GDP in Q2 is unrevised and remains flat on the quarter. The EuroCOIN indicator of activity fell in August. There are also some positive data developments, but there is enough weakness to make it clear that inflation is not being pushed up by domestic activity anytime soon. Meanwhile, the global picture is still a net-negative. The table, clearly, is well-set for more ECB stimulus for the EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates