Global| Jan 23 2008

Global| Jan 23 2008European Orders Surprise with a Spurt in November

Summary

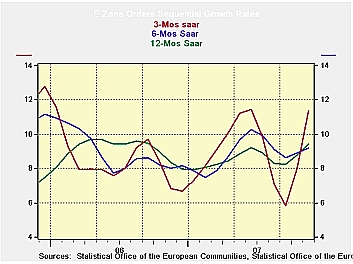

With various country indices showing slowing the EMU orders aggregate for November rose and was surprisingly strong showing a gain of 2.7% following a rise of 2.5% in Oct. Two months into Q4 data show total MFG orders rising at a [...]

With various country indices showing slowing the EMU orders

aggregate for November rose and was surprisingly strong showing a gain

of 2.7% following a rise of 2.5% in Oct. Two months into Q4 data show

total MFG orders rising at a 17.6% annual rate. Domestic MFG orders in

the zone are up at a 13.8% pace while foreign orders are up at a 26.5%

pace. In Q4 German orders through November are up at a 28% pace while

in France, Italy and the UK results are much worse. French orders are

rising at a 1.2% annual rate, in Italy the pace is 7.1%. In the UK

industrial orders are dropping at a 31% annual rate in Q4.

Clearly the EU/EMU is seeing a great deal of irregularity

among members. Still, in January the ECB remains pre-occupied by

inflation risk and is not following the Fed in its rate-cutting

program. The orders data seem to confirm that there remains a core of

strength within the Euro Area but, at the same time we can wonder how

widespread it is and long lived it will be.

| E-zone-13 and UK Industrial Orders And Sales | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Nov-07 | Oct-07 | Nov-07 | Oct-07 | Nov-07 | Oct-07 | ||

| Ezone Detail | Nov-07 | Oct-07 | Sep-07 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Manufacturing Orders | 2.7% | 2.5% | -1.2% | 17.4% | 9.4% | 13.0% | 10.0% | 11.7% | 8.3% |

| Manufacturing Sales | -- | 0.1% | -0.2% | -- | -0.5% | -- | 3.7% | -- | 5.6% |

| Consumer Goods | -- | 0.2% | 0.2% | -- | 3.2% | -- | 4.1% | -- | 4.1% |

| Capital Goods | -- | 0.5% | 0.5% | -- | 6.8% | -- | 7.1% | -- | 8.1% |

| Intermediate Goods | 1.6% | 4.2% | -3.0% | 11.1% | 2.5% | 10.7% | 8.4% | 10.6% | 7.1% |

| Memo: MFG | |||||||||

| Total Orders | 2.7% | 2.5% | -1.2% | 17.4% | 9.4% | 13.0% | 10.0% | 11.7% | 8.3% |

| E-13 Domestic MFG orders | 1.6% | 4.2% | -3.0% | 11.1% | 2.5% | 10.7% | 8.4% | 10.6% | 7.1% |

| E-13 Foreign MFG orders | 3.9% | 2.4% | 0.0% | 27.8% | 18.6% | 14.8% | 13.5% | 13.6% | 11.2% |

| Countries: | Nov-07 | Oct-07 | Sep-07 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo |

| Germany (MFG): | 4.1% | 4.0% | -2.0% | 26.8% | 15.7% | 13.3% | 9.8% | 14.0% | 10.1% |

| France (Ind): | -0.2% | 2.4% | -2.5% | -1.3% | -4.5% | 2.7% | 7.9% | 7.9% | 6.4% |

| Italy (Ind): | 3.6% | -0.5% | 0.6% | 15.8% | -2.9% | 11.0% | 8.4% | 10.4% | 6.2% |

| UK (Engineering Ind): | -0.6% | -0.7% | -4.9% | -22.5% | -46.9% | 0.7% | 0.3% | 2.6% | 4.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates