Global| Oct 12 2007

Global| Oct 12 2007French Inflation Turns Higher But Not Really...

Summary

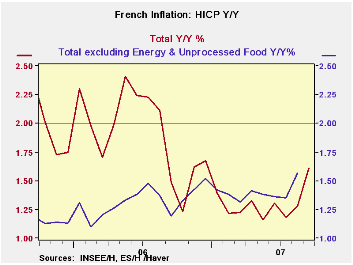

The graph on the left paints a clear picture of French inflation turning higher in September 2007.And year/year inflation did just that. Yet inflation in France is not really accelerating. The year/year jump is due to an adverse base [...]

The graph on the left paints a clear picture of French inflation turning higher in September 2007.And year/year inflation did just that. Yet inflation in France is not really accelerating. The year/year jump is due to an adverse base effect - the fact that a year ago inflation had fallen making this month’s year/year a tougher comparison. When we instead look at 3-month inflation compared to 6-month inflation we see that the rate of inflation is back down from 2.7% to 1.8%.. Diffusion calculations also confirm that inflation remains under wraps. Diffusion calculates the percentage of main sectors in which inflation has accelerated in a period. What we find is that for the 3-month to 6-month inflation comparisons diffusion is 27.3 which is below the neutral level of 50. Indeed at this level we can see that inflation is in fact decelerating in many more sectors than it is accelerating. Inflation in France seems under control despite the unfortunate accompanying chart.It is more unfortunate that the chart is the main way that inflation watchers view inflation.

The graph on the left paints a clear picture of French inflation turning higher in September 2007.And year/year inflation did just that. Yet inflation in France is not really accelerating. The year/year jump is due to an adverse base effect - the fact that a year ago inflation had fallen making this month’s year/year a tougher comparison. When we instead look at 3-month inflation compared to 6-month inflation we see that the rate of inflation is back down from 2.7% to 1.8%.. Diffusion calculations also confirm that inflation remains under wraps. Diffusion calculates the percentage of main sectors in which inflation has accelerated in a period. What we find is that for the 3-month to 6-month inflation comparisons diffusion is 27.3 which is below the neutral level of 50. Indeed at this level we can see that inflation is in fact decelerating in many more sectors than it is accelerating. Inflation in France seems under control despite the unfortunate accompanying chart.It is more unfortunate that the chart is the main way that inflation watchers view inflation.

The table below shows the diversity in French inflation trends with one main thing in common: that inflation is mostly decelerating at least from 6 months to 3 months.Year-over-year, most sectors confirm that inflation IS higher although the headline is barely higher at 1.6% compared to 1.5% a year ago.

| France HICP and CPI details | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Sep-07 | Aug-07 | Jul-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.1% | 0.3% | 0.0% | 1.8% | 2.7% | 1.6% | 1.5% |

| Core | #N/A | 0.3% | 0.0% | #N/A | #N/A | #N/A | 1.2% |

| CPI | |||||||

| All | 0.0% | 0.3% | 0.1% | 1.6% | 2.4% | 1.5% | 1.3% |

| CPI ex F&E | 0.1% | 0.4% | 0.1% | 2.2% | 2.2% | 1.5% | 1.3% |

| Food | 0.6% | 0.7% | -0.2% | 4.8% | 5.0% | 1.3% | 2.7% |

| Alcohol | 0.7% | 2.9% | 0.3% | 16.5% | 10.2% | 3.9% | 0.3% |

| Clothing & Shoes | 0.4% | 0.3% | -0.7% | -0.2% | 0.3% | 0.9% | 0.2% |

| Rent & Utilities | 0.3% | 0.1% | 0.2% | 2.5% | 3.5% | 2.7% | 3.8% |

| Health Care | 0.1% | 0.1% | 0.4% | 2.5% | 0.7% | 0.3% | 0.2% |

| Transport | 0.1% | -0.4% | 0.2% | -0.5% | 3.0% | 2.4% | 0.6% |

| Communication | 0.2% | 0.5% | 0.0% | 2.8% | 0.7% | 0.2% | -6.2% |

| Recreation & Culture | -0.7% | -0.1% | -0.2% | -3.8% | -1.8% | -1.5% | -1.6% |

| Education | -0.1% | 0.1% | 0.2% | 0.9% | 1.7% | 2.1% | 2.6% |

| Restaurant & Hotel | -1.0% | 0.8% | 0.5% | 1.3% | 2.3% | 2.8% | 2.3% |

| Other | 0.2% | 0.1% | 0.0% | 1.3% | 2.0% | 1.9% | 3.2% |

| Diffusion | 27.3% | 63.6% | 63.6% | ||||

| Type: | Diffusion Compared to | 6-mo | 12-mo | Yr-Ago | |||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates