Global| Dec 27 2013

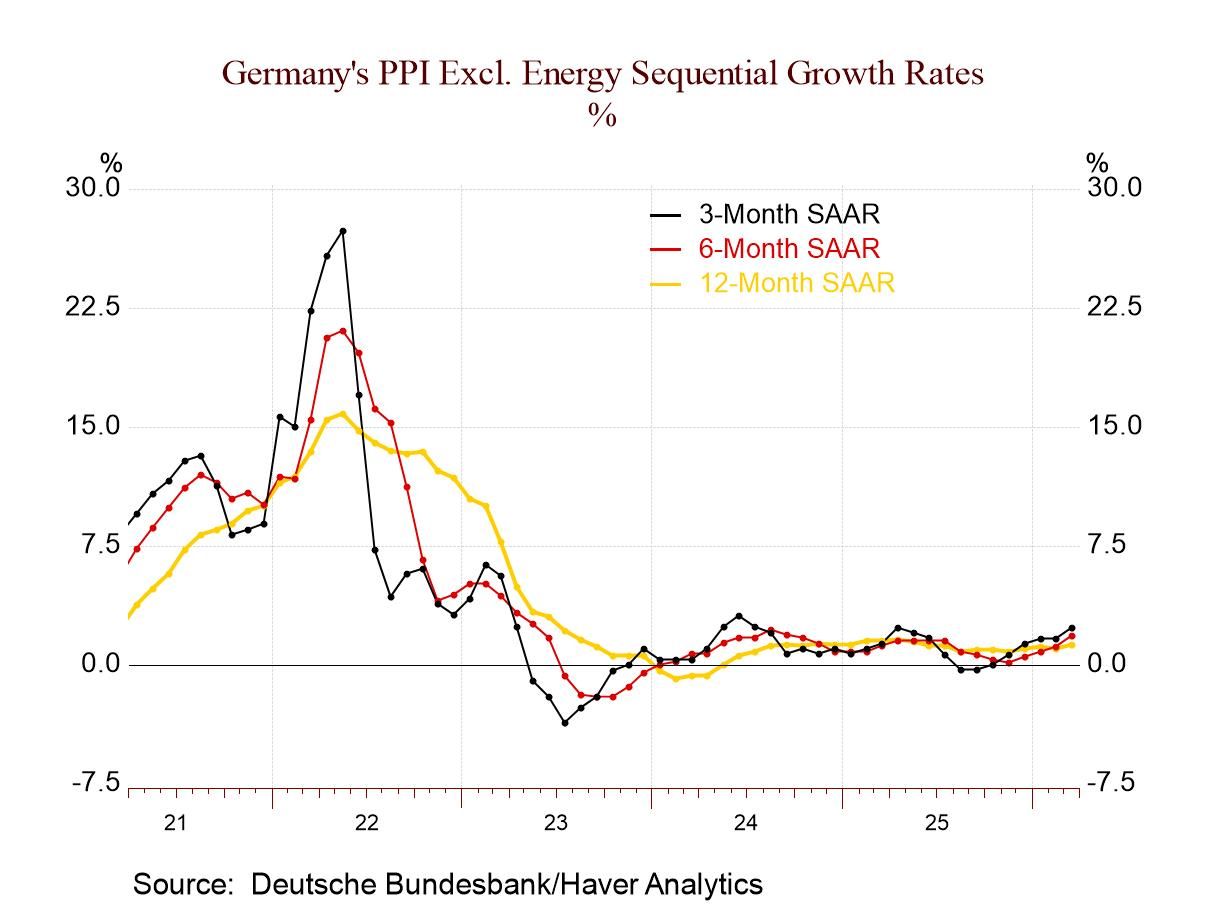

Global| Dec 27 2013French PPI Components Are Mixed

Summary

As we wonder how much strength is built in the European Monetary Union, France is showing some rebound in PPI prices in November. However, price trends in France do not give us a clear picture of activity trends. Such associations are [...]

As we wonder how much strength is built in the European Monetary Union, France is showing some rebound in PPI prices in November. However, price trends in France do not give us a clear picture of activity trends. Such associations are only indirect in any case. But the ongoing price weakness in France, Europe and the United States, to name a few, has been taken as a symptom of weak demand, not just low inflation.

As we wonder how much strength is built in the European Monetary Union, France is showing some rebound in PPI prices in November. However, price trends in France do not give us a clear picture of activity trends. Such associations are only indirect in any case. But the ongoing price weakness in France, Europe and the United States, to name a few, has been taken as a symptom of weak demand, not just low inflation.

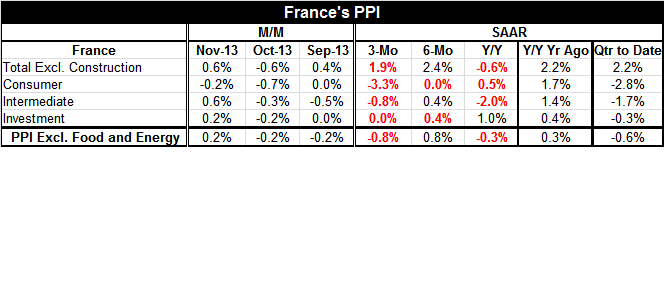

For France, price trends across sectors are mixed trends. Overall PPI prices have fallen in only one of the last three months. But for consumer goods and intermediate goods prices each have fallen in two of the past three months. The core PPI has fallen in two of the last three months as well.

The overall PPI, excluding the impact of the construction sector, is showing more strength than the sector components. Still, the headline is decelerating form six months to three months, but it is also expanding. It is, however, still lower on balance over 12 months. Consumer goods prices are still on a weakening trend. But investment goods are steady at a low rate of increase. This configuration is in concert with the ongoing firmness in EMU manufacturing.

Among the components only intermediate goods, the category with the most raw materials, shows a 12-month net drop. But over six months all component trends are tempered. Over three months all sector trends are flat or lower.

On balance the price trends in France do not give us a sense that domestic demand is reviving and putting upward pressure on prices. Since recent price weakness affects more than just intermediate goods, there is still reason to wonder about the strength of demand in France. Still the trends do not show any new weakness...just the same old patterns.

It may be that manufacturing will pull Europe into recovery after all. In the United States, the same dynamic is in place as manufacturing is doing well while the service sector lags badly; thus, contributing less than half is usual push to GDP. The only problem with a manufacturing-led revival is that it is a revival without many jobs. Productivity is high in manufacturing and so output is achieved with little labor. This is exactly the kind of recovery that has been in place from the start. It is a recovery, but it is also limited.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief