Global| Oct 31 2013

Global| Oct 31 2013German Consumer Climate Edges Lower with Repercussions?

Summary

The GfK consumer climate survey that extrapolates a November figure for German confidence foresees a tailing off in consumer climate in Nov. The GfK components are not updated for the projected climate reading in November, so they lag [...]

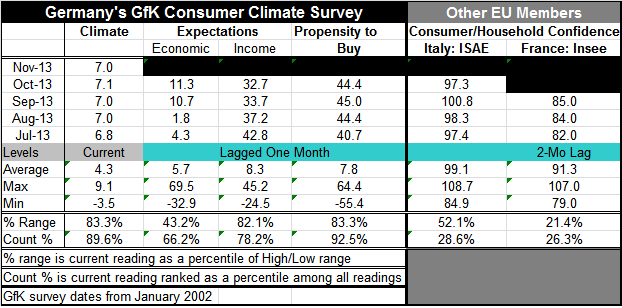

The GfK consumer climate survey that extrapolates a November figure for German confidence foresees a tailing off in consumer climate in Nov.

The GfK consumer climate survey that extrapolates a November figure for German confidence foresees a tailing off in consumer climate in Nov.

The GfK components are not updated for the projected climate reading in November, so they lag one month. But the indicators for income and buying propensities already had peaked and started lower. Income expectations peaked in July at a reading of 42.8 and have been rapidly losing ground ever since. The buying propensity had been moving higher until this month when it fell back from 45.0 to 44.4. It is the economic reading which has continued to surge higher, even in October. We cannot be sure what the shift in November is due to since we do not have component values for that month. But a decline is not really a surprise; except for the surging economic reading, the GfK components had already showed signs of exhaustion.

Still the German index is much better off than that for other EMU nations. The November Climate reading stands in the 89th percentile of its historic queue (count). This means it has been higher only about 11% of the time. The economic gauge stands in the 66th percentile of its queue, income stands in the 78th percentile of its queue and the buying propensity is in the 92nd percentile of its queue. From these assessments we can surmise that it is the economic index that has been surging and playing catch-up with the other metrics. The overall climate ranking is more in step with the rankings on income and buying than with the economy ranking.

When we compare these assessments with other EMU members, we find that over this same period from January 2002 to date, Italy's consumer metric stands only in the 28th percentile of its queue. France stands in the 26th percentile of its queue. German consumers are leagues ahead of other consumers in EMU.

It will be interesting to see if the German optimism is really going to start turning lower. European expectations have been lifted by the improved performance of the countries of Southern Europe and by Spain's emergence from recession. Still, it isn't at all clear what a setback in Germany would do to all this optimism. After all the German economy works off of export-led growth, not a phenomenon that helps to boost its neighbors.

In fact the US has just launched a criticism of the German model of export led growth in its semiannual report to Congress. Germany is already up in arms defending its system here.

But the fact is that demand is becoming increasingly scarce globally as formerly high consumption countries are pulling back as consumers are paying down debt and governments worldwide are becoming more debt-conscience, limiting their own spending. Countries whose national economics are geared to exploit that which is getting scare are bound to encounter criticism. In competitive markets a surplus country will find its currency is forced higher, diminishing its competiveness and causing its exports to slow. It follows that a country cannot have a policy of persistent export-led growth without manipulating exchange rate values.

In the case of Germany the exchange rate question becomes even more muddied since Germany is a highly competitive country whose currency should probably rise in value to diminish is export prowess (this will also increase German wealth and buying power-and eventually, German imports). But Germany is locked in a currency union with a lot of other nations with exactly the opposite problem!

This is simply another way to see the inconsistencies in EMU and to recognize that the rest of the world is not immune from the effect of the imbalances created within the eurozone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates