Global| Dec 06 2018

Global| Dec 06 2018German Orders Tick Higher in October; Trend Still Weak

Summary

Germany's factory orders in October rose instead of falling as expected, but the gain was only of 0.3% and it reflected widely different results on domestic vs. international orders. Foreign orders rose by 2.9% in October while [...]

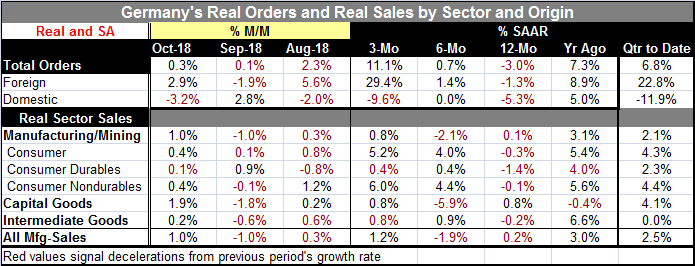

Germany's factory orders in October rose instead of falling as expected, but the gain was only of 0.3% and it reflected widely different results on domestic vs. international orders. Foreign orders rose by 2.9% in October while domestic orders plunged by 3.2%. These results left foreign orders on a three-month tear rising at a 29% annualized rate while domestic orders are falling over three months at a nearly 10% annualized rate.

Germany's factory orders in October rose instead of falling as expected, but the gain was only of 0.3% and it reflected widely different results on domestic vs. international orders. Foreign orders rose by 2.9% in October while domestic orders plunged by 3.2%. These results left foreign orders on a three-month tear rising at a 29% annualized rate while domestic orders are falling over three months at a nearly 10% annualized rate.

Still, over 12 months, both foreign and domestic orders are falling; foreign orders by 1.3% and domestic orders by 5.3%. Foreign orders, however, show an accelerating trend with growth stepping up over six months to a 1.4% pace then to the 29.4% spurt over three months. Domestic orders do not show a steady trend. They do improve from a 5.3% decline over 12 months to flat over six months but then they succumb to a 9.6% annual rate drop over three months, a faster drop than their 12-month pace of decline. It's fair to characterize German domestic and foreign orders as on opposite paths.

We see this in the QTD (quarter-to-date) growth rates as well with the composite for orders rising at a 6.8% annualized rate on the back of a 22.8% surge in foreign orders QTD as domestic orders are weak, falling at an 11.9% annualized rate QTD.

Sector sales

Real sales by sector show a much smoother path but still a rocky road for trend setting. Over 12 months, real sector sales are mostly falling across sectors with capital goods the exception. However, the headline is also up by just 0.1%. Manufacturing sales manage to gain by 0.2%. But at the sector level, consumer goods overall as well as consumer durables and nondurables show sales declines over 12-months. Intermediate goods sales fall by 0.2%. Capital goods log the only sizeable sector gain, one of 0.8%.

Trends

Momentum is a more complicated picture for sector sales. Consumer goods overall show acceleration in sales from 12-months to six-months and again to three-months. That is propelled by strength in durable goods sales. But capital goods and intermediate goods show decidedly mixed trends. The overall mining and manufacturing sales or simply manufacturing alone also show the cross currents of trends.

Sales trends reflect the chaos in orders trends despite the fact that the headlines for orders is accelerating. That acceleration is a technical one. It is on the back of accelerating foreign orders while domestic orders show mixed behavior. And that is what is reflected in real sales trends: chaos.

A broader view

These trends are consistent with recently released and now finalized Markit PMI readings. There the German factory sector slips from September to October to November. The average German PMI reading falls from its 12-month average to its six-month average to its three-month average. Clearly, there has been slowdown in place. And this is true of the overall EMU trends which are important to Germany as well as therein reside some important German customers.

The EMU is still slowing and Germany is slowing. The one-month uptick in German orders hardly reverses that trend. And the fact that the overall reading is the net of the confluence of two very differently behaved source of growth from domestic and foreign sources underlines its unpredictability.

So data trends cannot settle the matter as to future trends. But the politics of the future are grimmer with the EU now torn on several fronts. The British may be prepared to reject a Brexit deal- the Brexit deal. And instead of a hard-Brexit the U.K. may actually be willing to go back to the drawing board and vote again. It could be that the EU's hard bargaining has caused the U.K. to rethink the merits of its exit strategy altogether. But that would be the end of the good news and it is speculative at best. Less speculative are the circumstances of France and Italy. The yellow vest protests would seem to put France out of compliance with her budget promises. President Macron has rescinded the fuel taxes and has not replaced them while protests are certainly damaging growth and tax receipts in the aggregate. Macron himself may face a 'no confidence vote.' Meanwhile, in Italy the Five Star movement has agreed to some flexibility on its budget but not much at all. And with France falling out of compliance, the EU Commission has much more of a conundrum on its hands. At the same time, the message from the U.S. yield curve may be that a U.S. recession is nearer than everyone has been thinking. If that is so, then Europe will 'catch a cold' too and in all likelihood all budgets will fall out of compliance (except of course Germany's). So the EU Commission has some deciding to do. While these various events are unconnected, that does not make the EU Commission's decisions any easier.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates