Global| May 30 2008

Global| May 30 2008German Retail Sales by Sector

Summary

German retail sales are showing some real weakness in April. Nominal sales ex-autos are off by 1.3% in April and 1.7% in real terms. For the developing second quarter the results are grim. As of the first month of the new quarter the [...]

German retail sales are showing some real weakness in April.

Nominal sales ex-autos are off by 1.3% in April and 1.7% in real terms.

For the developing second quarter the results are grim. As of the first

month of the new quarter the growth rate of ex auto retail sales in

April over the Q1 base is at a minus 13.1% annualized growth rate for

nominal retail sales and -15.9% for inflation-adjusted retail sales.

The table shows a steady menu of negative growth rates over

all horizons from one year in, with the pace of declines getting more

or less progressively weaker.

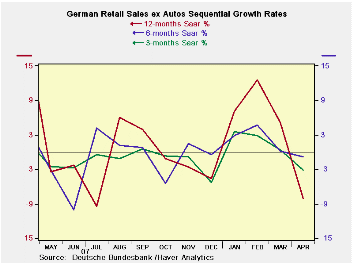

The chart shows that retail sales trends in Germany have been

volatile even though these series exclude auto sales which can be even

more volatile. The current month is turning trends sharply lower. April

is the second deeply negative month in a row. Weakness in March and

April offset what had looked like a strong gain in February sales. The

trends in Europe have been more consistently negative. Like in the US,

consumer readings in Germany and in Europe are generally among some of

the weakest in the entire economy. Weak retail sales keep this trend in

play.

| German Real and Nominal Retail Sales | ||||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Apr-08 | Mar-08 | Feb-08 | 3-MO | 6-MO | 12-MO | Yr Ago | QTR Saar |

| Retail Excl Auto | -1.3% | -2.2% | 1.4% | -8.1% | -0.8% | -3.1% | 1.7% | -13.1% |

| Food Beverage & Tobacco | -1.0% | -0.1% | 0.0% | -4.4% | -3.1% | -2.3% | 1.7% | -6.4% |

| Clothing footwear | 1.2% | -10.3% | 6.2% | -13.4% | -4.0% | -9.9% | 8.6% | -21.8% |

| Real | ||||||||

| Retail Excl auto | -1.7% | -2.2% | 1.0% | -11.3% | -3.9% | -5.6% | 0.9% | -15.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates