Global| Sep 30 2013

Global| Sep 30 2013German Retail Sales Fail to Excite

Summary

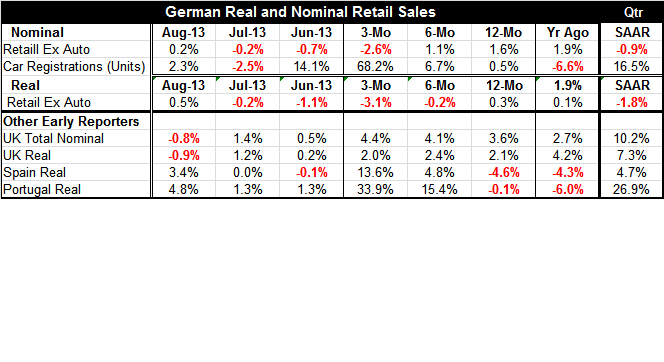

German retail sales are up in August in both nominal and in real terms. And, while auto registrations are building a head of steam, German retail sales excluding autos are still slogging ahead with little sign of any renewed [...]

German retail sales are up in August in both nominal and in real terms. And, while auto registrations are building a head of steam, German retail sales excluding autos are still slogging ahead with little sign of any renewed enthusiasm.

German retail sales are up in August in both nominal and in real terms. And, while auto registrations are building a head of steam, German retail sales excluding autos are still slogging ahead with little sign of any renewed enthusiasm.

Over three months both real and nominal retail sales are in Germany are dropping. Real sales are falling at a 3.1% annual rate. Two months into a new quarter real sales are falling at a 1.8% annual rate.

German retail sales did rise in August in both nominal and real terms. But the weakness in previous months has failed to take growth to the bottom line over time horizons out to three-months. German retail sales trend are surprisingly weak and faltering.

Real sales seem to be losing momentum instead of gaining. They are falling at a 3.1% annualized rate over three-months, and dropping at 0.2% annual rate over six months while up by just 0.3% over 12-months. Nominal sales are losing momentum with a similar progression.

Despite the surge in auto registrations and other up-beat data that are being quoted by the euro-optimists, German retail sales look dull and drab.

Elsewhere in the Zone and in the EU early reporters of retail sales are giving off mixed signals. In August real and nominal sales fell in the UK where economic data have generally been quite upbeat. In Spain and in Portugal, where growth has been absent, sales are up strongly in August. All three countries, however, show strong real sales in the quarter to date with UK sales up at a 7.3% annual rate, Spain's sales up at a 4.7% pace and Portugal's sales up at a 26.9% pace.

When it comes to consumer spending, Germany is not leading the parade. And that is why Germany must be seen as a sort of `island' EMU economy. It does not spin off a lot of positive impact. German's growth tends to be export-led and does not have coattails for the rest of EMU to ride. Germany may do well, but it is no locomotive for EMU. That's not how the German economy works. If the rest of EMU is going to recover, it will have to do it on its own.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates