Global| Nov 30 2016

Global| Nov 30 2016German Retail Sales Rebound Strongly; Still More Volatility Than Trend

Summary

German retail sales rebounded strongly in October, gaining 2.6% after a 1% decline in September. Even with two monthly drops in a row in August and September, the October rebound puts rates on a three-month growth track. But German [...]

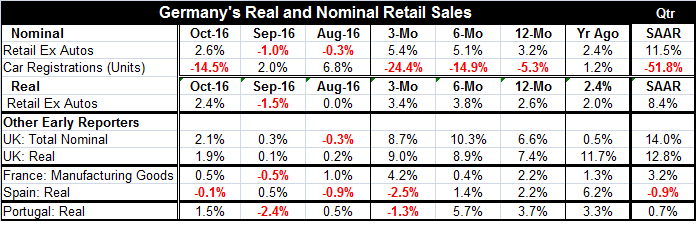

German retail sales rebounded strongly in October, gaining 2.6% after a 1% decline in September. Even with two monthly drops in a row in August and September, the October rebound puts rates on a three-month growth track. But German retail sales have been so volatile that it is still hard to discern a trend. Even with the strong readings for October, it is not clear that three-month, six-month and 12-month growth rates are not still locked in a downtrend.

German retail sales rebounded strongly in October, gaining 2.6% after a 1% decline in September. Even with two monthly drops in a row in August and September, the October rebound puts rates on a three-month growth track. But German retail sales have been so volatile that it is still hard to discern a trend. Even with the strong readings for October, it is not clear that three-month, six-month and 12-month growth rates are not still locked in a downtrend.

The sequential growth rates tell a more optimistic story but one that we know can easily be erased in the next month's report. Sales patterns are accelerating from 12-month to six-month to three-month. But real sales are not quite on that same upbeat profile as they show a slight six-month to three-month deceleration.

Quite separately auto registrations in Germany have been contracting and their contraction is sequentially more severe. Over 12 months they contract at a 5.3% pace, over six months the contraction pace steps up to -14.9% while over three months it is at a -24.4% annual rate. Registrations did put in two monthly gains in a row in August and September before collapsing in October. That kind of action makes trends hard to read.

However, in the quarter-to-date, German retail sales are up at an 11.5% pace and for real sales the pace is 8.4%. Auto registrations are still undergoing a severe contraction early in Q4. But since this quarterly calculation is based on positioning one month over the previous quarter's average and compounding the results, the actual growth rates are subject to great change as the rest of the quarterly data come in. This is essentially like a GDP NOW calculation where we take the current trend as gospel and do not try to guess any change in the trend for the rest of the quarter. It yields volatile results, but it is unbiased and free of judgment.

At the table, we survey other early retail sales reporters. The U.K., France and Portugal show sales gains in October with Spain showing a real sales decline but only one of -0.1% over three months. The U.K. and France post strong sales gains while Spain and Portugal log substantial three-month declines. However, on all other horizons, all the countries retail sales are increasing and usually on solid to strong rates of growth (France over six months is an exception with weak growth). In the quarter-to-date, only real sales in Spain show a decline; that is only at less than a -1% annual rate.

At the table, we survey other early retail sales reporters. The U.K., France and Portugal show sales gains in October with Spain showing a real sales decline but only one of -0.1% over three months. The U.K. and France post strong sales gains while Spain and Portugal log substantial three-month declines. However, on all other horizons, all the countries retail sales are increasing and usually on solid to strong rates of growth (France over six months is an exception with weak growth). In the quarter-to-date, only real sales in Spain show a decline; that is only at less than a -1% annual rate.

On balance, retail sales in key EMU countries and in the U.K. seem reasonably resilient if not strong. There is a great deal of volatility making it hard to tell if sales are changing speeds for real or not. However, in the recently released EU Commission indices, retailing was the top performing sector in the EMU area. The EU Commission retail diffusion readings for select EMU members are presented in a companion chart. France shows some softening, but the rest demonstrate firming.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates