Global| May 10 2007

Global| May 10 2007Inflation in Scandinavia Experiences Mild Swings; Taxes, Mortgage Rates Highlight Definition of "Core" Rates

Summary

CPI data reported today by the three Scandinavian countries illustrate well the reasons for monitoring both total inflation measures and "core" measures to determine the underlying trends. Moreover, the "core" measure applicable to an [...]

CPI data reported today by the three Scandinavian countries illustrate well the reasons for monitoring both total inflation measures and "core" measures to determine the underlying trends. Moreover, the "core" measure applicable to an individual country may vary from those used elsewhere, depending on the structure of each economy.

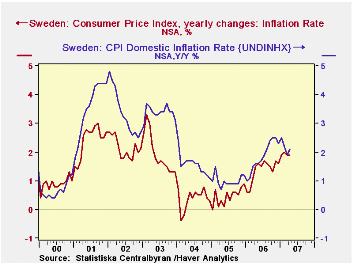

So in Sweden, we see the total CPI inflation rate at 1.9% over the 12 months through April, extending a generally increasing trend that began in early 2005. But apparently, the Swedes concentrate on another gauge, "UNDINHX", the so-called "domestic inflation rate". This index was 2.1% in April, but that's slower than it has been for the last six months. The grouping excludes home mortgage interest, some indirect taxes and goods that are mainly imported; this last would have the effect of omitting most fuel. Since last fall, interest rates have risen noticeably in Sweden while energy costs have slowed. Clothing prices have slowed and "other" prices have also eased. The rise in interest rates pushed up the total inflation rate, but the weaker inflation in other areas lowered the "domestic inflation rate".

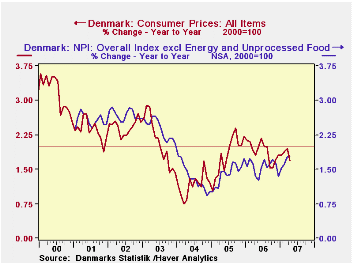

In Denmark, recent price movements have been fairly muted, and in general inflation is running pretty consistently at 1.7%-1.8%. The overall CPI was up 1.69% in April from April 2006. The favored version of the CPI in that country seems to be the NPI, "net price index", which nets out the impact of indirect taxes. In Haver's data offerings in the NORDIC database, values are given only for summary CPI categories, but net price indexes are available for numerous lower level line items. The total net price index was up 1.76% in April, year on year. Several "special groupings" are available; one seen in our chart alongside excludes energy and unprocessed food, a familiar concept of a "core" rate. This index was up 1.77% in April and has had a tendency toward firming. Home maintenance expenses, home furnishings and communications costs have been rising, in particular. Energy, as elsewhere, has been easing recently.

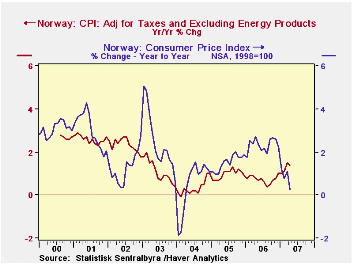

Norway reports very low inflation. Its overall CPI is up a mere 0.3% in the 12 months through April. And a rundown of the broad categories suggest a pretty mixed bag. Clothing prices, for example, are weak, while furniture and hotels and restaurants are up. If we exclude taxes, inflation is 0.9%, showing that reduced tax impact took 0.6% off April's inflation rate. Energy prices have been mixed, but have also pulled down on the inflation rate. Household heating and electricity have fallen, while auto-related expenses have increased. Overall, energy took 1.2 percentage points of the CPI. When the tax and energy effects both are netted out, the CPI was up 1.4% in April, still a low rate by world standards.

We see here that indirect taxes are important in these countries and that efforts to assess genuine "price" inflation, that is, what we would refer to as the "core" rate, require adjustment to remove the taxes. In the US, by contrast, a national VAT or GST is not in use and excise taxes play only a modest role. The main concern in this country is over volatile items where supply factors have a heavy weight, that is, food and energy. The countries discussed here net out mortgage interest costs. The UK also does this. The US eliminated those from the CPI nearly 25 years ago, substituting a "rental equivalence" measure for the direct input of interest charges. Japan, in another example of a varying definition of "core", now calculates two "core" rates, the original that excludes only fresh foods and a "Western" style that also excludes energy costs. The former remains the more popular. Thus, while it is convenient in some senses to have the European practice of "harmonized" inflation measures, it also continues to make just as much sense for each country to retain its own price index structure that fits the character of its own national economy.

| Apr 2007 | Mar 2007 | Feb 2007 | December/December||||

|---|---|---|---|---|---|---|

| 2006 | 2005 | 2004 | ||||

| Sweden: Inflation Rate | 1.9 | 1.9 | 2.0 | 1.6 | 0.9 | 0.3 |

| Domestic Inflation Rate (UNDINHX*) | 2.1 | 1.9 | 2.2 | 2.3 | 1.2 | 1.1 |

| Denmark: All Items | 1.7 | 2.0 | 1.9 | 1.8 | 2.2 | 1.2 |

| Net Prices ex Energy & Unprocessed Food | 1.8 | 1.8 | 1.6 | 1.3 | 1.7 | 1.0 |

| Norway: CPI | 0.3 | 1.1 | 0.8 | 2.2 | 1.8 | 1.0 |

| Adjusted for Tax / Excl Energy | 1.4 | 1.5 | 1.1 | 1.0 | 0.9 | 1.0 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates