Global| Jun 10 2014

Global| Jun 10 2014IP in France Makes Partial Recovery; Italy Nets a Gain

Summary

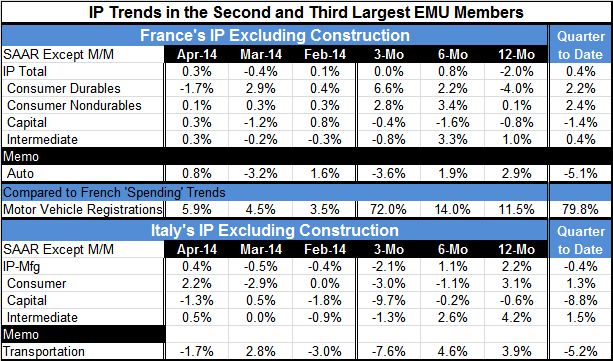

France saw its industrial production (IP) gain strongly in April, but it still did not fully shake off the drop in March. Italian IP is in the same boat in April as its 0.4% gain is less than its 0.5% drop in March. However, Italy has [...]

France saw its industrial production (IP) gain strongly in April, but it still did not fully shake off the drop in March. Italian IP is in the same boat in April as its 0.4% gain is less than its 0.5% drop in March.

France saw its industrial production (IP) gain strongly in April, but it still did not fully shake off the drop in March. Italian IP is in the same boat in April as its 0.4% gain is less than its 0.5% drop in March.

However, Italy has managed a year-over-year gain in IP while France has not. Italy's IP is up by 2.2% over 12-months while French IP is still lower by 2%.

French Trends: For overall IP, growth over 6-months and 3-months is stronger than over 12-months, perhaps a bit of progress is being made here despite some ugly headlines. French production trends show different results for different sectors. Consumer goods output is generally accelerating or improving from 12-months to 6-months to 3-months. There is acceleration for durable goods and improvement for nondurable goods. Capital goods output shows declines over all horizons, but (at least!) the growth rates are not getting progressive worse. Intermediate goods show a gain over 12-months, but erratic trends after that. In the quarter-to-date, French IP is up for all sectors except capital goods. While auto output is falling in the quarter-to-date, auto registrations are growing and accelerating sharply in the quarter.

Italian Trends: While Italy has the better year-over-year trend, its growth dynamics over one year are poor. Overall production trends are steadily deteriorating with the 12-month annual growth rate of 2.2% falling to 1.1% over six-months and deteriorating further to -2.1% over three months. With one minor exception, all the major categories show this pattern of sequential deceleration. Auto output is similarly decaying and shows a sharp drop in the quarter-to-date. Italy's overall IP is off in the quarter-to-date, but the sectors are mixed. Consumer and intermediate goods sector output is up, but capital goods output is off sharply.

For the euro area as a whole, nine members have reported IP results and all but one show gains month to month. Over three-months, Italy, the Netherlands and Greece show net output declines. Seven are showing improvement in their 12-month growth rates and report stronger growth rates compared to last month; France, Finland and Germany are exceptions.

The three biggest economies are still very slow-growing with Germany at 2.5%, France at 0% and Italy at 2.2% (all year-over-year). Spain, the fourth largest EMU member, has a 12-month growth rate of 5.1%, very impressive; however, its current IP level as a ratio to its cycle peak is 72% making it the second weakest reporting EMU member (Greece is the weakest) and putting its strong growth in a different light. This is catch-up growth. The average ratio of current to peak output among these reporting countries is 85%. Only Germany, the Netherlands, Ireland and Portugal are above it. Italy's ratio is 76%; France's is 83%

The overwhelming conclusion is that the euro area continues to grow. The year-over-year growth rates are still low, ranging from a very outsized 10.6% in Ireland to -1.1% in Greece. Neither of these rates is representative. When we look at underlying data, we only see growth acceleration from 3-months to 6-months in three of the six reporting members. Six of nine do accelerate from 12-months to 6-months. The good news is that the euro zone is growing and some of the weakest countries are catching up. Italy and France are still floundering.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates