Global| Nov 21 2016

Global| Nov 21 2016Japan's Trade Trends Edge Toward Improvement

Summary

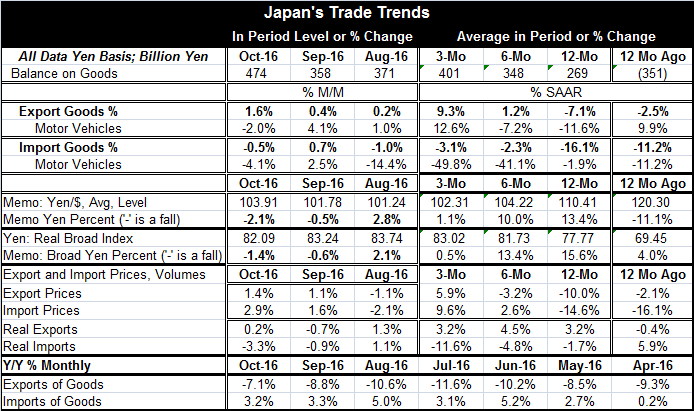

Japan's surplus is back in business and has given 12 positive readings in the last 12 months, making the return to surplus look like a lasting event. Japan's surplus position continues to make steadily higher despite the closure of [...]

Japan's surplus is back in business and has given 12 positive readings in the last 12 months, making the return to surplus look like a lasting event. Japan's surplus position continues to make steadily higher despite the closure of the bulk of its nuclear reactors and the added burden energy imports that are required under this protocol. Since the Tsunami hit and Japan began to have fears about its nuclear program, it has shuttered its reactors not just the damaged Fukushima reactor.

Japan's surplus is back in business and has given 12 positive readings in the last 12 months, making the return to surplus look like a lasting event. Japan's surplus position continues to make steadily higher despite the closure of the bulk of its nuclear reactors and the added burden energy imports that are required under this protocol. Since the Tsunami hit and Japan began to have fears about its nuclear program, it has shuttered its reactors not just the damaged Fukushima reactor.

Japan is making progress on exports as the growth of exports is steadily accelerating on the progression of 12-month to six-month to three-month horizons. Imports continue to demonstrate weak domestic demand as they are falling on all horizons. Imports are, however, less weak over three months than they are over 12 months.

In real terms, the trends shift slightly. On inflation adjusted terms, Japan's exports look steady instead of like they are accelerating. Export growth is in the range of 3% to 4.5% on three-month through 12-month horizons.

Expressed in real terms, imports are getting weaker. Real imports are down at a 1.7% pace over 12 months. But annualized import growth is at a -4.8% pace over six months and a -11.6% pace over three months; the decline is accelerating.

Over the last year, the yen has been in motion. It is stronger by 13.4% against the dollar over 12 months and rising at just a 1.1% annualized pace over three months. The yen has made roughly the same movements on a broad inflation-adjusted basis as well. The 'real' yen exchange rate has been rising and that will give exports a headwind and imports a tail wind. Still, Japan's domestic demand is so weak that imports still are not increasing.

Domestic demand and output

Domestic demand and output

Japan's sector indices tell a good deal of the story of Japan's demand weakness. When sector output is weak, income growth is weak and consumption will be weak. The construction sector is showing some life but remains off peak. The mining and manufacturing sector lags and shows only the smallest tendency to improve from what have been weak readings. The tertiary or services index is expanding but on a very weak gradient. The services index has been stronger - and this is looking at index levels not at rates of growth - about 32% of the time comparing current readings to past performance. Mining and manufacturing has been stronger 75% of the time, marking this sector as exceptionally weak. The construction sector has been stronger about 25% of the time. Mining and manufacturing on the PMI framework is showing expansion but not a very robust expansion. The weak standing of the sector index tells the right story and it is not encouraging.

With such weak sectors and flagging population growth, Japan does not have a vibrant domestic economy. The rising yen makes the international economy a bit tougher in an international environment that already is difficult. Still, on balance, Japan's trade performance is helping out. Exports are growing and the deficit has turned to surpluses. Both of those factors augment Japan's growth. But so far, it has not been enough to get Japan's growth to turn the corner or to ignite inflation to hit the target set by the Bank of Japan.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief