Global| Mar 14 2007

Global| Mar 14 2007Major Increase in Mortgage Delinquencies in Q4; Rate of Foreclosures Started Hits a Quarterly Record

Summary

A notable catalyst for yesterday's stock market sell-off was the quarterly mortgage delinquency report from the Mortgage Bankers' Association (MBA). It showed that 4.95% (seasonally adjusted) of all loans surveyed by MBA were past due [...]

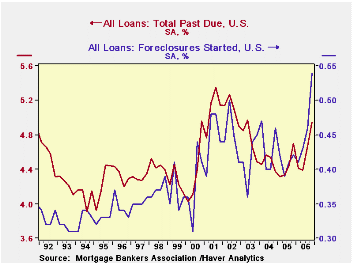

A notable catalyst for yesterday's stock market sell-off was the quarterly mortgage delinquency report from the Mortgage Bankers' Association (MBA). It showed that 4.95% (seasonally adjusted) of all loans surveyed by MBA were past due on December 31, an increase from 4.67% in September and the highest since September 2002. The foreclosure process was started on 0.54% of all loans, 0.08% more than during the previous quarter and a record high rate for a single quarter; at the end of December, 1.19% of loans were in foreclosure, up from 1.05% at end-September and 0.99% at the end of 2005. These rates are calculated on a total base of more than 42 million mortgage loans.

The MBA gives data on several types of mortgages: conventional prime, conventional subprime, FHA and VA. Each of these is further broken down by fixed and adjustable rate. Haver maintains these series in its specialized database MBAMTG and individual series are available on HaverSelect. The database includes seasonally adjusted data for the country as a whole and the four Census regions as well as not seasonally adjusted data for those areas plus the nine Census divisions, the 50 States, District of Columbia and Puerto Rico.

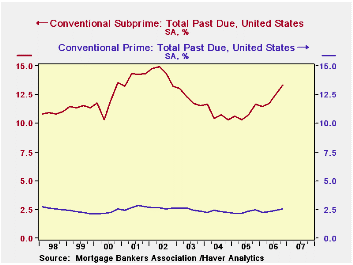

Delinquencies worsened for all major loan types. Conventional prime loans, which constitute 76.6% of the total market, had loan payments over due 30 days or more increase from 2.52% to 2.79% of the loans in that segment. Conventional subprime delinquencies rose from 12.95% to 14.27%. "Conventional" loans are those not insured by the federal government, such as FHA or VA. Conventional loans may be insured by private mortgage insurance or not insured at all. "Subprime" loans are those granted to borrowers with risky credit ratings or with excessively generous lending terms, such as loan-to-value ratios ("LTV") near 100%, whereas "prime" mortgages typically see LTVs below 80% and average or higher credit quality in the borrower.

Delinquencies on FHA-backed loans affected 14.43% of those loans and foreclosures were initiated on 0.96%. VA-insured loans had a delinquency rate of 7.43% and a foreclosure rate of 0.36%.

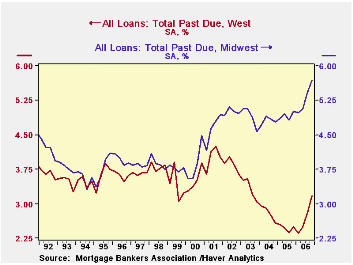

There are very large differences in delinquency experiences among the regions of the country. The Northeast had 4.58% of its loans past due in December, near the national average. But the Midwest and the South were both at about 5.7% and the West at 3.18%. So credit quality varies considerably around the nation.

| Mortgage Delinquencies (SA, %) | Q4 2006 | Q3 2006 | Year Ago | 2006 | 2005 | 2004 | 2001 |

|---|---|---|---|---|---|---|---|

| Total Loans Past Due | 4.95 | 4.67 | 4.70 | 4.61 | 4.45 | 4.48 | 5.11 |

| Foreclosures Started | 0.54 | 0.46 | 0.42 | 1.86 | 1.63 | 1.73 | 1.80 |

| Conventional Prime Loan Delinquencies | 2.57 | 2.44 | 2.47 | 2.39 | 2.29 | 2.30 | 2.67 |

| Conventional Subprime Loan Delinquencies | 13.33 | 12.56 | 11.63 | 12.27 | 10.84 | 10.80 | 14.04 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief