Global| Mar 21 2008

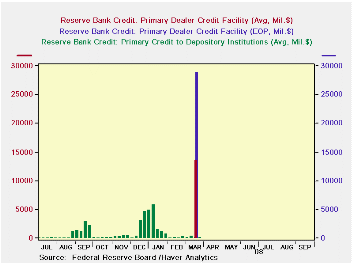

Global| Mar 21 2008Nonbank Dealers Borrow $29 Billion from the Fed

Summary

You can't say the Fed isn't trying. And if the current credit crisis situation turns into something far worse, it's unlikely that historians a generation from now will be able to blame the Fed's present efforts, as they can with the [...]

You can't say the Fed isn't trying. And if the current credit crisis situation turns into something far worse, it's unlikely that historians a generation from now will be able to blame the Fed's present efforts, as they can with the Great Depression. When various institutions have encountered troubles in recent months, the Fed has conjured a way to try to help them.

So it is that this week's H.4.1 release, the presentation by

the Fed of its own provision of credit to the economy, has new line

items. The indicator that years ago was known simply as "member bank

borrowing" is now a five-part section of the statement, with the latest

two added this week, "primary dealer credit facility" and the vaguely

titled "other credit extensions". The central bank's attempt last

summer to encourage borrowing largely fell on deaf ears; despite the

Fed's encouragement, few "depository institutions" wanted to be known

as accessing the old discount window. Some that did borrowed for 28

days, the period the Fed indicated it would favor, and then let the

loans run off. At the peak in early September, these loans averaged

$3.2 billion for the statement week ended Wednesday, September 12.

Year-end pressures brought some back in again from mid-December through

early January. Otherwise these loans were only frictional amounts. In

the week ended March 12, they averaged $103 million daily and there was

a total of just $27 million outstanding at the close of business that

Wednesday (that's million, with an "m").

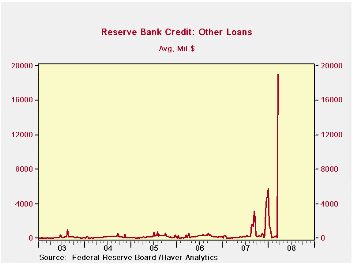

These loans covered just "depository institutions", that is,

banks and thrifts, which fund their activities from a base of customer

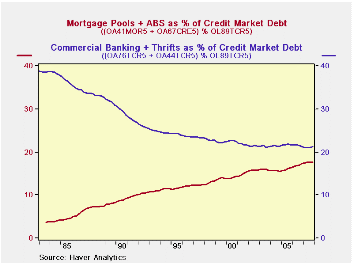

deposits. But as securitization has grown to cover more and more of the

US credit markets (see the graph from the Flow-of-Funds data), the

bank-oriented discount window safety value on the economy's finances

has become less and less relevant. The Fed, "the lender of last

resort", needed to be able to reach non-depository credit providers.

This week, it found one big way. The "primary dealer credit facility"

surged from $0 on Monday morning to $28.8 billion by Wednesday (that's

billion, with a "b"). No token borrowing here, clearly.

The mechanical workings of this facility appear to be very similar to the repo transactions the Fed does. Dealers offer various securities as collateral for an overnight loan of cash. The differences are that the loan comes at the dealers' initiative, not the Fed's, and the collateral is of the dealers' choosing, not the Fed's prescription. And there is a fixed rate, the "discount rate", rather than the competitive auction-type proceeding the Fed conducts in its repos. So indeed, the Fed found it could essentially open the discount window to nonbanks. This got cash where it is needed in yet another example of the Bernanke approach of targeted responses to specific circumstances.

The Fed's H.4.1 release, "Factors Affecting Reserve Balances", is in Haver's WEEKLY database under the "Money and Banking" heading. Flow-of-funds data are in FFUNDS.

by Robert Brusca March 21, 2008

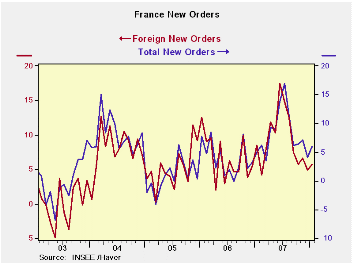

French industrial orders are hanging tough in an environment

where Euro Area growth is fading and the euro is getting stronger.

Total new orders and foreign orders are however losing some momentum

after spurting strongly in mid-2007 as the chart above shows. While off

peak and while showing some so-far short-lived downtrend, French

domestic and foreign orders are still at firm levels and slipping only

very gradually.

Despite Euro Area weakening, France has one of the higher NTC

MFG indices in the Zone, at 53.8 in February just short of Germany’s at

54.3. And, like Germany, France has seen its rate of unemployment over

the past year drop by more than one percentage point, faster than for

the Euro Area as a whole. On the face of it, France’s economy is still

doing well but household confidence is off sharply, MFG surveys show

weakening trends, business climate is off peak and has flattened out,

and the services sector climate index has been sliding. With France we

must be aware that some of the recent trends that can be viewed a still

firm exist in an environment where other survey responses seem to show

relatively more concern and more slippage.

| French Orders | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Jan-08 | Dec-07 | Nov-07 | 3-mo | 6-mo | 12-mo |

| Total | 3.1% | -2.1% | -0.2% | 3.0% | -2.7% | 5.9% |

| Foreign | 3.3% | -0.9% | 1.8% | 18.0% | 5.1% | 5.8% |

by Robert BruscaMarch 21, 2008

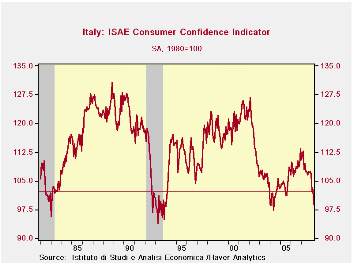

The chart on the left shows that consumer confidence has been weaker briefly in 2004 and then again back in 1994. But at the pace that confidence is falling it may be there soon. Italy’s Sentiment indicator is in the bottom 6% of its range since 1999 but it is not far from its recession low in 1994 and it is still plunging. A number of components are on lows for this period. In 1998 a number of the components cease to be available even though the headline and other component measures do go back further in time. Still, it is clear from the longer-horizon chart as well as from the shorter-horizon table that looks only at a recovery period that the current responses by survey participants are not much like those in expansion periods and are getting to look more like they do in downturns. Other Euro area countries may be more resilient but Italy is fighting to maintain its growth. Unemployment expectations are in the top 8% of where they have been since the start of 1999. The household past, current and future financial situations all are rated as the worst in this period since 1999. The overall situation is in the bottom 6%; only 17 percent of respondents think it’s a good time to make a major purchase. See the table, the percentile rankings are telling.

| Italy ISAE Consumer Confidence | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since January 1999 | ||||||||||

| Mar 08 |

Feb 08 |

Jan 08 |

Dec 07 |

%tile | Rank | Max | Min | Range | Mean | |

| Consumer Confidence | 99 | 102.8 | 102.2 | 106.7 | 6.1 | 108 | 127 | 97 | 30 | 111 |

| Last 12 months | ||||||||||

| OVERALL SITUATION | -84 | -76 | -79 | -69 | 0.0 | 111 | -22 | -84 | 62 | -55 |

| PRICE TRENDS | -17.5 | -18 | -23 | -21.5 | 40.8 | 61 | 4 | -32 | 36 | -15 |

| Next 12months | ||||||||||

| OVERALL SITUATION | -35 | -31 | -39 | -35 | 6.3 | 108 | 24 | -39 | 63 | -13 |

| PRICE TRENDS | 23 | 22 | 24.5 | 28 | 38.1 | 55 | 49 | 7 | 42 | 24 |

| UNEMPLOYMENT | 6 | 5 | -2 | 4 | 92.3 | 6 | 9 | -30 | 39 | -5 |

| HOUSEHOLD BUDGET | -2 | -3 | 1 | 9 | 2.8 | 110 | 33 | -3 | 36 | 14 |

| HOUSEHOLD FIN SITUATION | ||||||||||

| Last 12 months | -55 | -53 | -46 | -44 | 0.0 | 111 | -7 | -55 | 48 | -29 |

| Next12 months | -16 | -12 | -14 | -14 | 0.0 | 111 | 14 | -16 | 30 | -1 |

| HOUSEHOLD SAVINGS | ||||||||||

| Current | 54 | 61 | 53 | 60 | 79.1 | 11 | 63 | 20 | 43 | 39 |

| Future | -45 | -42 | -35 | -37 | 0.0 | 111 | -9 | -45 | 36 | -23 |

| MAJOR Purchases | ||||||||||

| Current | -50 | -44 | -42 | -47 | 16.7 | 89 | -15 | -57 | 42 | -40 |

| Future | -65 | -61 | -53 | -61 | 25.8 | 65 | -42 | -73 | 31 | -62 |

| Total number of months:111 | ||||||||||

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates