Global| Aug 21 2008

Global| Aug 21 2008Philadelphia Fed Index: Less Weakness

Summary

The Philadelphia Federal Reserve Bank reported that its Index of General Business conditions in the manufacturing sector "recovered" somewhat in August to -12.7 from -16.3 in July. This was a bit more improvement than forecast by [...]

The Philadelphia Federal Reserve Bank reported that its Index of General Business conditions in the manufacturing sector "recovered" somewhat in August to -12.7 from -16.3 in July. This was a bit more improvement than forecast by market economists, who looked for -14.

The Philadelphia Fed constructs a diffusion index for total business activity and each of nine sub- indexes. The business conditions index reflects a separate survey question, though, not some weighted combination of the sub-indexes.

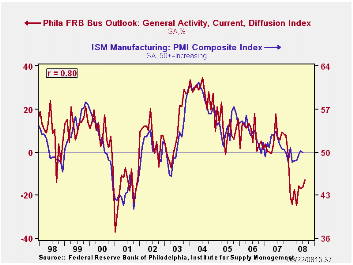

Market participants often monitor the Philadelphia Fed's General Activity Index as a hint about how the ISM survey will turn out for the same month. Indeed, there is an 80% correlation between the two indexes over the last 10 years and 74% over the life of the Philadelphia survey, since 1968. This relationship did break down in January (see graph), but the subsequent monthly trends have been similar. More broadly, during the last ten years the Philadelphia Index has held a 61% correlation with the three-month growth in industrial production for manufacturing. And there has been a 43% correlation with q/q growth in real GDP; however, until about 2000, that 10-year correlation was also around 60%. In all, this survey serves as a useful indicator of real activity, with the advantage of early timing in compilation and publication each month.

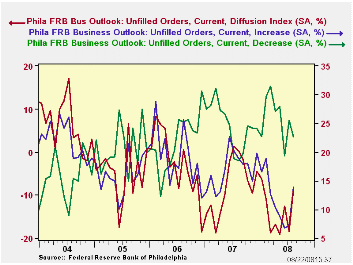

The new orders sub-index, at -11.9, maintained its general June level for a third month. This resulted from nearly equal increases in the number of companies reporting increases and decreases in new orders in August. The shipments index was noticeably less negative for this month, at -3.3 from -8.0 in July; the better showing came from less weakness, not more strength, as the number of companies with lower shipments fell 6 points and the number with higher shipments also fell, by 1.7 points. Unfilled orders had a -8.7 balance, compared with -18.3 in July, the net of an increase of 6.8 points in the share of companies with larger backlogs and a decrease of 2.9 points in those with smaller ones.

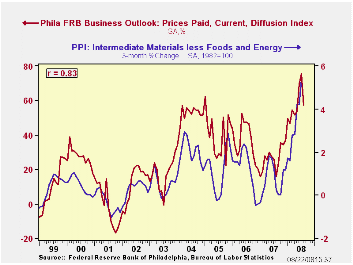

The prices paid index came down markedly to 57.5 from July's 75.6; the number of companies paying higher prices fell by 11.1 points, the largest monthly decrease in three years. The proportion of companies paying lower prices for materials rose from 0.9% to 7.9%; while this is a low absolute figure, it is higher than the 7.0% 20-year average for the proportion of firms enjoying price declines. During the last ten years there has been a 67% correlation between the prices paid index and the three-month growth in the intermediate goods PPI. There has been an 82% correlation with the change in core intermediate goods prices.

The separate index of business conditions expected in six months recovered to 27.6 after July's decline to 18.0. Here again, however, it was less a case of outright gain and more that fewer companies reported declines.

| Philadelphia Fed (%) | August | July | June | August '07 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| General Activity Index | -12.7 | -16.3 | -17.1 | 5.7 | 5.1 | 8.1 | 11.5 |

| Prices Paid Index | 57.5 | 75.6 | 69.3 | 16.0 | 26.4 | 36.6 | 40.1 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates