Global| Feb 04 2008

Global| Feb 04 2008PPI Main Sector Trends Still Excessive But Lose Some Momentum

Summary

PPI Trends. PPI trends are accelerating for the headline measure as well as for key country level headlines for inflation.In the Euro area inflation continues to flare for energy and for MFG goods more generally. Capital goods [...]

PPI Trends.

PPI Trends.

PPI trends are accelerating for the headline measure as well

as for key country level headlines for inflation.

In the Euro area inflation continues to flare for energy and

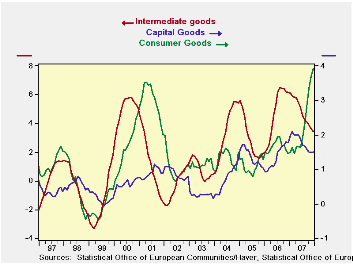

for MFG goods more generally. Capital goods inflation has remained

subdued at a low of 1.5% Yr/Yr pace. Consumer goods inflation has

backed off its highs but is still strong at 3.9% Yr/Yr. Intermediate

goods inflation has worked its way lower as well. Inflation ex-energy

has come back down to 2.1%, just a small step over the 2% rate that the

ECB has set as its overall inflation ceiling for the Euro area-wide

HICP. In that respect inflation is beginning to behave. Once energy

prices stop boosting headline inflation there is every reason to

believe that the overall rate will revert to the core.

By country…

For Germany, Italy and France, while headline inflation is

clearly over the top, ex-energy inflation shows hopeful trends, for

Germany and Italy, ex-energy inflation is at a 1.4% pace over three

months and is below the 2% over the three- and six-month horizons. In

France, the ex-energy inflation rate is at 2.2% above the 2% headline

ceiling pace but in a mode of deceleration.

The UK shows that over the top inflation is still

accelerating. At 3.6% ex-energy inflation is over the top as well and

roughly stable at that pace making the BOE’s task difficult.

Summing up

On balance there is reason for some optimism since the ex-energy measures are in better shape than the headline inflation rates, except for the UK. Ex-energy rates are decelerating as well and in the case of Germany and Italy they already are well below the 2% top-allowable pace for inflation generally. This progress may be enough to keep the ECB on hold and waiting for these core trends to take root. In time it should dominate the now higher headline rates of inflation across the Euro area nations as oil prices settle lower in the wake of the global slowing in growth.

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Ezone-13 | Dec-07 | Nov-07 | 3-Mo | 6-Mo | Yr/Yr | Y/Y Yr Ago |

| Total excl Constructions | 0.1% | 0.9% | 6.8% | 4.9% | 4.3% | 4.1% |

| Excl Energy | 0.1% | 0.1% | 2.1% | 2.5% | 3.1% | 3.4% |

| Capital Goods | 0.1% | 0.0% | 0.9% | 1.0% | 1.5% | 1.8% |

| Consumer Goods | 0.3% | 0.3% | 4.8% | 5.3% | 3.9% | 1.5% |

| Intermediate & Capital Goods | -0.1% | 0.0% | 0.7% | 1.0% | 2.7% | 4.4% |

| Energy | 0.1% | 3.4% | 23.2% | 13.0% | 8.3% | 6.2% |

| Manufacturing | 0.0% | 0.8% | 5.3% | 4.3% | 4.7% | 2.9% |

| Germany | -0.1% | 0.8% | 4.8% | 2.7% | 2.5% | 4.4% |

| Germany excl Energy | 0.0% | -0.1% | 1.4% | 1.4% | 2.2% | 2.9% |

| France | 0.2% | 0.8% | 6.8% | 5.6% | 4.5% | 2.7% |

| France excl Energy | 0.2% | 0.1% | 2.2% | 3.1% | 3.0% | 2.8% |

| Italy | -0.1% | 1.1% | 6.4% | 5.4% | 4.6% | 5.2% |

| Italy excl Energy | -0.1% | 0.2% | 1.4% | 1.9% | 3.0% | 4.2% |

| UK | 0.5% | 2.9% | 23.8% | 15.2% | 4.0% | 0.4% |

| UK excl Energy | 0.3% | 0.2% | 3.6% | 3.4% | 3.5% | 3.1% |

| E-zone 13 Harmonized PPI excluding Construction | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, | ||||||

| Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief