Global| Aug 27 2009

Global| Aug 27 2009Q2 GDP Unrevised on Net at 1.0% Fall; Hesitant Profits Recovery Continues

Summary

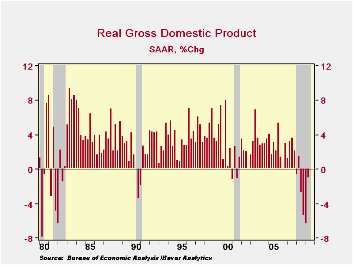

The pace of real GDP change was unchanged in today's report from the Commerce Department, which showed a 1.0% rate of decline. Inventories were revised lower but offset in the GDP tally by a smaller decline in domestic final sales and [...]

The pace of

real GDP change was unchanged in today's report from the Commerce

Department, which showed a 1.0% rate of decline. Inventories

were revised lower but offset in the GDP tally by a smaller decline in

domestic final sales and a larger push from net exports than were

reported in the July release. Notably, these latter two

revisions put total final sales up at a 0.4% rate, the first quarterly

increase in a year.

The pace of

real GDP change was unchanged in today's report from the Commerce

Department, which showed a 1.0% rate of decline. Inventories

were revised lower but offset in the GDP tally by a smaller decline in

domestic final sales and a larger push from net exports than were

reported in the July release. Notably, these latter two

revisions put total final sales up at a 0.4% rate, the first quarterly

increase in a year.

This GDP report marks the initiation of new nomenclature by the Commerce Department for the order of the GDP releases. Formerly, the "advance" report was followed by the "preliminary". Now the report after the "advance" is called "second release" and will be followed next month by the "third release". Surely this is an improvement for the last here, formerly known as "final", but which was revised soon enough yet again in annual and comprehensive revisions, so it was hardly "final".

Among categories of

demand, revisions were generally modest and favorable.

Consumer spending is now estimated to have fallen at a 1.0% annual rate

compared to 1.2% before and residential investment is down at a 22.8%

pace instead of  the 29.3% reported earlier. Exports were

revised to a 5.0% decline from 7.0% before, and government consumption

and gross investment was increased to 6.4% growth from 5.6%.

On the downside, nonresidential investment was lowered to a 10.9% rate

of decline from 8.9% reported before, with the cut coming from

structures; equipment outlays were lifted a bit. Imports

remained down at a 15.1% rate, as goods imports were "more weak" and

service imports were "less weak".

the 29.3% reported earlier. Exports were

revised to a 5.0% decline from 7.0% before, and government consumption

and gross investment was increased to 6.4% growth from 5.6%.

On the downside, nonresidential investment was lowered to a 10.9% rate

of decline from 8.9% reported before, with the cut coming from

structures; equipment outlays were lifted a bit. Imports

remained down at a 15.1% rate, as goods imports were "more weak" and

service imports were "less weak".

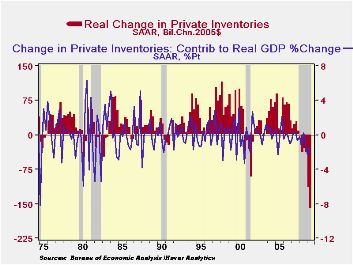

The inventory reductions are even more impressive than they were in the earlier report. Previously seen at $141.1 billion SAAR in chained 2005 dollars, the new data show them at -$159.2 billion. Every major stage of distribution cut stocks sharply: manufacturers, wholesalers and retailers. We often attribute such major adjustments to the auto industry, and it certainly participated, but durable and nondurable goods wholesalers and "other" retailers also reduced their merchandise on hand. This said, the contribution of inventory change to the GDP decline was not as severe, 1.4%, as it had been in Q1, 2.4%.

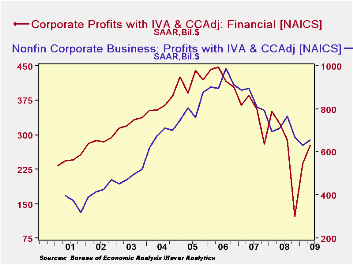

One

reason to cut inventories -- and labor forces, for that matter -- is to

cut costs. The performance of profits indicates that progress

has been made on this front. Corporate profits in Q2 rose

5.7% pre-tax, including IVA and CCAdj, from Q1 and were below Q2 2008

by "just" 10.9%. The year-to-year movement in Q1 had been

-19.0% with -25.1% in Q4. By broad sector, financial industries saw their quarterly profits gain 16.7% in

Q2 from Q1; they had nearly doubled from Q4 to Q1, gaining

95.1%. On a year-to-year basis, financial company profits are

still down, with Q2 at -14.3%; on this 4-quarter trend, profits have

declined continuously since Q3 2006. Nonfinancial company

profits have contracted less consistently, although they continued a

quarter-to-quarter decline in Q1, down 6%. Q2 saw a partial

reversal to an increase 4.5%. The year-to-year trend remains

down, by 7.7% in Q2; this has been negative since Q2 2007.

Thus, these operating profits are beginning to recover, but with such

hesitation that might not yet inspire much confidence.

sector, financial industries saw their quarterly profits gain 16.7% in

Q2 from Q1; they had nearly doubled from Q4 to Q1, gaining

95.1%. On a year-to-year basis, financial company profits are

still down, with Q2 at -14.3%; on this 4-quarter trend, profits have

declined continuously since Q3 2006. Nonfinancial company

profits have contracted less consistently, although they continued a

quarter-to-quarter decline in Q1, down 6%. Q2 saw a partial

reversal to an increase 4.5%. The year-to-year trend remains

down, by 7.7% in Q2; this has been negative since Q2 2007.

Thus, these operating profits are beginning to recover, but with such

hesitation that might not yet inspire much confidence.

The

U.S. National Income & Product Account data are available in

Haver's USECON and the USNA

databases.

| Chained 2005$, % AR | 2Q '09 (2nd Release) | 2Q '09 (Advance) | 1Q '09 | 2Q Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| GDP | -1.0 | -1.0 | -6.4 | -3.9 | 0.4 | 2.1 | 2.7 |

| Inventory Effect | -1.4 | -0.8 | -2.4 | -1.0 | -0.4 | -0.4 | 0.1 |

| Final Sales | 0.4 | -0.2 | -4.1 | -2.9 | 0.8 | 2.5 | 2.6 |

| Foreign Trade Effect | 1.6 | 1.4 | 2.6 | 0.9 | -1.2 | 0.8 | 0.1 |

| Domestic Final Demand | -1.2 | -1.5 | -6.4 | -3.8 | -0.4 | 1.7 | 2.5 |

| Chained GDP Price Index | 0.0 | 0.2 | 1.9 | 1.5 | 2.1 | 2.9 | 3.3 |

by Robert Brusca August 27, 2009

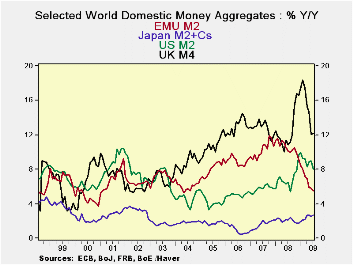

The chart exhibits growth rates for money presented in

national currency terms for several key countries. The table produces

the same data with some different horizons for calculation. In the

chart’s lower panel, the various series are inflation-adjusted (real

balances).

Monetary expansions looks too strong - The

picture on Yr/Yr money growth is a bit frightening. Japan’s growth rate

for M2 plus CD’s, its preferred monetary measure, is at 2.7% and is

quite contained. EMU’s rate at 5.5% seems high for its current growth

state. At 8.1% and 12% respectively the US and the UK seem to have

flooded their respective markets with liquidity. And in some ways they

have.

Or is it decelerating too much? But if you

turn your attention to the table instead of the chart you see a second

phenomenon is in play. Money growth rates are and have been

decelerating greatly from 12-months to 6-months and from 6-months to

3-months. In addition we provide some credit measures for EMU and they

have the same properties.

Weak once inflation adjusted - Next if we

turn to the lower panel of the chart to focus on the inflation adjusted

flows there, we find a marked deceleration is in place and that

monetary growth appears to be much less aggressive than it seems on the

broader 12-month horizon and in a nominal framework.

EMU - In EMU 3-Month growth rates for

money are at 2% while credit to residents is rising in real terms at a

1% rate and loans are shrinking by nearly 1% in real terms.

US and UK: Despite double-digit 12-month

growth rates in both the US and the UK each has real money balances

shrinking over three months.

Japan: Only Japan has relatively stable

nominal rates of growth for money and a slightly expanded growth rate

for real money balances over three months.

Policy confusion: All this just adds to the

confusion about policy. Is it tight or is it loose? Is it as loose as

it seems over 12 months or is it being tightened too rapidly as the

3-month trend seems to say? What about extracting ourselves from this

overtly stimulative period? Is there inflation risk and can the central

banks handle it?

Crosscurrents -On balance we see lots of

opinions but few good ways to make a clear discriminating argument. We

prefer to point out that the situation is complicated and in flux. We

urge investors to weigh the issues and we believe that where you come

down on the central bank issue depends on if you have trust in the

central bank/bankers or not. We do not think that the data are very

clear or that any course of action is baked in the cake. We see the

excessive money growth followed by some too-hard squeezing as evidence

that the central bankers are managing the risks – or trying to do so.

After all, the Yr/Yr money supplies are bloated but that is what the

bankers did to help blunt the crisis. It is in the past. To balance

that we do not see explosive sequential growth rates for money, quite

the opposite. We do not think this is a coincidence. Just as we are

monitoring these flows, so the central bankers are monitoring the

economy and the monetary trends. The data in the table are good

remainders to be careful about only looking at Yr/Yr growth rates. That

Yr/Yr growth in US and UK money supplies looks a lot different when you

shorten the growth horizon and deflate the flows to adjust for the

effects of inflation.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit: Residents |

Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 1.8% | 0.6% | -1.1% | 3.2% | 3.1% | 2.7% | 171.5% |

| 6-MO | 2.7% | -0.8% | -1.9% | 2.7% | 2.4% | 3.4% | 136.3% |

| 12-MO | 5.5% | 3.0% | 0.9% | 8.1% | 12.1% | 2.7% | -52.0% |

| 2-Yr | 7.8% | 7.0% | 5.1% | 7.3% | 11.5% | 2.4% | -6.6% |

| 3-Yr | 8.8% | 8.4% | 6.9% | 6.8% | 12.1% | 2.3% | -4.7% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 2.0% | 0.9% | -0.8% | -0.2% | -0.6% | 5.1% | 162.5% |

| 6-MO | 2.5% | -1.0% | -2.1% | 0.5% | -0.9% | 4.7% | 131.3% |

| 12-MO | 6.2% | 3.7% | 1.6% | 10.1% | 10.2% | 4.9% | -51.1% |

| 2-Yr | 6.1% | 5.3% | 3.3% | 5.5% | 8.2% | 2.4% | -8.2% |

| 3-Yr | 7.0% | 6.6% | 5.1% | 4.8% | 9.2% | 2.3% | -6.5% |

| Japan CPI for July is an estimate; it uses the June value to produce the real balance figure | |||||||

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates