Global| Sep 27 2019

Global| Sep 27 2019The Euro Dynamic: Where Is It Going?

Summary

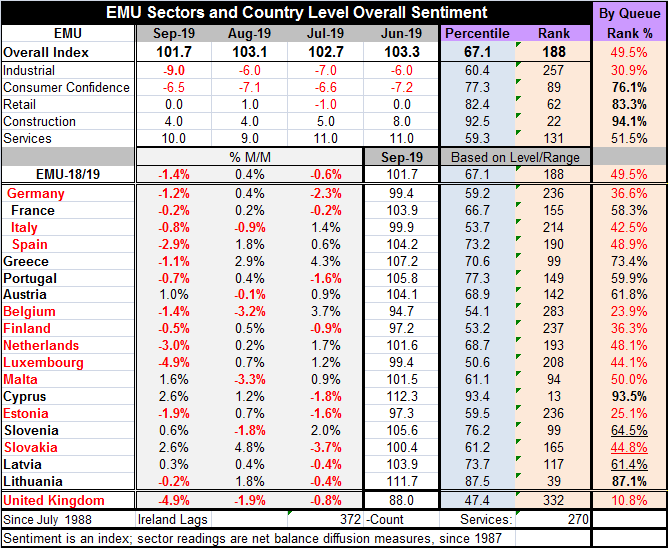

The EU Commission index for the European Monetary Union countries has fallen to 101.7 in September from 103.1 in August. At this mark, the index has a 49.5 percentile standing on data back to late-1988. The 49.5 mark is barely below [...]

The EU Commission index for the European Monetary Union countries has fallen to 101.7 in September from 103.1 in August. At this mark, the index has a 49.5 percentile standing on data back to late-1988. The 49.5 mark is barely below 50, the level that represents the median for the series. So the EMU index has fallen from the highest point it had reached since before the 2000 recession and is now just below its median mark. What's next?

The EU Commission index for the European Monetary Union countries has fallen to 101.7 in September from 103.1 in August. At this mark, the index has a 49.5 percentile standing on data back to late-1988. The 49.5 mark is barely below 50, the level that represents the median for the series. So the EMU index has fallen from the highest point it had reached since before the 2000 recession and is now just below its median mark. What's next?

Momentum

Momentum is unfortunately very negative again. Of the 18 early reporters, 12 (13 counting the United Kingdom) have declining readings in September. This follows August when only five registered slippage (plus the U.K.); this followed July when 9 (plus the U.K.) had fallen month-to-month. September does mark a step up the negative momentum.

Over a longer horizon, only Slovakia shows a 12-month rise. However, over six months, Lithuanian, Slovakia, Cyprus, Greece, and France show gains. Over three months, Portugal, Austria, Cyprus, Slovenia, Slovakia, Latvia, and Lithuania show gains (for a total of seven). There is some unevenness to the weakness mostly in the more volatile small countries that have showed some gains recently as downward momentum is still intense.

Standing

The overall EMU index has a 49.5 standing which is near its median. Nine countries have standings below their respective medians including three of the four largest EMU economies (France is the exception). One country, Malta stands at its median value. Owing to Brexit, the U.K. at 10.8% (Europe's second largest economy) has the lowest percentile standing in the table. The highest standings are Cyprus 93.5%, Lithuanian 87.1%, and Greece at 73.4%. The inclusion of Greece highlights that this method ranks each country relative to its performance since the late 1980s. Greece has a current comparison against some very poor historic values.

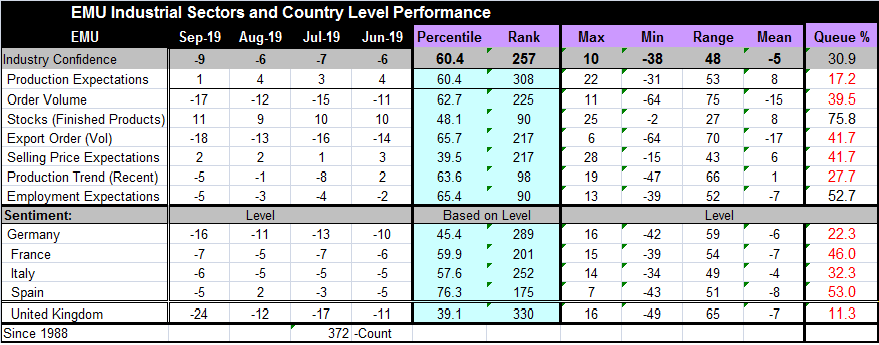

Sector standing: Only one sector has a below median standing, but that is the key industrial sector. The industrial ranking is a very weak 30.9 percentile with services at a 51.5 percentile ranking. Construction has a very strong 94.1 percentile standing, but it is a small sector. Retailing is surprisingly buoyant with an 83.3 percentile standing (it has been stronger less than 17% of the time). Consumer confidence across the EMU area has a 76th percentile standing, a top 25th percentile mark.

There is clear tension between the weakness in manufacturing and the ongoing buoyancy of the consumer. This is true in Europe as well as in the United States. In Europe, however, there is some evidence that the relentless weakness in the manufacturing sector has begun to drag down the services sector. We see this in the eroding service sector PMIs from Markit. In the U.S., the Fed keeps lauding firm-to-strong consumer spending, but just today August U.S. consumer spending (PCE) rose by just 0.1% month-to-month and real spending is rising at just a 2.3% pace over three months compared to a 4.6% pace in the Q2 GDP report. The real question for the U.S. and Europe is whether the consumers can keep it up if the trade war drags on. Right now it appears as though the consumer is falling behind in that race. Meanwhile, the industrial sector continues to weaken further.

The industrial sector reading slipped to -9 in September from -6 in August to a 30.9 percentile standing. The strongest component in the industrial survey is stocks; that is a bad sign since it shows inventories are high while orders, output and output expectations are weak. Employment expectations cling to a 52.7 queue standing, a reading just above its median. Employment is usually a lagging variable. Note the weakness in the sector reading for industry at the bottom of the table. The U.K. is doing very badly.

Summing up

Summing up

The period of weakness and of the downward momentum in the EMU clearly is continuing. While there are still a few sectors of resistance against the weakness, the problem is that, except for construction, the strong sectors seem to be losing their staying power. The erosion of weak manufacturing is spreading the disease of weakness. Central banks have applied their own inoculation, but so far it does not seem sufficient and what they have done has met with some significant criticism and that will cause it to be less effective since we know we are no longer in the land of 'whatever it takes.' We are now in the land of 'You are on your own.' And that will make a difference to how stimulus is perceived, received and in what is achieved.

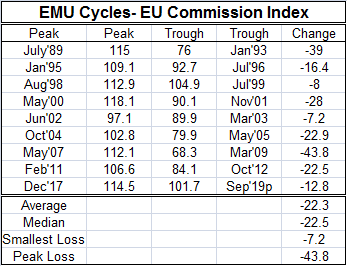

I count nine significant cycles in the EU Commission index for the EMU since the late 1980s. While there is a good deal of consternation about the current cycle so far, it is really one on the milder ones. As of September, there are only two cycles milder than this one since mid-1989. This cycle has not been severe because the manufacturing sector has not dragged the rest of the economy along with it kicking and screaming. But that could yet happen. As such, the table should either reassure you or scare the dickens out of you about what may lie ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates