Global| Jan 30 2015

Global| Jan 30 2015The Germans in the Dell: the Cheese and the Germans Stand Alone

Summary

The unemployment rate turned lower in December in both the EU and EMU. This, despite a host of problems: weak PMI readings and the ECB on a glide path to its controversial QE plan. Of the 11 topically reporting members in the table, [...]

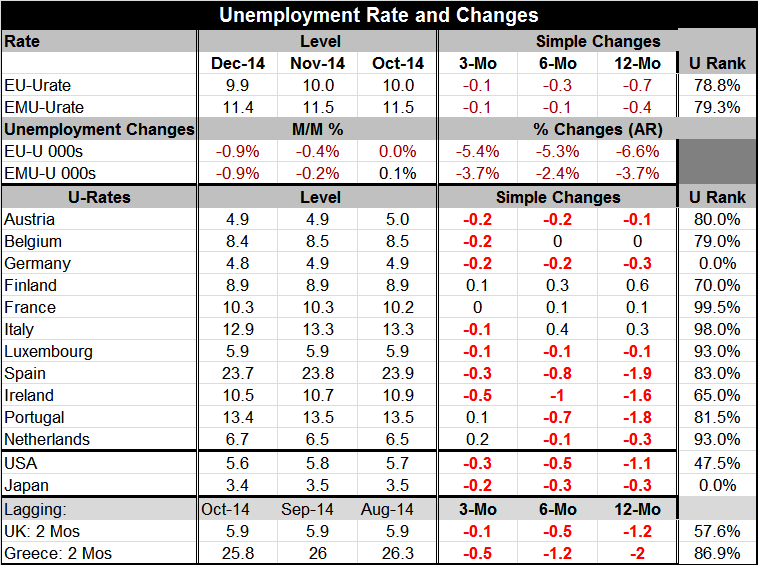

The unemployment rate turned lower in December in both the EU and EMU. This, despite a host of problems: weak PMI readings and the ECB on a glide path to its controversial QE plan.

The unemployment rate turned lower in December in both the EU and EMU. This, despite a host of problems: weak PMI readings and the ECB on a glide path to its controversial QE plan.

Of the 11 topically reporting members in the table, only three saw the unemployment rate rise over the last three months on balance. The unemployment rate fell in seven of these nations. On a lagged basis, unemployment fell in the U.K. and in Greece, too. Year over year the unemployment rate is lower in nine of these 11 counties, including EU member the U.K. and lagging Greece.

On the surface the momentum looks constructive and of course it is. But it may not be quite what it seems. For Spain, Ireland, and Portugal, the unemployment rate has dropped over 12 months in the range of 1.5 percentage points to 2 percentage points, sizeable drops. Despite this progress, we are not speaking of normalcy any time soon. We are only speaking of making progress to a goal that is yet on a very distant horizon. That is except for one country, Germany.

The German unemployment rate has hit its low. From 2009 onward, this is as low as German unemployment has been. Compare that to the rest of the countries in the table where the unemployment rate is swimming in the top 10% (90th percentile) for four of them, the top 20th percentile for three of them; four including Greece. It is in the top 30th percentile for two more and in the top 35th percentile for Ireland, the best of the lot, excluding Germany, of course. Germany stands alone.

By comparison, the U.S. unemployment rate stands in its 47th percentile on this timeframe and Japan, like Germany, is seeing its lowest rate, but largely (like the U.S.) for demographic reasons.

The ECB's new QE program is yet to be launched. Its asset backed purchase program, which has been in place, seems to have borne little fruit. But most of the ECB's hopes are placed on QE. Still, QE is being launched in a hostile environment. Both ECB and German headline inflation rates have dipped below zero. Deflation is alive and stalking the EMU. True, the core inflation rates are still above zero allowing us the prevarication of saying so far it's just energy prices with weak inflation elsewhere. But as we well know, those deflation forces can spread. EMU economic growth is still weak.

Many EMU challenges lie ahead. Not the least of these is the wide gap between Europe's largest economy, Germany, and the rest of the euro area. The rest of the euro area looks like it belongs together, but Germany is like the cheese in the famer in the Dell rhyme. Germany stands alone. And because of that and since ECB policies are made for the euro area as a whole and not for a single member, Germany is going to see ECB policies implemented that are inappropriate for Germany. Germany is going to see a euro too weak, interest rates too low and QE too stimulative. We should be prepared for this in 2015. German forecasts for 2015 growth have been notched up by a tick or two. But Germany is set not just to grow a little bit faster but to progress toward overheating. The only brake for Germany would be to run a contractionary fiscal policy. And we may see that. Of course, that is the opposite of what the rest of Europe would like to see.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates