Global| Mar 07 2008

Global| Mar 07 2008U.S. Payrolls Again Fell Unexpectedly

by:Tom Moeller

|in:Economy in Brief

Summary

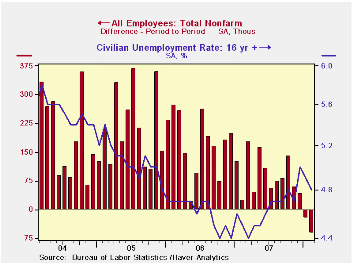

The Bureau of Labor Statistics reported that for the second consecutive month, nonfarm payrolls fell. A 63,000 decline last month followed a downwardly revised 22,000 drop during January. The December job gain also was revised weaker. [...]

The Bureau of Labor Statistics reported that for the second consecutive month, nonfarm payrolls fell. A 63,000 decline last month followed a downwardly revised 22,000 drop during January. The December job gain also was revised weaker. Expectations had been for a modest 25,000 increase in February payrolls.

The decline in payrolls was the first consecutive two-month drop since 2003.

To the upside was job creation in the government sector where February employment rose 38,000 (1.1% y/y). Strength in hiring by state governments (1.2% y/y) and localities (1.3% y/y) has offset weakness in job creation by the Federal government (-0.1% y/y). This strength in government sector job creation only highlights weakness in the February labor report. Private sector employment fell 101,000 (+0.5% y/y), the largest decline of three during the last three months.

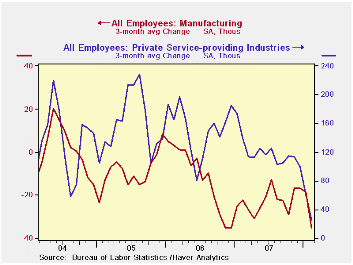

Weakness in factory sector hiring intensified as indicated by a 52,000 drop in payrolls. That was the deepest since 2003 and compared to an average monthly decline of 22,000 last year.

The rate of decline in construction employment also picked up steam. Employment here fell 39,000, twice the average monthly job loss last year.

The news out of the private service sector was perhaps more distressing. A 12,000 loss of jobs was the first since 2003. It dropped the two month change to a meager 8,000 and it compared to an average monthly gain of 109,000 last year. Professional & business services jobs fell by 20,000 (+1.3% y/y) while temporary help services jobs cratered 27,600 (-3.9% y/y). They have been declining for more than a year. Jobs in retail trade also fell a hard 34,100 (-0.0% y/y) and a January increase was revised away. Employment in finance dropped as well by 12,000 and it fell 1.5% from the late 2006 peak. Weakness in the real estate sector continued to lead the softening with a 7,000 job loss last month. Since the 2006 peak jobs are down 2.2%

Jobs in education continued to grow. A firm 30,000 February increase was only slightly off last year's pace of 45,000 per month (3.0% y/y) while job gains in the health care sector rose 37,000 (2.9% y/y), right on last year's pace. Jobs in the leisure & hospitality sector also rose a steady 21,000 (2.5% y/y) last month.

Continuing to portend further weakness in overall job creation was another decline in the one month diffusion index to 45.6%. This measure of the breadth of job creation amongst industries was its lowest level since 2003. The three month index also was a weak 46.9%.

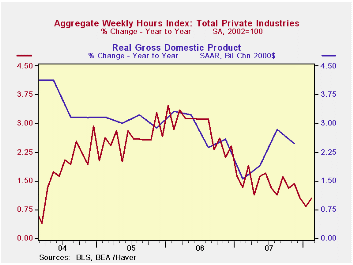

What the employment numbers say about overall economic growth this quarter is not good. When the job figures are combined with what was a stable level of hours worked, the level of aggregate hours (employment times hours) fell both last month and in January. Those declines pulled the average for 1Q so far down 1.3% (AR) from 4Q07. During the last thirty years there has been a 76% correlation between the q/q change in aggregate hours worked and the change in real GDP. That correlation has fallen in recent years, however, as productivity has picked up.

Average hourly earnings rose a very steady 0.3%. Weakness in job creation, however, has lowered the y/y gain to 3.7% which is down slightly from the peak 4.0% rise during all of last year. Factory sector earnings rose 0.1% (3.0% y/y) and private service-providing earnings rose 0.3% (3.8% y/y).

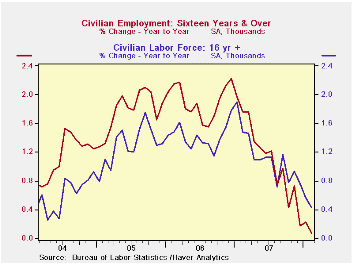

The unemployment rate slipped again, last month to 4.8%. Household employment declined 255,000 (0.1% y/y) and that points up the deterioration in y/y job growth to 0.1% from a 1.1% gain during all of last year and of 1.9% in 2006. A decline in the labor force of 450,000 (+0.4% y/y) is what kept the February unemployment rate from rising.

The average duration of unemployment fell slightly to 16.8 weeks from 17.5 in January and from 16.9 weeks last year.

Exchange Rate Pass-Through and Monetary Policy is today's speech by Federal Reserve Board Governor Frederic S. Mishkin and it is available here.

| Employment: 000s | February | January | December | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | -63 | -22 | 41 | 0.6% | 1.1% | 1.8% | 1.7% |

| Previous | -- | -17 | 82 | -- | 1.3% | 1.9% | 1.7% |

| Manufacturing | -52 | -31 | -22 | -2.1% | -1.9% | -0.5% | -0.6% |

| Construction | -39 | -25 | -55 | -2.9% | -1.0% | 4.9% | 5.2% |

| Average Weekly Hours | 33.7 | 33.7 | 33.8 | 33.7 (Feb. '07) | 33.8 | 33.9 | 33.8 |

| Average Hourly Earnings | 0.3% | 0.3% | 0.3% | 3.7% | 4.0% | 3.9% | 2.7% |

| Unemployment Rate | 4.8% | 4.9% | 5.0% | 4.5% (Feb '07) | 4.6% | 4.6% | 5.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates