Global| Aug 19 2008

Global| Aug 19 2008U.S. PPI Up 1.2%; Big Increases Widespread

Summary

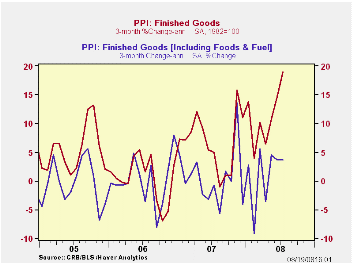

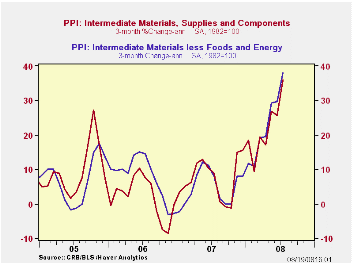

Producer prices continued strongly higher in July, with the total index up 1.2% after June’s outsized 1.8%, and the core up a substantial 0.7%, considerably more than June’s 0.2%. Forecasts for the total index centered around 0.6% and [...]

Producer prices continued strongly higher in July, with the

total index up 1.2% after June’s outsized 1.8%, and the core up a

substantial 0.7%, considerably more than June’s 0.2%. Forecasts for the

total index centered around 0.6% and for the core, 0.2%. Intermediate

goods rose 2.7%, with their core up 2.0% and crude goods were up 4.2%,

with the core up 3.4%. All of these are monthly changes; year-on-year,

finished goods prices are up 9.8% and crude goods a whopping 51.3%.

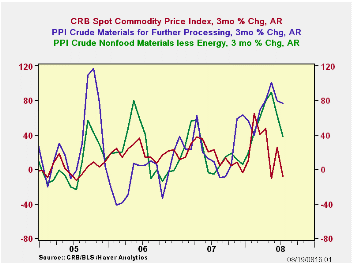

What we know, though, before we panic over these inflationary

figures, is that the PPI data are collected near mid-month,

specifically the Tuesday of the week containing the 13th of the month.

For July, that day would be Tuesday, July 15, now five weeks ago. That

period was near the peak in commodity prices; by yesterday, futures

prices, measured by the Reuters/Jeffries CRB Futures Index had fallen

14.6% since that date, and the CRB Spot Index was down 5.5%. So while

the previous gains in commodity prices continue through the production

and distribution system, we do know that some relief might already be

in process.

Meantime, the bigger-than-expected gain in the July finished goods index did hit a wide variety of items. Food was a notable exception, inching up only 0.3% from June. But energy rose 3.1%, concentrated in residential gas (8.8%) and heating oil (3.7%); before seasonal adjustment, gasoline was up 2.8%, but that was all seasonal (believe it or not!), so that with adjustment, it was actually down 0.2% (sure.) Among consumer goods with better-than-1% monthly increases are soaps & detergents, tires & tubes, newspapers, floor coverings, sporting goods and fine jewelry. Capital equipment overall saw an 0.8% rise, seasonally adjusted. Among the larger advances there are machine tools, materials handling equipment, pumps, transformers, heavy trucks and ships. Passenger car wholesale prices rose 0.5% in July and light trucks 0.8%, both seasonally adjusted. Several of these show the effects of earlier increases in lumber, petroleum and metals and we can hope that renewed declines in those raw materials can help alleviate further price pain.

| Producer Price Index (%) | July | June | Yr/Yr | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Finished Goods | 1.2 | 1.8 | 9.8 | 3.9 | 3.0 | 4.9 |

| Core | 0.7 | 0.2 | 3.6 | 1.9 | 1.5 | 2.4 |

| Intermediate Goods | 2.7 | 2.1 | 16.8 | 4.1 | 6.4 | 8.0 |

| Core | 2.0 | 1.3 | 10.2 | 2.8 | 6.0 | 5.5 |

| Crude Goods | 4.2 | 3.7 | 51.3 | 12.1 | 1.4 | 14.6 |

| Core | 3.4 | -0.2 | 36.9 | 15.6 | 20.8 | 4.9 |

by Carol Stone August 19, 2008

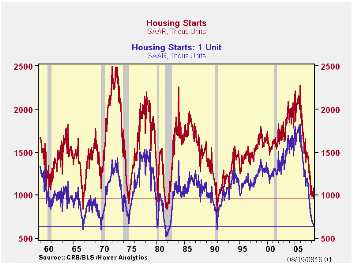

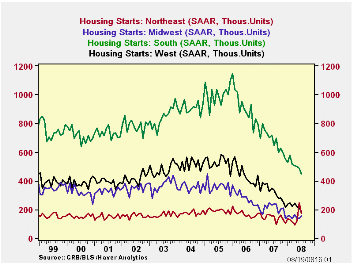

After June’s phantom jump in housing starts, which owed completely to a building code change in New York, they fell back in July by 11.0% to just 965,000 (S.A.A.R.). This was the lowest since 921,000 in March 1991. This month, both single-family and multi-family starts declined, by 2.9% and 23.6%, respectively. There were marginal upward revisions to June and May totals. As evident in the first graph, the total and the single-family amounts are not only the lowest since the last major housing contraction in 1991, but they are at levels that have only been since during periods of major housing distress.

At the same time, multi-family starts have been somewhat

steadier. They retreated

surely in July from their artificial surge in June, but their general

pace has held up; in July, they numbered 324,000, just below their

average over the last 10 years of 339,000. With

the great weakness in single-family units, multi-family building now

constitutes more than a third of new home construction.

By region in July, the Northeast reversed its June increase, but it remains the steadiest part of the country on trend, and actually stands 13.0% above a year ago. The July loss was all in multi-family, while single-family units there were up smartly, by 11.3%. Total starts were also down in the South and the West, both, coincidentally, by 8.2%. Starts rose in the Midwest in July, by 10.0%.

Building permits followed the same pattern as starts nationally in July, falling 17.7% after a June increase of 16.4%. Single-family permits dropped 5.2% in the month to 584,000, the weakest since September 1982.

| Housing Starts (000s, SAAR) | July | June | May | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Total | 965 | 1,084 | 982 | -29.6% | 1,341 | 1,812 | 2,073 |

| Single-Family | 641 | 660 | 682 | -39.2% | 1,034 | 1,474 | 1,719 |

| Multi-Family | 324 | 424 | 300 | +2.5% | 307 | 338 | 354 |

| Building Permits | 937 | 1,138 | 978 | -32.4% | 1,389 | 1,844 | 2,160 |

by Louise Curley August 19, 2008

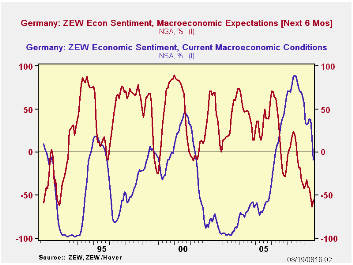

The ZEW indicator of German economic sentiment among

institutional investors and analysts improved in August. It remained,

however at historically low levels. The percent balance between the

pessimists and the optimists rose from -63.9% in July to -55.5% in

August. At the same time, the appraisal of current conditions by the

financial community worsened and showed an excess of pessimists of

9.2%, the first negative since March 2006. The first chart shows the

percent balances for expectations and current conditions.

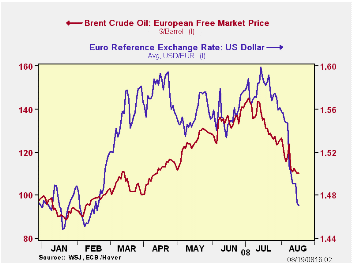

The recent declines in the euro and the price of oil may well have accounted for the improvement in sentiment concerning the outlook for the next six months. Lower oil prices should improve the profit outlook for business and the lower Euro should benefit exports. The second chart shows the daily price of oil and the value of Euro in dollar terms in the current year. The price of oil is down 23% from its high on July 11, and the Euro is down 8% since its high on July 15.

After Eurostat reported that Germany's second quarter GDP declined by 0.5%, it is not surprising that the pessimists have begun to exceed the optimists in their appraisal of current conditions.

| GERMANY | Aug 08 | Jul 08 | Jun 08 | May 08 | Apr 08 | Mar 08 | Feb 08 | Jan 08 |

|---|---|---|---|---|---|---|---|---|

| ZEW Indicator of Expectations (% bal) | -55.5 | -63.9 | -52.4 | -41.4 | -40.7 | -32.0 | -39.5 | -41.6 |

| ZEW Indicator of Current Situation (% bal) | -9.2 | 17.0 | 37.6 | 38.6 | 33.2 | 32.1 | 33.7 | 56.6 |

| High | Date | Recent | Date | % chg | ||||

| Oil Price (bbl) | 143.25 | 7/11 | 110.08 | 8/15 | -23.16 | -- | -- | -- |

| US/Euro | 1.599 | 7/15 | 1.470 | 8/18 | -8.04 | -- | -- | -- |

by By Robert Brusca August 19, 2008

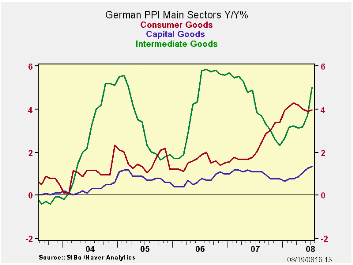

Although German officials are trying to calm the public about

growth prospects the inflation numbers that being churned out are far

from reassuring in inflation-wary Germany. Core PPI inflation is on a

tear up to a 6.1% pace over three-months and 3.6% Yr/Yr. In Q3-to-date

inflation for the Core PPI is running at a 7.1% pace with headline PPI

inflation at a 19.4% pace. And Germany is one of those EMU places that

tends to keep inflation more under control.

Growth has been sputtering. Accelerating inflation will simply

tie the hands of the ECB for a longer period of time. Everyone believes

that falling oil prices make headline inflation less of a threat. But

the rising core remains an issue that all central banks will be wary

of. Prospects for unwinding elevated core inflation under lower energy

prices are good, too. But any core unwind will take time.

| Germany PPI | ||||||||

|---|---|---|---|---|---|---|---|---|

| %m/m | %-SAAR | |||||||

| Jul-08 | Jun-08 | May-08 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | IN Q3 | |

| MFG | 2.0% | 1.0% | 1.1% | 17.4% | 12.7% | 8.9% | 1.1% | 19.4% |

| Ex Energy | 0.8% | 0.4% | 0.4% | 6.1% | 5.1% | 3.6% | 2.5% | 7.1% |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates