Global| Dec 04 2007

Global| Dec 04 2007Uh, oh and Away …PPI Sails Well Above 2% Pace

Summary

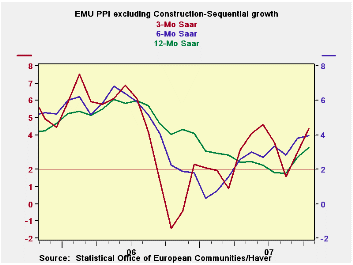

The EMU ex construction PPI chart shows a clear pattern of acceleration. The PPI (excluding construction) has a 3-month rate in excess of its six-month pace that is, in turn, above the Yr/Yr pace. That is acceleration by definition. [...]

The EMU ex construction PPI chart shows a clear pattern of

acceleration. The PPI (excluding construction) has a 3-month rate in

excess of its six-month pace that is, in turn, above the Yr/Yr pace.

That is acceleration by definition. All measures are well above the

hypothetical ceiling rate of inflation of 2% (that ceiling applies to

the HICP alone, however). Still, having PPI inflation at this strong of

a pace must be disconcerting to the ECB.

More disconcerting is for ex-energy inflation to show that

same sort of accelerating pattern: 3-month inflation, at 3.4%, exceeds

6-month inflation, at 3%, and that pace is only a tick below the

12-month pace at 3.1%. All of these speeds are above the 2% mark and

therefore excessive.

These sorts of ‘cost pressures’ in turn feed into the CPI in a

way that is unhealthy. It is hard for the CPI (HICP) to maintain a sub

2% pace if the things that go into it, or that underlie it, are

speeding ahead faster. Consumer goods inflation is a major culprit with

inflation on a steady sequential acceleration and a three-month pace of

6.4%. Of course energy and all its pressures are embodied in that

measure. Intermediate goods inflation has been quieting down with the

opposite tendency, revealing deceleration with inflation below 2% over

the recent three months at 1.7%. Capital goods inflation is at 1.1% and

also has been decelerating, but not uniformly.

Among the larger EU countries, Germany shows overall and

Ee-energy PPI inflation that is excessive and accelerating. Italy shows

an excessive and accelerating PPI and an ex-energy inflation that is

over the 2% mark but not worsening. The UK shows a greatly accelerating

headline PPI while ex-energy producer price pressures are clear but a

bit less strident.

On balance, the ECB has a PPI report that will give it little

sense of relief. The EMU PPI components make inflation appear a bit

more like it is a consumer sector problem in the main. That is curious

since that has been such a weak sector in EMU while the capital goods

sector has been vibrant and yet there inflation remains tame and is

ensconced well within its preferred range. All this leave the ECB in a

quandary that only worsens when you look at the foreign exchange market

and consider, too, the loss of momentum growth has been seeing in the

region.

| Euro area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Ezone-13 | Oct-07 | Sep-07 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Total excl Construction | 0.6% | 0.4% | 4.5% | 3.7% | 3.3% | 4.0% |

| Excl Energy | 0.4% | 0.2% | 3.4% | 3.0% | 3.1% | 3.6% |

| Capital Goods | 0.1% | 0.1% | 1.1% | 0.9% | 1.5% | 1.7% |

| Consumer Goods | 0.6% | 0.5% | 6.4% | 4.8% | 3.4% | 1.7% |

| Intermediate & Capital Goods | 0.2% | 0.1% | 1.7% | 2.0% | 3.0% | 4.5% |

| Energy | 1.7% | 1.0% | 9.1% | 6.7% | 4.0% | 5.2% |

| MFG | 0.5% | 0.4% | 4.0% | 4.0% | 3.9% | 2.5% |

| Germany | 0.4% | 0.2% | 2.7% | 2.2% | 1.7% | 4.6% |

| Germany ex Energy | 0.4% | 0.0% | 2.9% | 2.4% | 2.4% | 3.0% |

| Itlay | 0.4% | 0.5% | 4.7% | 4.0% | 3.6% | 4.9% |

| Italy ex Energy | 0.2% | 0.2% | 2.4% | 2.4% | 3.1% | 4.4% |

| UK | 2.2% | 1.2% | 14.3% | 9.7% | 3.9% | 5.4% |

| UK ex Energy | 0.4% | 0.2% | 3.2% | 2.9% | 3.2% | 3.3% |

| E-zone 13 Harmonized PPI excluding Construction | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, | ||||||

| Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief