Global| Nov 23 2007

Global| Nov 23 2007UK Banks Sharply Restrain MortgageLending in October

Summary

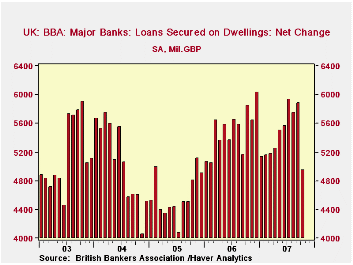

The British Bankers' Association (BBA) this morning reported significant declines in mortgage lending activity for October. These data cover the nine members of the "Major British Banking Groups", which account for some two-thirds of [...]

The British Bankers' Association (BBA) this morning reported significant declines in mortgage lending activity for October. These data cover the nine members of the "Major British Banking Groups", which account for some two-thirds of all UK mortgage loans outstanding.

The net change in loans outstanding at these big banks was £4.95 billion in October, markedly less than September's £5.88 billion and the smallest monthly amount since December 2005, £4.90 billion. The peak month was December 2006 at £6.04 billion.

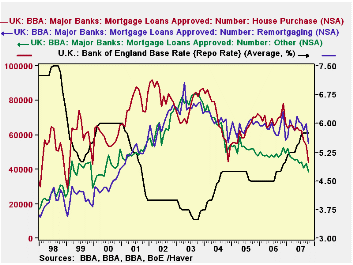

The accompanying loan approval information is valuable, of

course, as a leading indicator of the actual loans made. This showed

distinct weakness in October, with the number of loans approved for

home purchase at just 44,100 (absolute figure, not rounded or

annualized), compared with almost 54,000 in September. The year-ago

number was 70,458 and the recent peak was 78,301 in November 2006. Loan

approvals for remortgaging and for "other" purposes -- this last

importantly including equity withdrawal -- also decreased

significantly. As seen in the second graph here, the last "other"

category has been drifting downward since a peak in late 2003. But

straight refinancing loans have more or less paralleled home purchase

loans since early 2003. Both of these loan groups retrenched somewhat

with the Bank of England tightening during 2004, but held up well

during more interest rate hikes from mid-2006. Finally, both purchase

and remortgaging loan approvals began to come down more decisively in

May this year and have continued to decrease since then despite the

BoE's steady rate policy beginning in August.

These lending data for October reflect the first full month following the international credit crunch of late August and September. In the UK, this directly involved Northern Rock, one of the nine "Major British Bank Groups" and a "Top 5" mortgage lender, which experienced massive deposit runs in September. The October figures thus illustrate clearly the impact of reversals in the global mortgage security market. Additionally, press reports today also indicate that Northern Rock's own delinquency experience has been worsening. Broader data on mortgage possession actions from the UK's Council of Mortgage Lenders show a sharp uptrend in such proceedings beginning in 2006. So while we may be disturbed by loan performance in the US, it is certainly not the only country where borrowers are faltering, contributing to an eventual slowdown in the entire home financing system.

| UK BBA | Oct 2007 | Sept 2007 | Aug 2007 | Year Ago | Monthly Averages | ||

|---|---|---|---|---|---|---|---|

| 2006 | 2005 | 2004 | |||||

| Mortgage Loans, Net Change, Bil.£ | 4.95 | 5.88 | 5.75 | 5.84 | 5.50 | 4.59 | 5.05 |

| Number of Loan Approvals | |||||||

| Home Purchase | 44,100 | 53,997 | 56,811 | 70,458 | 68,961 | 62,754 | 68,888 |

| Remortgaging | 54,881 | 66,519 | 62,559 | 66,238 | 64,149 | 65,014 | 67,989 |

| Other (incl "Equity Withdrawal") | 38,471 | 43,143 | 40,744 | 48,298 | 48,557 | 52,127 | 64,924 |

| Average Value, Loans Approved for Home Purchase*, £ | 153,500 | 152,300 | 153,800 | 144,600 | 139,167 | 128,250 | 112,100 |

by Robert Brusca November 23, 2007

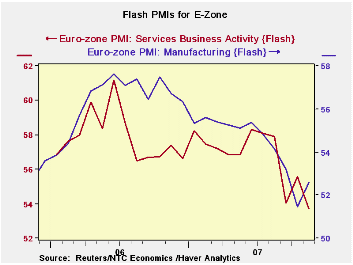

The NTC-Reuter Flash PMIs for November show an unexpected

bounce for Manufacturing and slip for Services. Both readings are weak,

however. Placed in the past 23-month range (the whole of the life of

the services index) services are the weakest ever at a reading of

53.72. The MFG index is in the 18.5 percentile of its range for this

period. Although taking MFG back to 1997, we find it resides in the

55th percentile of its much longer range experience. That experience

includes episodes of recession whereas for services and MFG the shorter

comparison does not.

The graph, however, underscores that the peaking and dropping

of the indices dates from super-peaking in 2006 then to a dropping from

a lower plateau in mid 2007. Currently the indices are chopping around

at a much lower level that barely indicates continuing growth (above a

level of 50).

We know that the strong euro is part of the problem, but

interestingly the outlook and slowing has spread though the services

industries just as fast even though MFG is sure to be affected first by

foreign exchange issues. With exports plus imports accounting for 40%

of GDP in some EMU nations it is no wonder that the impact of a strong

currency spreads faster that in the US where the sum is so much smaller.

In Germany the export association says firms can still export

at an exchanger rate to the dollar of 1.50 but Merkel is registering

worry already and orders of all sorts across the Euro Area members are

slowing if not weakening. The NTC indices memorialize and underscore

that Europe is slowing and is well off peak. They tell us more

topically what other indices will hold for us in the months ahead.

While certain groups of exports may be more resilient than others some

line seems to have been crossed that says that a the euro has risen

above a critical level that is taking business prospects down a notch

for some critical mass of companies. In part this means that US-based

firms should benefit form the exact factor that is hurting European

business (FX competitiveness), but due to the weakness in Europe that

the euro strength also engenders, that the amount of benefit will be

limited.

| FLASH Readings | ||

|---|---|---|

| NTC PMIs for the Euro Area 13 | ||

| Manufacturing | Services | |

| Nov-07 | 52.60 | 53.72 |

| Oct-07 | 51.46 | 55.56 |

| Sep-07 | 53.21 | 54.04 |

| Aug-07 | 54.16 | 57.91 |

| Averages | ||

| 3-Mo | 52.42 | 54.44 |

| 6-Mo | 53.61 | 56.28 |

| 12-Mo | 54.56 | 56.74 |

| 23-Mo Range | ||

| High | 57.61 | 61.21 |

| Low | 51.46 | 53.72 |

| % Range | 18.5% | 0.0% |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief

Global| Mar 19 2026

Global| Mar 19 2026Charts of the Week: Energy Shock — Early Signals, Uncertain Fallout

by:Andrew Cates