Global| Feb 07 2008

Global| Feb 07 2008UK Industrial Production Growth Slows to a Crawl

Summary

UK industrial production slowed sharply in December and major trends are all pointing lower. IP in December was weaker than had been assumed in the UK GDP report, raising the possibility that GDP could be revised lower. The quarterly [...]

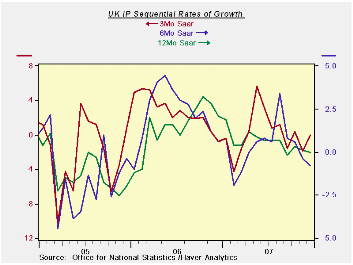

UK industrial production slowed sharply in December and major

trends are all pointing lower. IP in December was weaker than had been

assumed in the UK GDP report, raising the possibility that GDP could be

revised lower. The quarterly growth rate for manufacturing is -0.4% in

Q4. The sequential growth rates from 12 months to 6 months to 3 months

show a slowing across manufacturing components with the exception of

capital goods. Detailed sectors show food and drink, textile and

leather and motor vehicle sectors in a progressive state of decline and

deceleration. The quarter’s growth rate for these components is deeply

negative and so would the overall result if it were not for strength in

the utilities output and some growth in mining and quarrying.

| UK IP and MFG | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Dec 07 |

Nov 07 |

Dec 07 |

Nov 07 |

Dec 07 |

Nov 07 |

|||

| UK Manufacturing | Dec 07 |

Nov 07 |

Oct 07 |

3mo | 3mo | 6mo | 6mo | 12mo | 12mo | Q-4 Date |

| Manufacturing | -0.2% | -0.1% | 0.3% | 0.0% | -1.9% | -0.8% | -0.4% | 0.0% | 0.1% | -0.5% |

| Consumer Goods | ||||||||||

| Consumer Durables | 1.5% | -1.4% | -1.0% | -3.8% | -16.1% | -3.0% | 0.6% | -3.0% | -4.1% | -10.1% |

| Consumer Nondurables | -0.4% | -0.1% | 0.1% | -1.6% | -1.2% | -0.2% | -0.8% | -1.6% | -0.4% | -0.7% |

| Intermediate Goods | -0.4% | -0.1% | 0.7% | 0.8% | 0.0% | -1.3% | -0.8% | 1.5% | 0.8% | 0.0% |

| Capital Goods | 0.6% | 0.1% | 0.7% | 6.0% | 1.5% | 1.3% | 0.7% | 2.3% | 0.7% | 3.6% |

| Memo: Detail | 1Mo% | 1Mo% | 1-Mo% | 3mo | 3mo | 6mo | 6mo | 12mo | 12mo | Q-4 Date |

| Food Drink & Tobacco | -0.3% | 0.0% | -0.5% | -3.1% | -2.3% | -0.8% | -0.4% | -1.6% | -0.5% | -2.5% |

| Textile & Leather | -1.2% | -0.9% | -0.1% | -8.5% | -10.4% | -8.0% | -2.5% | -3.1% | -0.8% | -9.2% |

| Motor Vehicles & Trailer | 0.8% | 0.3% | -2.7% | -6.4% | -14.9% | 3.8% | 9.5% | 9.4% | 7.0% | -8.1% |

| Mining and Quarry | 0.3% | -1.6% | 2.7% | 5.5% | 1.6% | -2.3% | -5.1% | 4.0% | 0.0% | 1.1% |

| Electricity, Gas & Water | 0.6% | 1.1% | 0.2% | 7.9% | 10.2% | 5.8% | 3.3% | 3.7% | 2.9% | 7.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates