European Manufacturing Trends Remain Mixed

Output in the European Monetary Union shows the median rise across early reporting members of 1.3% in November. This is a rebound from a 1.2% decline among the same members in October and compares with a 0.5% increase in September.

Progressive growth trends The medians for their manufacturing growth rates are mixed with year-over-year IP output rising by 0.4%, the six-month median shows a gain of 1.8%, while the three-month median shows a fall of 1.2%, annualized. The progression does not point to any clear trend, although the disturbing element is the decline over the recent three months with five European Monetary Union (EMU) members showing industrial production declines over three months at annual rates ranging from minus 1.2% to minus 11.4%. Over six months only three EMU members show manufacturing output declines, the same as over 12 months.

Quarter-to-date developments Quarter-to-date tracking of industrial production trends in manufacturing are up to date through November; that's two out of three months of the fourth quarter. The median annualized change for the quarter at this juncture is a decline at a 1.5% annual rate. Greece, the Netherlands, and Finland show the largest quarter-to-date declines in progress while the strongest gains come from Belgium, Ireland, and Austria. There is quite a division in growth rates among these early reporting members for fourth-quarter growth, ranging from +20% to -13%.

Recovery since Covid There are still three European Monetary Union members, Germany, France, and Portugal that have not returned to the level of manufacturing output they had enjoyed as of January 2020 before Covid struck. The median among early reporting members shows the gain from January 2020 is 8.3%. The strongest gains from January 2020 comes from Ireland, Belgium, and Austria. These contrast with the countries that have not yet reestablished January levels for output.

Nordic growth Sweden and Norway, countries that are not European Monetary Union members, also have reported manufacturing production data early. Both show output declines in November but both show increases in the recent three months. Sweden shows a 0.4% gain over 12 months, a 1.4% annual rate decline over six months and a strong 5.3% pace over three months. Norway shows positive growth rates on each timeline with growth of 0.3% over 12 months, rising to 2.6% at an annual rate over six months, and ticking down to a 2% pace over three months.

Europe a mixed picture On balance, Europe does not show us strong trends for manufacturing industrial production. There is a solid gain in November but that follows an equally weak performance in October. However, among the nine early reporting countries, four of them Austria, Belgium, Germany, and Ireland show gains in output on all horizons over 12 months, six months and three months. Among those four, Belgium and Germany show trends that are steadily accelerating. On the negative side, only Finland and Greece show declines in output on all three horizons although both of those countries also show steady deceleration is in progress in each of them.

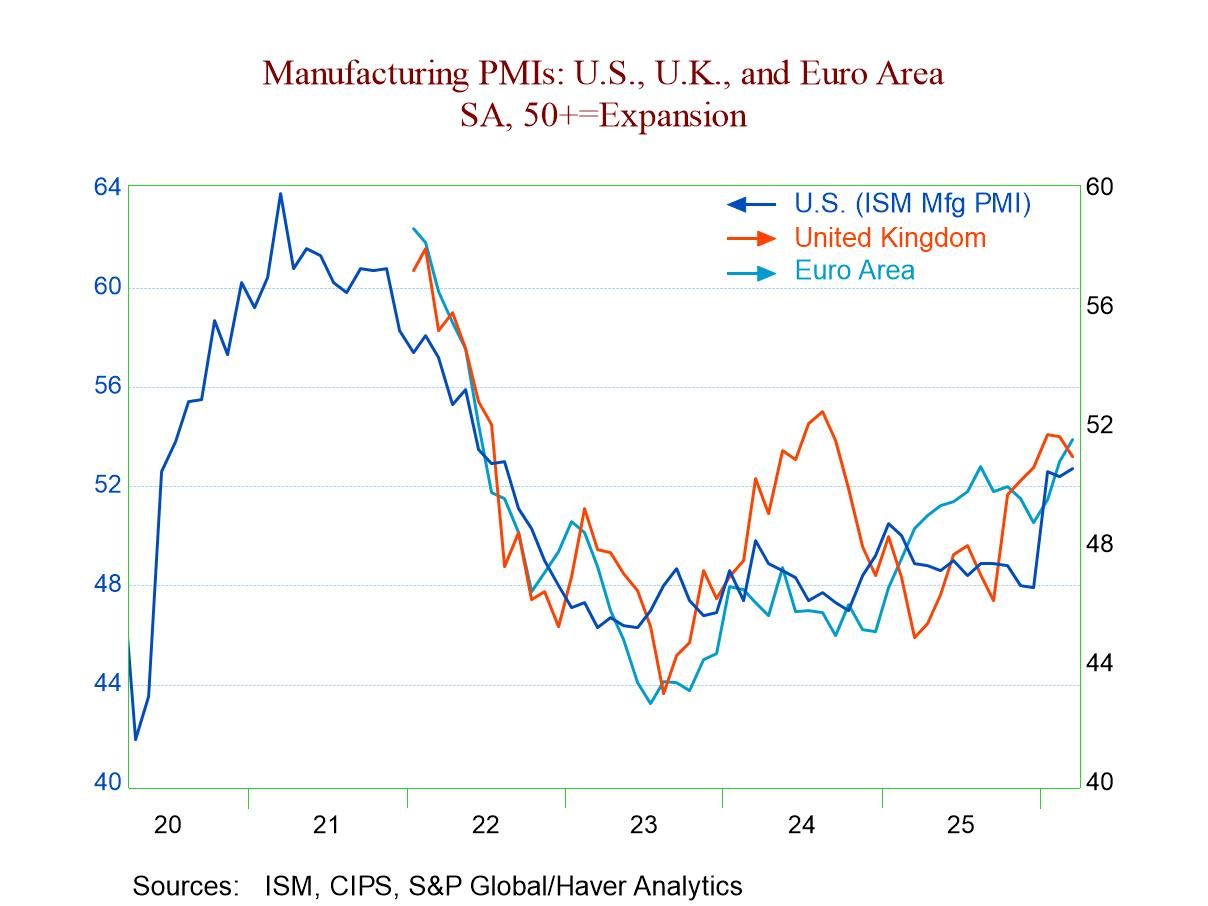

Still in the grip of cross-currents Europe is still in the grip of various cross currents as they are still in the aftermath of the adjustment to Brexit, still adjusting to life in the wake of Covid with the Covid virus still circulating, it has a full scale war going on just outside of its border between Russia and Ukraine, and the European Central Bank is in the midst of trying to get a grip on the inflation that emerged in the post Covid period. This is a lot to deal with at once and it's not surprising that European economies are having some struggle with it. The PMI data across Europe shows that there is a broad slowing of progress that really cuts across manufacturing and services industries. With inflation still excessive, and the European Central Bank raising rates, the prognosis for growth in 2023 is guarded.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global