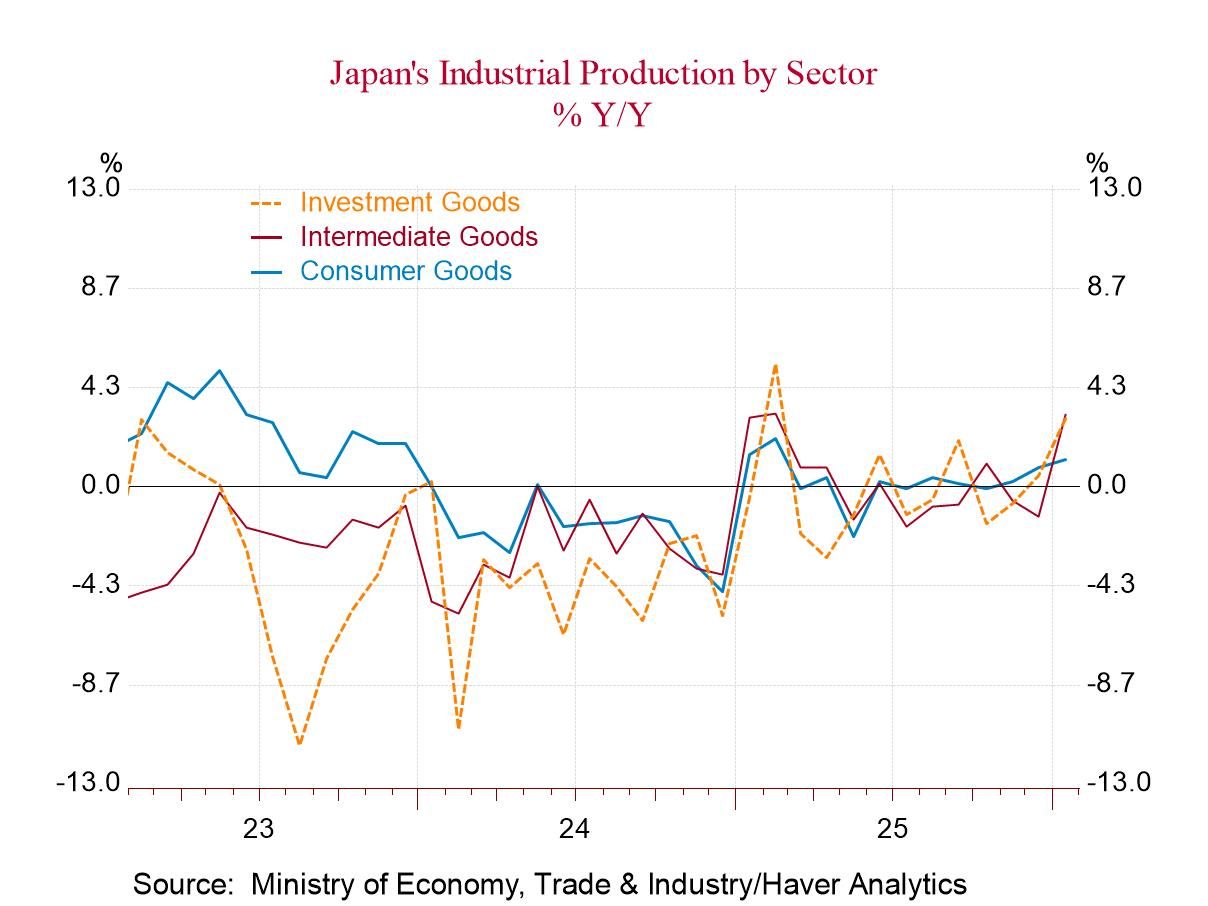

French IP Ignites for a Month

French industrial output rose sharply in August, a gain of 1.6% after declining by 0.2% in July. Output in August was led by consumer goods; nondurable goods output increased 4.2% month-to-month in August while consumer durable goods output increased by 3% month-to-month. Output of capital goods was also strong during the month, with a 1.6% gain, although intermediate goods output continued to be weak, falling by 0.4% in August and dropping for the second month in a row.

Sequentially French output explodes over three months although it's relatively mild mannered over 12 months and over six months. The strength in French output is relatively recent. Manufacturing output gains 0.3% over 12 months; over six months it is falling at a 0.5% annual rate but that transforms into a 31.1% annual rate over three months as output sharply recovered in June and in August.

Sequential growth for MFG components Components find consumer durable goods output falling by 6.3% over 12 months, gaining at a 4% annual rate over six months then rising at a strong 14.9% annual rate over three months showing steady acceleration. Consumer nondurable goods output rises by 5.9% over 12 months; output slows to gain at a 4.3% annual rate over six months then it expands sharply to grow at a 19% annual rate over three months. French capital goods output is up only 0.3% over 12 months, but it then expands at a 1.5% annual rate over six months and gains at a 14.2% annual rate over three months showing steadily accelerating growth on this time sequence. Intermediate goods output falls by 3.4% over 12 months, falls more sharply, at a 6.6% annual rate over six months, then cuts that weakness to only a 0.2% annual rate drop over three months.

Quarter-to-date With two months into the third quarter, manufacturing output is rising at 1.6% annual rate, with consumer nondurable output up at a 7% annual rate and consumer durable goods output up at a 3.8% annual rate. Capital goods output is up at a 4.3% annual rate; intermediate goods output is falling at a 5% annual rate in the quarter-to-date.

During this period when output has been experiencing some mild increases, they have transformed into strong increases over three months. Yet, motor vehicle registrations have been consistently weak. That important big ticket consumer item has not taken off.

Manufacturing: IP vs. PMI The chart shows that manufacturing output as measured by the IP index has been relatively flat. But output as signaled by the S&P PMI survey has showed building weakness in French manufacturing. The PMI trend to weakness was being arrested early in 2024 but then the incipient rebound turned into more weakness. Just this month there has been some small rebound and stabilization in the MFG PMI.

It's here from the PMI, that data give much more of a sense of French output being weak than we get from looking at the industrial output report itself. French industrial output has been fairly flat, but with a small uptrend in place.

Smoothed year-on-year gains show that French output generally saw year-on-year expansion from early-2022 to May 2024. Since then, output has been more erratic with a deep decline logged in May IP. The sector has subsequently been digging itself back out. This month’s surge in output is continuing evidence of that recovery in progress. We do not get the same sense of weakness from looking at French IP data that we form looking at French PMI data.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Mar 19 2026

Global| Mar 19 2026Charts of the Week: Energy Shock — Early Signals, Uncertain Fallout

by:Andrew Cates