French Manufacturing Falls in July -What's Next Is Unclear

Manufacturing industrial production in France fell by 1.6% in July after advancing 0.9% in June and by 1% in May. Production is up by 0.2% over 12 months; however, it falls at a 3.1% annual rate over six months and then rebounds to rise at a 3.9% annual rate over three months. The French trend for production is not yet clear or established.

Sector performance in French manufacturing also shows mixed trends. Consumer durables output was up by 0.6% in July after falling in June; however, the June decline came after a strong surge in May. Consumer nondurables output fell by 1.5% in July after rising by 1% in June and falling by 0.3% in May. French capital goods output fell by 1.4% in July after rising by 1.2% in June and rising by 1.5% in May. Intermediate goods output fell by 2% in July after rising by 0.8% in June and rising by 1.0% in May.

The sequential trends for sector data also vary widely. Consumer durables output in France is accelerating strongly from a 5.3% annual rate over 12 months to an 8.9% annual rate over six months to a 30.1% annual rate over three months. Consumer nondurables, however, are losing momentum; that sector's output rises by 1.1% over 12 months, but falls at a 3.5% annual rate over six months and continues to fall at a lesser, 3% pace, over three months. Capital goods has output up by 0.5% over 12 months; it declines at a 0.7% annual rate over six months then rebounds to post a strong 4.9% annual rate of growth over three months. Intermediate goods output falls by 1.9% over 12 months and falls more substantially at a 6.8% annual rate over six months. That pace of the decline for intermediate goods output is sharply trimmed to -0.8% over three months but it's still a decline.

On balance, sector trends in manufacturing show great strength in consumer durables, with lingering weakness in consumer nondurables, moderation in capital goods that is topped up by strong three-month performance despite a decline in July. Intermediate goods show a steady diet of declines in output.

Where French IP is headed... The headline and sector trends don't give us much confidence about what French industrial production is really set to do. However, the chart also plots the manufacturing index against the French manufacturing PMI index. The PMI index, which is a diffusion treatment derived from a survey of firms, shows that the breadth of output decreases. French industry output has been lowing and in July is finally falling: there are more French businesses reporting output declines than reporting output increases. The diffusion index for July has slipped below 50 that is the indication that the sector is in a state of decline; that assessment accords with the decline in industrial production in July. However, the PMI index has been showing weakening trends for sometime whereas the manufacturing index for industrial production has showed expansion in the last two months with contraction coming only in July. Moreover, the expansion in May in June was significant at about 1% in each of those months. The IP report and the PMI reports are showing different trends

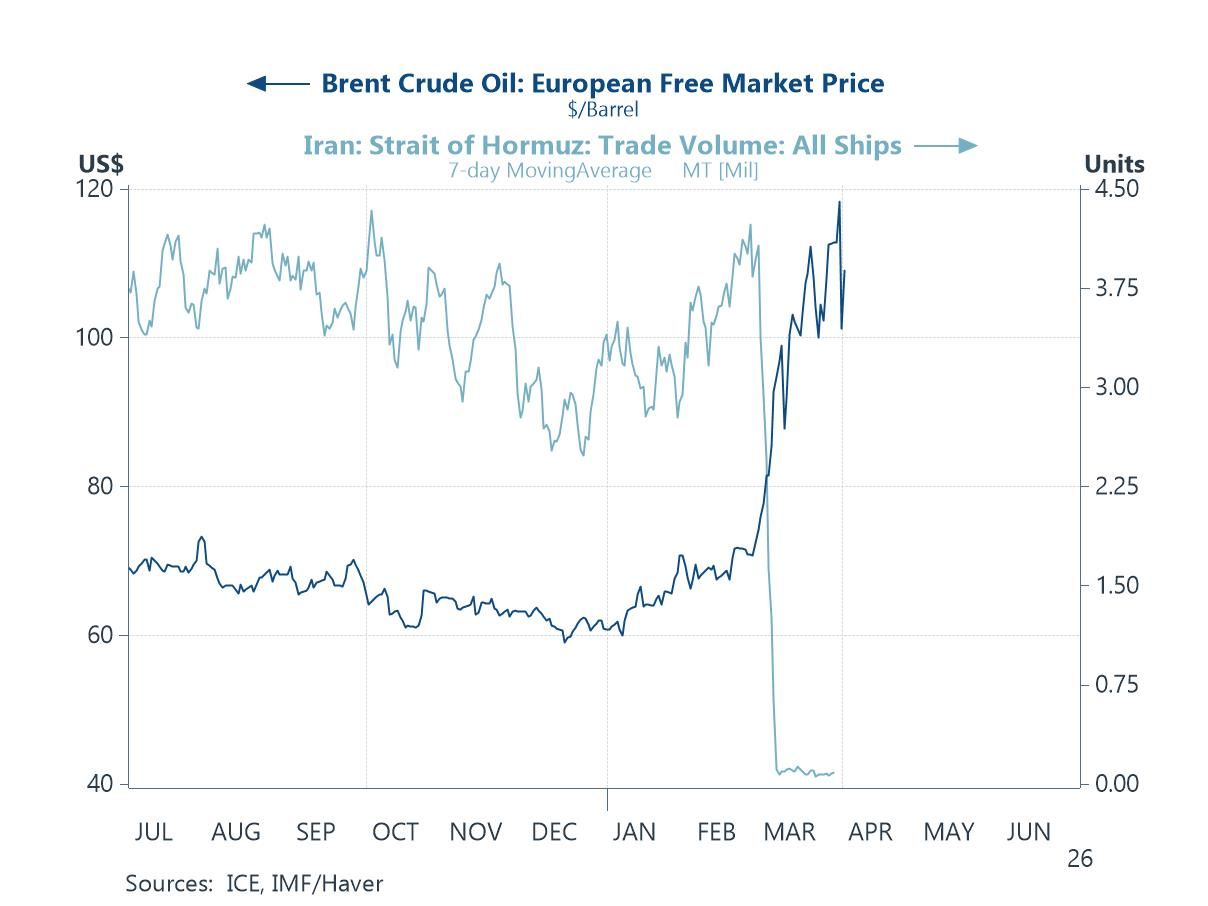

Growth and Europe's energy challenge Trends in French manufacturing are far from clear. However, trends don't always tell the whole story and right now there is a new challenge in Europe and it's about energy. The recent pipeline shut off by Russia has created a sudden energy problem in Europe. European states are meeting to try to decide what to do and one of the things they are talking about is putting price caps on energy because scarcity is driving prices up far too high. Europe has also talked about getting member states to make certain quantitative reductions in their energy usage particularly around peak times. Some of this discussion is about how to cap energy prices and what to do with the excess monies that they will no longer allow energy producers to keep. There's talk about diverting funds to consumers and having differential caps depending on whether an energy producer is making renewable energy or carbon-based energy. These are proposals that are digging deep into market interference and doing the utmost to destroy market pricing of energy in Europe.

Energy policy comes home to roost While Europe has a problem that is going to be extremely hard to solve, it would be easier to solve it if Europe were more interested in solving it without demonizing carbon or trying to anoint renewable energy as saintly. Higher prices may carry with them some unfairness, but they are the way the market gets people and businesses to conserve energy use, which is an important principle in Europe right now. High prices to producers are a way to channel funds to an industry so it can expand and improve supply. That's market economics. However, Europeans do not want carbon-based fuels to increase supplies and they do want renewables to increase supplies. So robbing from carbon to pay renewables make sense to them. I suppose that also makes sense because the entire energy crisis has been caused by bad government policy. Government can argue that since it has created the shortages through bad policy (eliminating nuclear -but not in France- discouraging carbon and making no plans for a workaround should Russian oil stop flowing) it should have control over the excess profits that are being made due to its policy mistakes. However, one problem with this is that renewables aren't a real solution to the energy problem because there is not enough renewable energy to service ordinary demand let alone peak demand. And because renewable energy isn't always available, it's only available when the sun shines, when the wind blows, or when the water flows. And all of those conditions are being challenged in Europe right now. In fact, the European drought has become so bad that in some places the rivers are too shallow and the water too warm to properly cool French nuclear facilities that have been forced to run on reduced output for that reason.

Euro-fornia Europe is somewhat like California, having a bad energy problem that has substantial homegrown elements to it. However, politicians insist on trying to blame it on external events or on global warming. It's too bad that global warming can't make the seats the politicians sit on just a little bit hotter. Climate on the planet is changing. Scientists do not fully understand what's happening, but clearly if man has a role it would be a good time to stop making things worse. However, if carbon is the problem, models have shown that that the potential for the most drastic policy shifts away from carbon to have an impact on climate near term is small. That will not solve these pressing short-term problems. Science needs to work to understand better what's happening with climate change. However, another extremely pressing part of this problem is to do something now and to do something to deal with extant issues. The situations in California and in Europe both should be treated as experiments that we need to learn from even as the people who live in those places need to find solutions that they can live with. The cut off in Russian carbon through its pipeline has come sooner and been more complete than anyone expected. Europe is being caught flat footed by this having mothballed nuclear plants and not built any ports to allow importation of LNG to bridge the Russia cut off. Europe is seeking solutions that are not going to put market economics on their side. Politicians, their objectives and planning, have a very poor record of dealing with climate challenges. Green lovers even welcomed China into the Paris Accord club as it made climate promises it has since broken as it has turned to sharply higher use of coal to support its economy. President Joe Biden has resisted drilling and fracking in the U.S. while encouraging Venezuela, Iran, and OPEC to produce more oil – really! Is that a move that is Green or political? How any of this makes any sense is beyond me. It's not surprising that Europe and California have an intractable energy problem. Nor, I suppose, is it surprising that Europe has chosen to scramble to salvage its future by clambering over the still-warm but dying body of capitalism in Europe. It's not easy being Green? Kermit the frog did not know the half of it…

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia