Germany’s IFO Shows Recovery

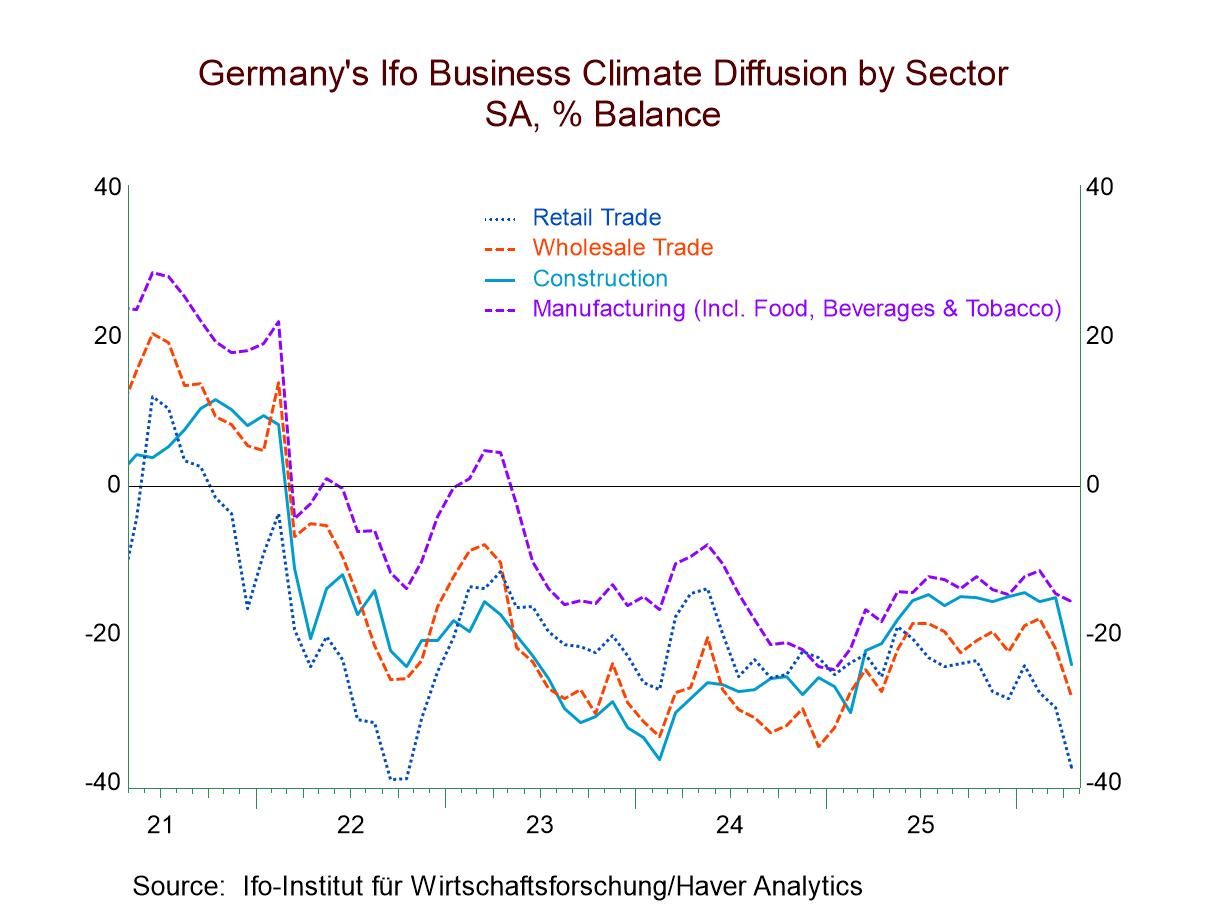

Germany's all sector climate index improved in March to -19.8 from -24 in February. Still, the index only has a 13.9 percentile standing on data back to the early 1990s. The all-sector climate index, the current index and expectations all improve month-to-month with the scope of improvement for the all-sector climate and expectations indexes greater only about 10% of the time. These are sharp month-to-month improvements. However, the levels of the indexes are so weak that the rankings continue to scrape very low levels. Overall conditions in Germany have hardly changed despite the solid month-to-month improvement concentrated in climate and expectations.

Climate The climate measure shows improvements for the all-sector reading, manufacturing, construction wholesaling, retailing, and services. The highest percentile standing for any sector is for construction at a below-median 41.5 percentile standing. The next highest standing is for retailing at a 24.5 percentile standing, the weakest reading is a standing of 10.3% in manufacturing, and the services sector is at a 13.2 percentile standing, not too much stronger than that.

Transition-Ho! While climate conditions are still in difficult straits, we find that current conditions standings are largely worse than for climate standings; expectations show uneven comparisons. We know there are big changes coming to Europe, particularly for Germany, because of the new shift to more defense spending. This, obviously, will create improvements in the defense sector but should also have broader multiplier effects for the economy, for the manufacturing sector, but also for the economy in general. We also expect these changes to spread across Europe with similar increases in military spending to be introduced in other countries, as the United States is looking for Europe to carry more of its own security burden. We should continue to see improvements in expectations and in climate in the coming months and those improvements should be translated gradually into improved current conditions as well.

Current conditions-Manufacturing and Construction lead Current conditions in the index show improvement across all sectors with minuscule improvements being posted in wholesaling and in retailing in March. The percentile standing for the current indexes in March show the strongest reading in construction; it is the only sector above its median: above its 50th percentile at 61.6%, with retailing close to its 50th percentile mark at 48.2%. The weakest readings are for manufacturing at an 11.9 percentile standing and then services at a 16.9 percentile standing. But manufacturing has the largest month-to-month gain. The overall standing for current conditions is lower still at its 10.7 percentile standing, indicating a confluence of weakness across sectors, a result that has the overall index at a weaker standing than any for individual sector.

Expectations – Manufacturing surges Expectations show broad improvement and for the most part fairly significant improvement across sectors. The headline improvement shows expectations at -16.1 in March compared to -20.5 in February, which leaves the index at a 16.9 percentile standing overall. Expectation standings are weak, however, with the strongest expectation standing in manufacturing at 21.1%, the second strongest for wholesaling at 19.8%; services rank third with the standing of 15.1%. Construction, the sector that has the strongest current and climate standings, has the weakest expectation-standing at the 8.2 percentile mark.

Summing up and looking ahead These readings begin to pick up some of the changes in progress with expectations showing still very weak current readings but substantial pickups month-to-month. However, most of this is simply expectations improving; it is not expectations built on actually better performance and jumping off from there, as we can see from the fact that the current indexes or the most part are not much changed month-to-month, with extremely little change in wholesaling and retailing. Still, both of those current/expectations reading are higher; manufacturing is also improved in the current reading but expectations are leading the way ahead, improving faster, not the other way around. German transactors are beginning to look to the future recognizing there is a change afoot on military spending that is going to permeate the economy and we're beginning to see that in different aspects of the IFO survey. Stay tuned and stay alert.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia