Global| Jan 05 2023

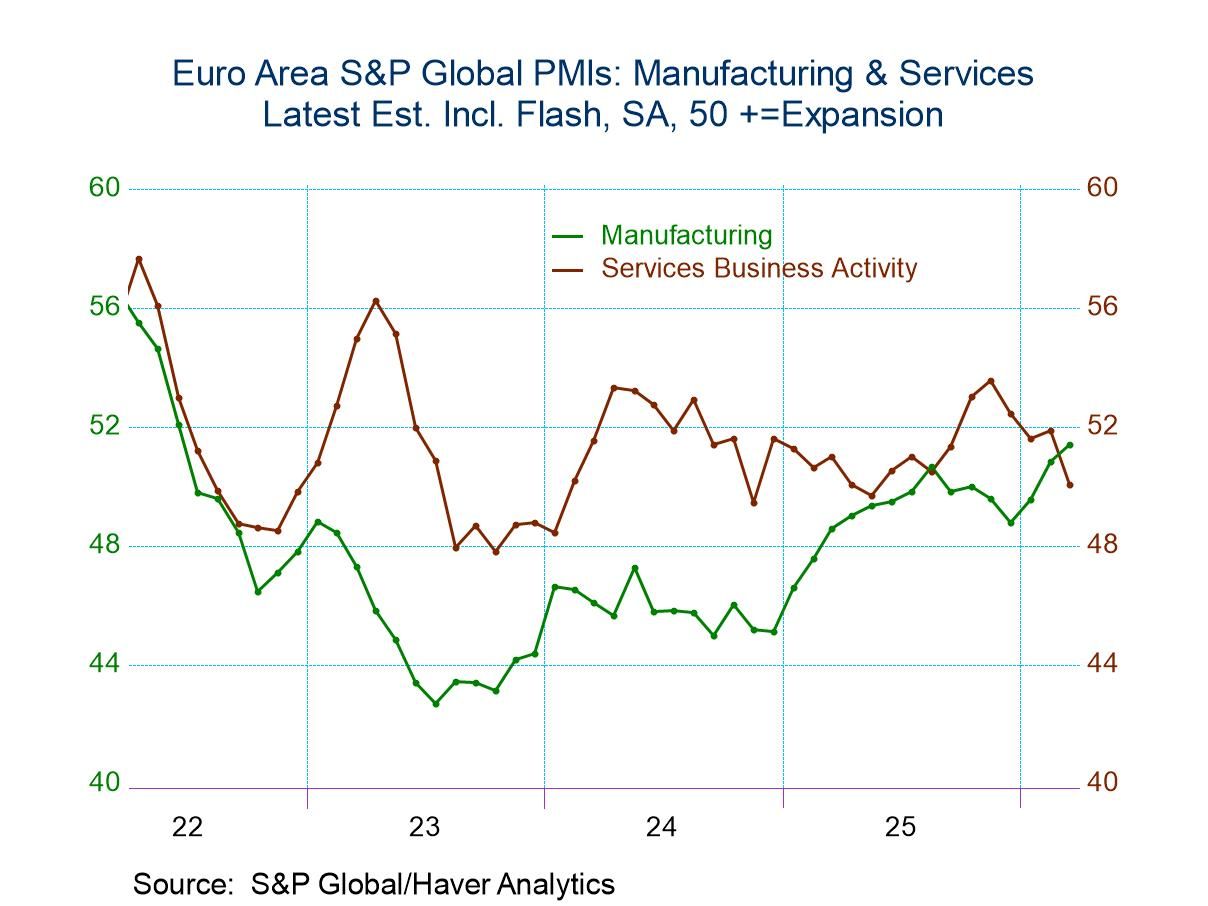

Global| Jan 05 2023Global Composite PMIs Erode or Show Contraction

The global S&P composite PMIs for December generally show weakness and declining momentum. In December, 9 jurisdictions show weakening composite PMIs compared to the month before (out of a sample of 22). Sixteen of these jurisdictions have composite PMI readings below 50 that indicate overall activity is eroding. The number showing month-to-month slowing has been diminishing from 15 in October to 11 in November to 9 in December; that's some improvement in terms of the breadth of jurisdictions reporting weakening month-to-month activity. However, the number of jurisdictions below 50, indicating outright contraction, remains high at 16 in December, the same as in November. And that number accounts for more than half of the reporters.

Large vs small country observations- In fact the count in this table is not weighted for economy-size and a quick glance at the table will show that the larger economies are showing a pronounced tendency to be below 50 and to decline month-to-month. The tendency to decline month-to-month has abated slightly in December among the larger economies (among G7 countries only France and the US erode month-to-month in December). Among G7 countries all have composite PMI readings below 50 in December, November and October save a reading of 51.8 in October for Japan (Japan has not yet reported for December, but was below 50 in November). The G6 percentile standings in December average 19%-weaker than the full sample average and median.

Thick as a bric? - The US, the UK, and the European Monetary Union have PMI readings that stand below the 20% mark in their historic queues for the last 4 1/2 years they average a standing at their 12 ½ % mark of their respective distributions. For now the BRIC countries are doing better than this, they have a 61.6 percentile standing in their historic queue (for this reading I exclude Russia) and this leaves them with readings that are above their historic medians. However, the average and median percentile standings for all members is reading is in the 20th percentile (27.3% Avg, 21.4% median) indicating significantly weak readings. Of the 22 readings in the table in fact, ten (of 22) have queue percentile standings below their 20th percentile.

More broadly... Looking at broader data over three-months, six-months, and 12 months we see more consistent readings concerning weakness and the breadth of slowing. On this smoothed basis the breadth of slowing has actually grown over the recent three months and the number of jurisdictions with an average reading below 50 over 3-months is 14, the same as it was over six-months and both of those numbers are much worse than what they reported on 12 month averages. Neither is that surprising since averaging below 50 over 12 months is an extremely weak condition.

Economic Landscape- The economic conditions for the global economy have not changed much. What that means is that inflation continues to be overshooting on a broad and significant scale. Central banks have been raising interest rates and they are continuing to raise interest rates with markets unsure where the end point for the rate hikes will lie. While inflation is overheating there are some indications that the escalation of inflation has stopped and there is some backtracking particularly based upon oil prices and commodity prices. But so far the backtracking is minor and episodic compared to the strong readings in the gauges that central banks focus on and target. And, in a recently released central bank report of commentary by central bank officials in the US, there were no members on the Federal Open Market Committee (FOMC) – no members among 18- who saw any interest rate reductions by the Federal Reserve in the year ahead.

War continues, with supply chain, fiscal, and geopolitical impact- The Russia Ukraine war continues full tilt and that continues to absorb a great deal of resources from the countries that are backing Ukraine while the war continues to be a great drain on the Russian economy that is also laboring under the weight of sanctions imposed by Western countries over Russia having instigated that war. However, and ominously, as that war drags on there's evidence of dissent within Western nations, not so much among their leaders, but within the countries among various political factions that the spending on the war is becoming increasingly unpopular. This development, of course, could encourage Russia to continue to fight even as its losing if it thinks that in the long run it can break the will of the Western countries that are supporting Ukraine. It’s a dangerous situation.

Energy- The global energy situation remains strained particularly with the United States focused on green policies and refusing to pump more oil even though it is an oil rich country while in Europe there has been some backtracking on green agendas because of the extreme strain that Europe is under and its need for energy since the Russian pipelines have been turned off. The US is helping US oil to pump more in Venezuela where some of the most sulfur-intensive, heavy oil, is found. This does not seem very ‘green’ to me… These conditions continue to be central to the way policy is run in Western countries. With China ending its zero Covid policy there is some concern that global energy demand could be rising and could strain prices again.

Policy candor? - Increasingly policymakers, even among central bank members, are talking more frankly and openly about the prospect for some sort of recession this year although this talk is quickly diverted to the topic of how any recession is likely to be moderate.

Central bankers on the hot-seat- Central bankers are having a hard time coming to grips with the fact that they played inflation very badly under Covid and it is greatly out of control because of their inattention and poor decisions. However, central banks still want to be seen as having credibility and the backbone to fight inflation and a desire to reduce it back to their target in an expeditious fashion. And while they are quite clear in stating that goal, they are much more wishy washy when it comes to explaining how they're going to get that job done. As central banks look at the future, they are far less willing to talk about doing ‘whatever it takes’ and much more prone to talk about taking some specific steps that they then argue are going to be sufficient while they worry about doing too much and about the impact on the economy. This sort of mixed-mouth mumbling does not instill faith among people in markets that the central banks have the will to achieve the objective that they claim they intend to achieve.

What markets expect... or handicap- Despite these lingering questions about central bank credibility and their backbones, markets seem to be handicapping that a less aggressive policy from the Federal Reserve in the United States will have a more pronounced economic impact. Markets see more rate cutting and sooner Fed rate cutting than the Federal Reserve is mapping out in its the so-called dot plot that provides some forward guidance on where policy is going. However, it's not clear that this is because markets think that (1) Fed policy is going to be more effective in bringing inflation down or (2) whether markets think that Fed policy is going to have a larger impact in bringing the economy down or, (3) whether markets simply view the central bank as having less of a backbone and being unwilling to continue to raise or hold rates even if inflation remains excessive once the unemployment rate begins to rise.

The future- All of this means that the future is still very much up in the air. Much of what we see going on in the world with central banks raising rates keys off of what the Fed has done and how it began to raise rates in March of last year. Most of the turbulence in global markets stems from that event. Clearly what the Fed does with policy is going to be a linchpin for the rest of the world and right now there doesn't seem to be a very clear view of what that policy will be even in the face of the Fed providing us with what it would call “guidance” and markets basically rejecting that. Remember that two years ago Federal Reserve’s “guidance" would have projected inflation around 2% and any Federal Reserve member confronted with what is now the reality of inflation would have denied the possibility of this ever occurring. Yet it has occurred. And the Fed has yet to provide us with any credible statements as to how this happened on its watch and why we should not be worried that it could happen again. Nor has the Fed said with conviction that it is prepared to do ‘what’s necessary’ to bring inflation to heel ‘quickly.’ We have gone down the rabbit hole, and it’s a different world in this wonderland than the one Paul Volcker lived in. The dual mandate lives, and both prongs of the mandate are equally important…except one prong may be more equal than the other. Once the central bank does what Volcker refused to do- take responsibility for unemployment in the short run- we are in a different realm. Your anti-inflation Fed decoder ring no longer works here. Just pat attention to what the Fed says and that is clear…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief