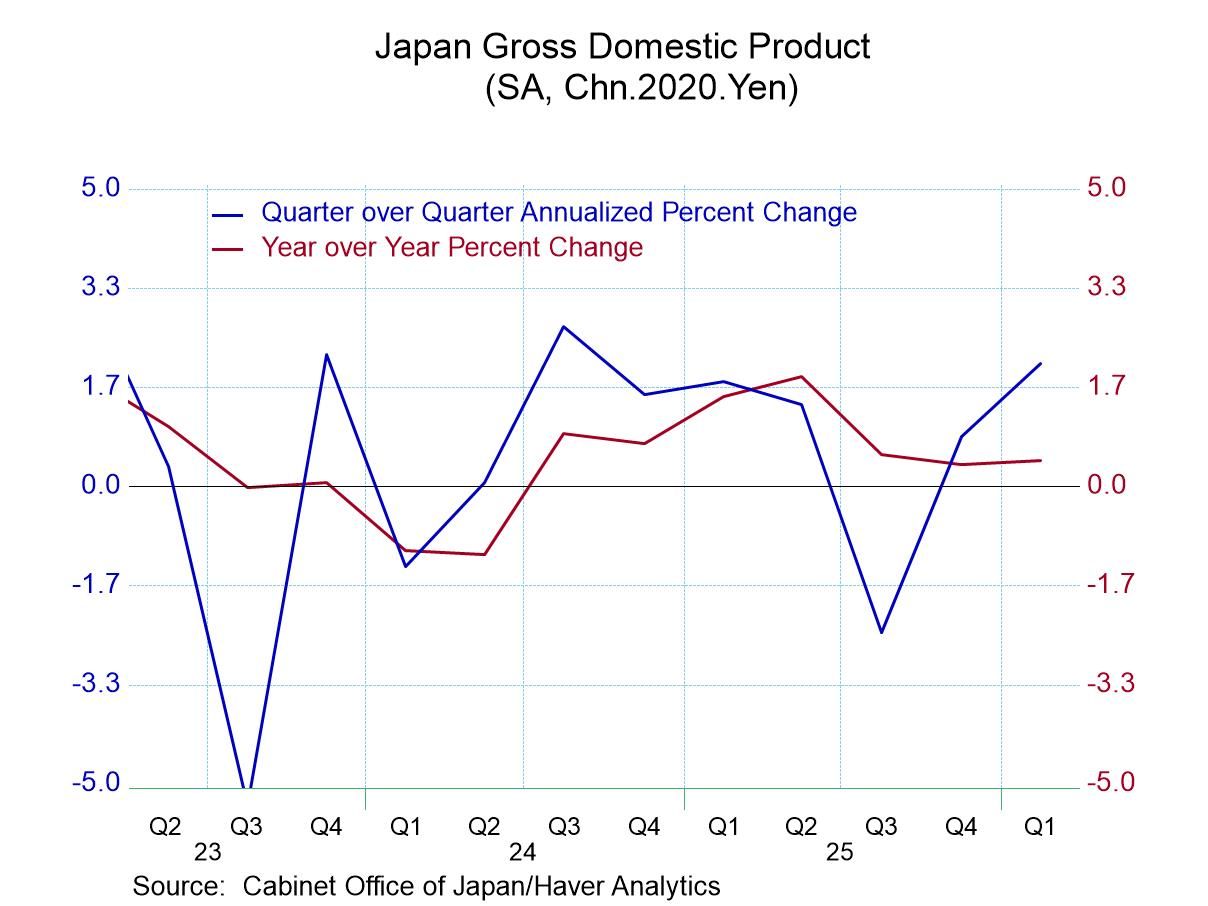

Japan’s Tertiary Sector Recovers in a Trend-dominated Report

Japan's tertiary index (service sector index) recovered in July, rising to 101.8 from 100.9 in June after it had reached 101.6 in May. The July recovery brings the index of tertiary sector activity up above its May level and leaves it with a relatively high year-over-year ranking of its growth rate’s top 10 percentile standing on data since 2011. In contrast, industry stepped back to an index reading of 103.8 in July from 105.7 in June. The July value is still above its May value, but the sector’s growth ranking has it in its 20.5 percentile, approximately the lower one-fifth of its historic level by ranking. The industry index is 4.6% below its level in January 2020 before COVID struck; the tertiary index is higher by only 0.2% since COVID struck. These two sector indexes have been either weak or lethargic over this 3½ year period.

Economy watchers indexes deliver a more upbeat reading; these diffusion indexes in July are all above 50 indicating expansion for the overall index and for the individual sectors the Economy watches index assesses. In July, the headline improved and most components improved, except for eating & drinking places and the overall metric for the services sector slipped to 57.5 in July from 60.7 in June but this reading still registers sector expansion. The economy watchers indexes have a growth ranking, for the most part, in the 80th to 90th percentile, the exception being a weaker ranking for employment growth.

The Teikoku readings are also diffusion indexes; they indicate more weakness than the economy watchers survey. Manufacturing, retailing, wholesaling, and construction all have readings below the 50% mark indicating weakening growth. Services post a 51.7 diffusion reading, a reading that improves relative to June and indicates sector expansion. The growth ranking on the Teikoku indexes has manufacturing below its historic median for growth. Retailing and services have rankings above their respective 80th percentiles, marking them as relatively strong in terms of momentum.

It is not surprising to have these somewhat sensitive diffusion indexes giving us slightly different perspectives on what's going on in the various sectors. This month the good news from the METI sector indexes is for services improving and that's important because services are the employment generating sector; the employment growth ranking in the economy watchers framework is the relative weakest barometer among the various sector assessments in that survey.

The chart of the METI indexes for services and industry shows that not much has changed in the Japanese economy of late. The tertiary (services) index has continued to plug along somewhat sluggishly while the industry reading (mining and manufacturing) has been more volatile in a narrow range; it is currently riding a down cycle. But everything in the table for the month seems to be a reading in the normal flow of recent trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia