Global| Jan 24 2024

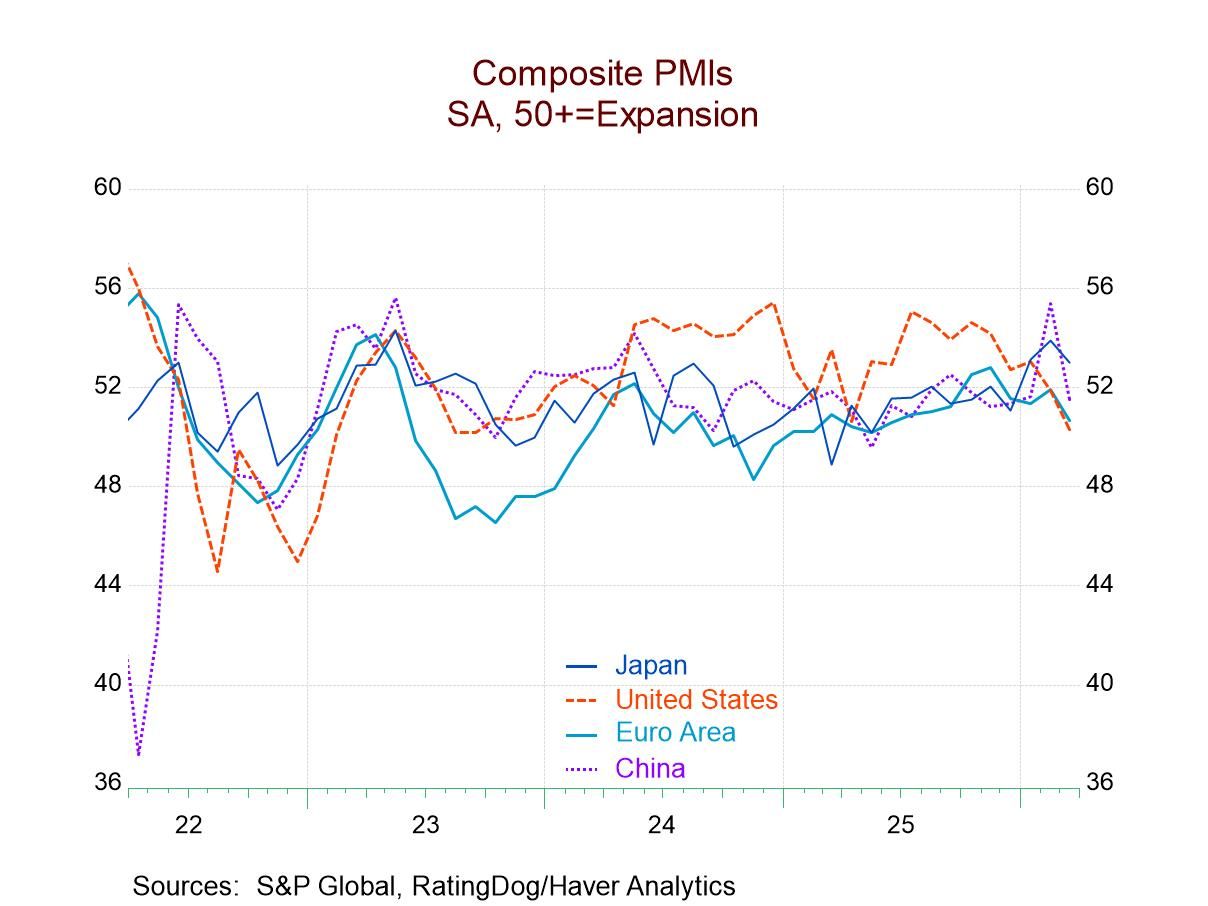

Global| Jan 24 2024S&P Flash MFG PMIs

The chart is for the European Monetary Union and there we see relative stability for services activity as manufacturing is turning higher. Turning to the table we see most of the responses- that means 10 out of 16 responses- show conditions in manufacturing or for services or for the composite, improving rather than weakening in January 2024. December also showed a strong move towards strengthening compared to weakening, especially against the history of the recent past. December also showed 10 metrics strengthening and only six weakening.

Beginning with this report our history for comparison moves up to January 2020 instead of to January 2019. On this timeline, the January 2024 values for the PMI responses in the table show only three above the 50% mark which means there are only three that have PMI standings above their median for this period.

Despite the slight improving tone in this report, it's quite clear that the changes and these PMI metrics back to January 2020 show that all but six of them are still lower than they were at that time - a significant span of four years. That's a long time for PMI gauges to not have improved.

With this improvement in January, on the heels of improvement in December, we now have over three months improvement across the board with only four exceptions. The exceptions are France where the service sector deteriorates and drags the composite down as well. The service sector in Germany weakens over three months and the manufacturing sector in Japan does so too.

On balance, over three months we're seeing improvements occur in the European Monetary Union, the aggregate index is up by 1.3 points, pushed strongly ahead by an improvement in manufacturing of 3.5 points, while services sector only creeps higher during this period rising by 0.5 points. The U.K. shows improvement on all gauged in each of the last three months – a power-house response and the strongest composite gain over three months in the table.

Seeing recovery in-train is good news. However, we must wonder if the current geopolitical issues resulting in closure of the Suez Canal are going to have adverse effects on economic growth and costs because of transportation difficulties in the period ahead. Inflation rates have settled down. And with the PMI data showing that growth statistics that had been moving sideways at weak to slightly contracting level for some time, are strengthening, would be a very positive development if it would last. Inflation data have improved as well with central banks still well-above the targets that they've imposed on themselves for inflation, but still having brought inflation rates down substantially from their recent overshoots.

The question is whether central banks are going to be able to corral inflation back within their target or whether central banks are going to be content letting inflation cruise some distance above the targets to nourish growth. In the U.S., at least, I'm suspicious that that's what the phrase “soft landing" really means. What it means is that there will be no landing for the economy because there will be no recession. But does it also mean that the central bank is willing to turn a blind eye to ongoing inflation overshoots because the overshoots are not severe enough? It's too soon to know if that's the case. It will take some time to figure out whether this was a wise move by central bankers, or a deal made with the devil.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.