Global| Mar 01 2023

Global| Mar 01 2023S&P Global MFG PMIs Contract on Balance But It’s More of a Mixed Bag

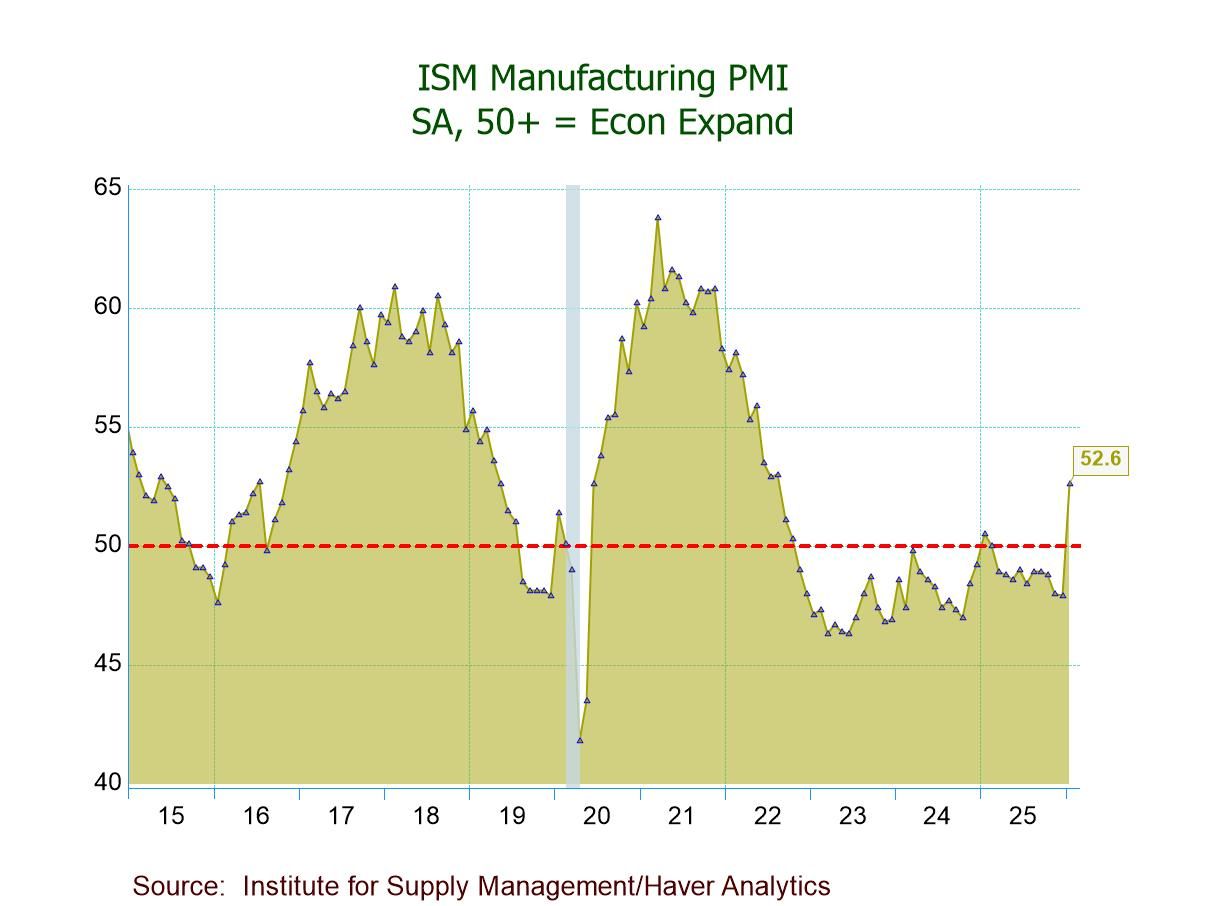

S&P manufacturing PMIs for February show a much more mixed bag than in previous months. Of the 18 reporting entities in February, 11 improve month to month. So, on a country count, there are more improvements than deteriorations. However, looking at the median level month-to-month, it is still lingering below ‘50’ indicating contraction in the lexicon of diffusion indexes - even though the median value does improve slightly month-to-month. As I noted, a mixed bag.

Sequential data also show complicated trends. The average PMI for manufacturing over three months is slightly better than over six months but only by a tick comparing 48.5 to 48.4. That's still showing a sector decline in terms of PMI diffusion index values. Over six months only 5 reporters show improvement compared to 12-month values. There is net deterioration over 12 months where there are only 5 reporters out of 18 that improve compared to 12-months ago.

Despite the slight firming on the month, there is continued contraction in manufacturing being reported although the contraction being reported is quite small. Still, the median queue standing that evaluates the current month has a standing compared to where it's been since 2019 at its 37th percentile. On that timeline back to January 2019, only six of 18 entries show percentile standings above their historic medians. On that span, the median is marked by a 50-percentile standing. Oddly - and interestingly- China and Russia both claim 98 percentile standings on the period, the highest in the group. Part of that is a reflection of how weak they have been.

The changes since COVID arrived, back to January 2020 levels, show there are eight reporting regions that have current manufacturing PMI values above their January 2020 levels: that’s over a span of three years. There's been very little growth overall as the median change has been a decline of 0.2 in the median PMI index.

Asian reporters in the table have fared better than the whole group overall. They log an average PMI value of 50 in February and sequential averages from 12-months, to six-months, to three-months show a progression higher. Their percentile standing at the 48th percentile is higher than the median for the group. China’s improvement and exit from a zero Covid strategy is helping.

Table 1

Table 2 provides some pooled information on the distribution of manufacturing PMI values and recent months as well as over different periods giving some historic context. The proportion of entries in what I regard as the neutral expansion area, between PMI values of 50 and 55, increased in February to 38.9% from January’s 33.3%. Those are both sharply higher than December's 16.7% in that category. The bulk of reporters still cluster in the first tier of contracting PMI signals which I put in the cohort from 40 to just less than 50. In February that shrank to 55.6% of the reporters from 61.1% in January and 77.8% in December.

There has been a gradual movement of reporters from the first tier of declining output into the neutral zone, but no countries in the last three months reporting anything in lower PMI tiers (nothing below a PMI of 40). Meanwhile, reporters in the upper tier from 55 to 60 diffusion values have been steady at just 5.6% of total reporters.

These distributional numbers tell us that everything is pretty much clustered around the middle. There aren't any countries that are extremely strong or extremely weak. The bulk of the reporters are showing moderate contraction although there's been a slow migration from modern contraction into moderate normalcy.

The February report is an improvement from what we've been seeing, and we do see 61% of the reporters improve month-to-month a little less than the 72% that improved month-to-month in January, but better than the 44% that reported improving month-to-month in December.

Over three months 72% of the reporters are improving compared to six-months. Over six months 44% are improving compared to 12-months, whereas over 12 months only 27.8% improved compared to 12-months ago. There is a progression of improvement underway. However, it's not clear if this improvement is episodic or if it's going to have legs.

Table 2

The policy outlook is…complicated Globally inflation remains high; central banks are still worried about inflation and determined to fight it. The emergence of economic strength, in fact, becomes a problem for central banks since inflation is persisting. While I don't want to portray central banks as anti-growth since they are trying to push inflation back down, it's very hard to do that if growth is accelerating so that puts bankers in a tough spot. Central banks clearly are put in a quandary by these developments and in my view, it raises the upside risks that we're going to see more interest rate hikes than what we had been expecting earlier.

We're back in the situation where good news may be bad news, at least for those who are crafting investment strategies that are centered on interest rate developments and expected interest rate developments. The key thing for central banks is to get inflation to behave and that's not happening… and growth is accelerating. It looks like it's not going to happen unless central banks take some added steps that were not expected. That's the risk that's put on the table in February.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief