U.K. Inflation Takes a Breather that Is Not Likely to Last

U.K. inflation rose by 0.5% in May after rising by 1.9% in April and 1.0% in March. Inflation acceleration was far less common in May with inflation accelerating in only 18% of the categories. In April inflation had accelerated in only 36% of the categories. That compares to March when inflation had accelerated in over half the categories with the diffusion value 54.5%. Despite seemingly tamer performance of inflation, inflation continues to rise and to accelerate from 12-months to six-months to three-months. Core inflation also broke lower in May at 0.3%; in April it was up by 0.5% but in March it had risen by 0.8%.

If we look at sequential trends, the U.K. headline CPIH rose 7.9% over 12 months, and at a 10.2% pace over six months, and logged a 14.4% pace over three months. The CPIH, excluding energy, food, alcoholic beverages & tobacco - the core measure, rose 5.2% over 12 months, at a 5.9% annual rate over six months, and at a 6.4% annual rate over three months. Inflation in the U.K. is accelerating over these sequential periods.

U.K. inflation is clearly excessive, but the Bank of England has prevaricated in taking firmer steps perhaps partly because of this less broad inflation in April and on the lower gain for inflation in May. But the Bank of England is still well behind the inflation curve, like the U.S. Federal Reserve and like the European Central Bank. Central banks need to get out ahead of the inflation problem and not chase it from behind, and become complacent when there's some sign that inflation might be slowing ‘organically.’ Central banks have come to dwell on the idea that they don't want to create a recession and that possibly they can create a soft landing. However, they are all so far behind the curve in terms of inflation fighting; it's hard to see how they can run hard enough to catch up without doing damage to the economic landscape.

Inflation diffusion over three months is at 63.6% - that means inflation is accelerating in about 63% of the categories, diffusion is at 72.7% over six months and it's at 90.9% over 12 months. Inflation clearly is accelerating and accelerating broadly. There is nothing half baked about the rise in the inflation rate and there really is nothing here suggesting it's going to settle down on its own even though there were some encouraging lower numbers for May with the core rising by only 0.3%. That probably reflects transitory phenomenon. Surveys show their inflation expectations are high as a kite.

Inflation expecations as well as inflation are high in the U.K. That all but assures that monetray policy is going to have to mount a major attack to conquer the problem. Soft landings are much less feasible when hard inflation is expected.

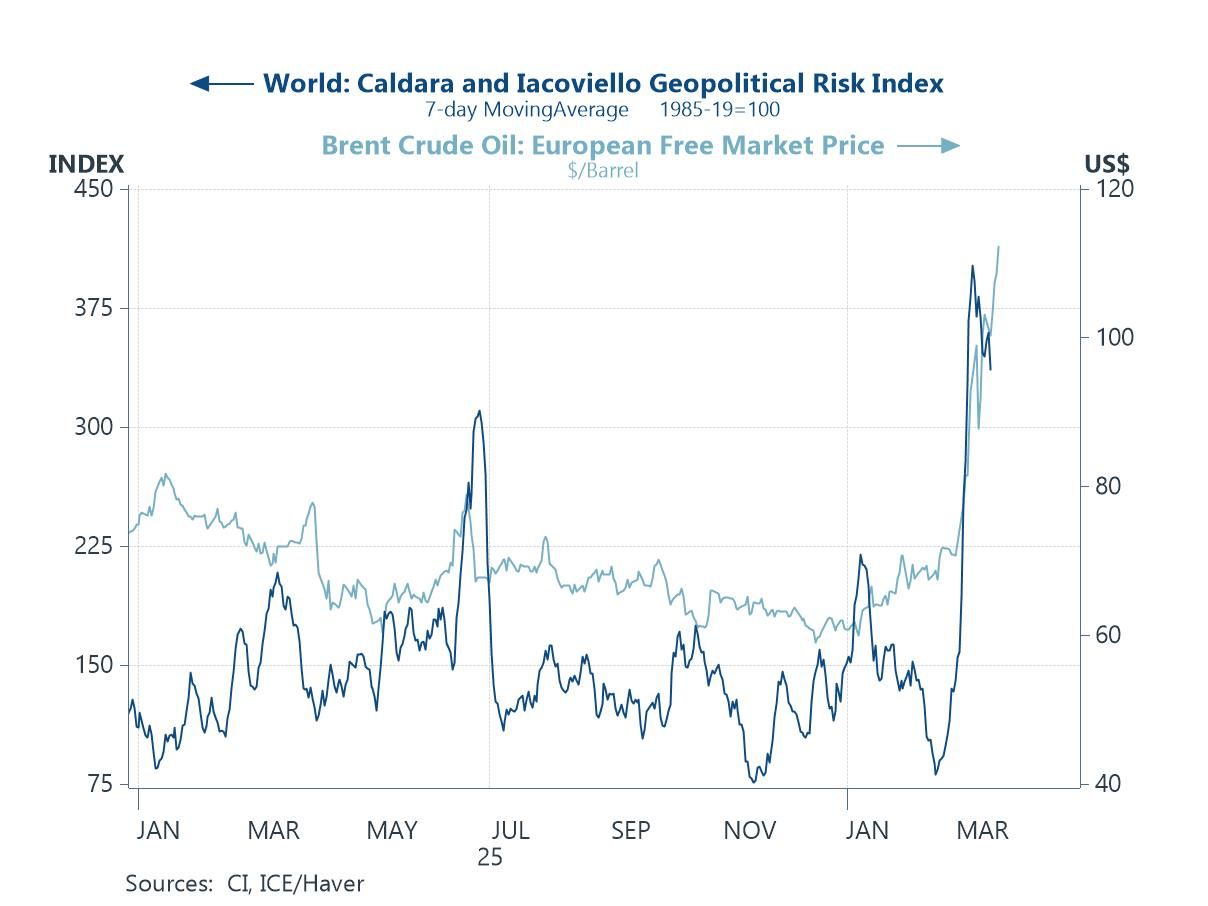

Global risiska are still very much afoot. A war between Ukraine and Russia is adding to inflation fires for food and energy, for select minerals, and especially for fertilizers. There's no telling when this is going to stop. The war continues to look like it is going to be long-lived with Russia at long last focusing its advantage much more narrowly and bringing its firepower to bear with superior weaponry over a smaller more intensely attacked battlefield. The West still hasn't given Ukraine what it needs to bring this battle to parity and it's not clear that the West will do so or if it will do so in time. There was a new escalation in the war this past week, with Lithuania not allowing sanctioned goods to transship from the Russian ports in the Baltic across its terrirory into Belarus and into Russia. This is creating new tensions and new threats from Russia.

The U.K. unemployment rate continues low in the economy. The economy still seems to be operating fairly well. However, with inflation so high and the central bank coming to get ahold of it, I would not expect growth continue to perform well in the months ahead. Central bankers have a problem and will have to use interest rates to knock inflation down. Consumers have been used to low interest rates for too long; everybody talks about how consumers have liquidity and good balance sheets. It isn't going to take much in the way of rising unemployment, and rising interest rates to change peoples’ assessments of where consumers stand. Once a recession gets going, the game changes and things never look exactly the way that they had looked before the recession began. In the United States, one recession signal has already turned on: that is one that I derive from the Philadelphia Fed’s manufacturing survey. That signal has forecasted every natural recession since the late 1960s (the Covid-recession did not register) and it has never predicted recession that did not occur. So it would seem to be a fairly reliable signal. As the U.S. goes into recession, it would be hard to find that the U.K. and Europe would not be far behind.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia