Global| May 16 2006

Global| May 16 2006Housing Starts Lowest Since 2004

by:Tom Moeller

|in:Economy in Brief

Summary

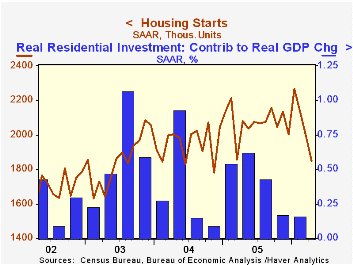

During April, housing starts fell 7.4% m/m to 1.849M units following the 6.4% March decline that was revised slightly shallower. Again, the decline by far exceeded Consensus expectations for a modest drop to 1.95M starts and reduced [...]

During April, housing starts fell 7.4% m/m to 1.849M units following the 6.4% March decline that was revised slightly shallower. Again, the decline by far exceeded Consensus expectations for a modest drop to 1.95M starts and reduced the number of starts to the lowest level since November 2004.

Since the peak this past January, total starts have fallen 18.4%.

Single-family starts dropped 5.6% to 1.535M units and added to the 10.3% March decline. The latest level is down 15.4% from the January peak and is the lowest since November 2004.

By region, single family housing starts were quite mixed last month. Starts in the South fell 15.9% m/m to a level that was off 19.9% from the January peak. In the West starts fell a moderate 3.6% but that added to the 19.1% slide in March and pulled the latest level down 22.0% from the February peak. In the Midwest single family starts moved in the opposite direction and reversed the prior month's decline with a 21.4% (+3.2% y/y) gain. In the Northeast starts also recovered the prior month's down draft and rose 6.7% though starts were still 17.7% off the January peak.

Multi family starts reversed the sharp March increase with a 15.1% decline to the lowest level since March of last years.

Building permits dropped by 5.4% for the third consecutive monthly decline and are off 10.7% from the peak last September.

| Housing Starts (000s, AR) | April | Mar | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total | 1,849 | 1,996 | -11.1% | 2,073 | 1,950 | 1,854 |

| Single-family | 1,535 | 1,626 | -8.6% | 1,719 | 1,604 | 1,505 |

| Multi-family | 314 | 370 | -21.3% | 354 | 345 | 349 |

| Building Permits | 1,984 | 2,097 | -8.0% | 2,144 | 2,057 | 1,8 88 |

by Tom Moeller May 16, 2006

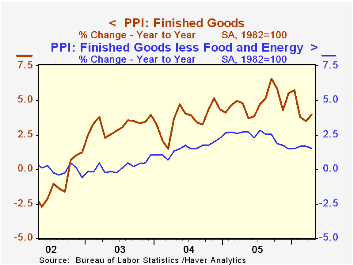

The April finished goods producer price index jumped 0.9%. That was the largest gain since a 1.4% spike last September but it about matched Consensus expectations had been for a 0.8% rise.

Less food & energy the (core) PPI increased 0.1% last month and fell short of expectations for a 0.2% rise. Durable consumer goods prices were unchanged (0.3% y/y) following two months of 0.1% increase and core consumer nondurable prices rose 0.1% (2.6% y/y) following three months of stronger gain. Apparel prices continued lower. Prices of all finished consumer goods less food & energy rose 0.1% (1.6% y/y).

Capital equipment prices rose 0.2% (1.4% y/y) after two months of 0.1% gains.

Finished energy prices jumped 4.0% (17.8% y/y) as gasoline prices increased 12.3% (33.9% y/y) and home heating oil rose 13.7% (27.6% y/y). A 3.0% decline in natural gas prices (+12.4% y/y) was the third consecutive monthly drop.

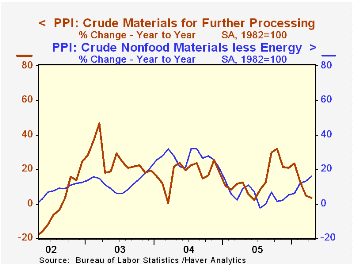

Intermediate goods prices jumped 0.9% on higher energy prices which rose 2.8% (18.4% y/y). Core intermediate prices increased 0.4%.

Crude goods prices regained about half of the prior month's decline with a 1.2% increase. Energy prices rose 1.3% higher crude oil prices were offset by lower prices for natural gas. Core crude prices, however, were notably strong and posted a 4.7% gain and are up 8.4% year to date. Copper base scrap (59.1% y/y), aluminum scrap (28.7% y/y) and iron & steel scrap (8.7% y/y) all continued strong. During the last thirty years "core" crude prices have been a fair indicator of industrial sector activity with a 48% correlation between the six month change in core crude prices and the change in factory sector industrial production.

| Producer Price Index | April | Mar | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Finished Goods | 0.9% | 0.5% | 4.0% | 4.9% | 3.6% | 3.2% |

| Core | 0.1% | 0.1% | 1.5% | 2.4% | 1.5% | 0.2% |

| Intermediate Goods | 0.9% | -0.1% | 7.3% | 8.0% | 6.6% | 4.7% |

| Core | 0.4% | 0.1% | 4.9% | 5.5% | 5.7% | 2.0% |

| Crude Goods | 1.2% | -2.7% | 3.3% | 14.6% | 17.5% | 25.1% |

| Core | 4.7% | 0.8% | 16.0% | 4.8% | 26.5% | 12.4% |

by Tom Moeller May 16, 2006

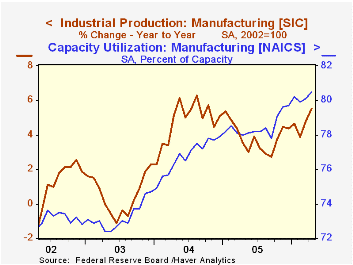

Total industrial output jumped 0.8% last month following two months of 0.5% gain. Consensus expectations had been for another 0.5% increase.

Factory sector output surged 0.8% (5.5% y/y) after an unrevised 0.5% March increase. That increase matched a 0.8% January spike and lifted the y/y gain in factory output to its highest since in over a year.

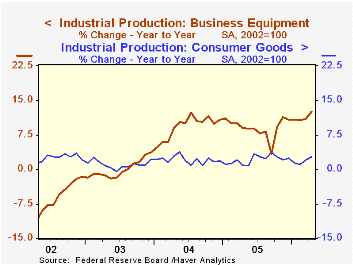

A 1.7% (12.4% y/y) rise in business equipment output provided umph to last month's gain in output as output of computers, communication equipment and semiconductors jumped 2.4% (21.7% y/y). Factory output excluding high tech, however, also was strong and rose 0.7% (4.6% y/y).

Output of nondurable consumer goods rose 0.4% (2.1% y/y) as appliance & furniture output rose 0.2% (4.0% y/y). Automotive products' production fell 1.1% (+4.2% y/y). Excluding motor vehicles and high tech factory output increased 0.9% (4.7% y/y).

Output of primary metals jumped 1.2% (6.7% y/y) following two months of decline and fabricated metals output rose 0.5% (6.1% y/y).

Total capacity utilization surged to 81.9%, the highest level since July of 2000. Factory sector utilization rose to 80.5%, also its highest level since 2000. During the last twenty years there has been a 36% correlation between the level of factory sector utilization and the y/y change in "core" producer prices. There also has been a 37% correlation with the change in core consumer prices.

Industrial capacity grew 0.1% (1.9% y/y) and the annual rate of growth is up from 1.3% last year and 0.3% during 2004. Factor sector capacity grew 0.2% (2.3% y/y) compared to 1.6% growth last year and 0.2% growth during 2004. Much of that growth has been in the high tech sector. Excluding high tech, factory sector capacity is up 1.0% y/y.

The 1990s Acceleration in Labor Productivity: Causes and Measurement from the Federal Reserve Bank of St. Louis can be found here.

| Production & Capacity | April | Mar | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Industrial Production | 0.8% | 0.6% | 4.8% | 3.2% | 4.1% | 0.6% |

| Manufacturing | 0.8% | 0.5% | 5.5% | 3.9% | 4.8% | 0.5% |

| Consumer Goods | 0.2% | 0.8% | 2.7% | 2.1% | 2.1% | 1.0% |

| Business Equipment | 1.7% | 0.7% | 12.4% | 9.1% | 9.3% | 0.0% |

| Capacity Utilization | 81.9% | 81.4% | 79.7% (4/05) | 80.1% | 78.6% | 75.7% |

by Louise Curley May 16, 2006

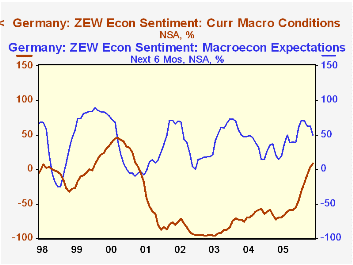

German investors and analysts, who report to the ZEW Center for European Economic Research, have become less optimistic regarding the economic outlook over the next six months. The excess of those expecting better conditions over those expecting worsening conditions dropped sharply from 62.7% in April to 50.0% in May. It is, however, still above the historical average of 35.3%. The consensus had expected a more modest drop. There has been a steady erosion of confidence since January when the percent balance reached 71.1%.

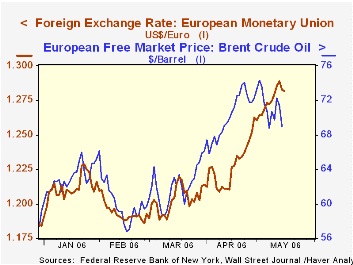

At the same time, the excess of those German investors and analysts who rate current conditions as "good" over those who rate them "bad" rose from 2.9% in April to 8.7% in May. These two ratings were the first positive ratings since April 2001. They may have reflected the improvement in the economy as measured by the 0.04% increase in GDP in the first quarter of this year, up from 0.01% in the fourth quarter of 2005. From the beginning of the this year until April, the price of a barrel of oil had remained below $66 and the euro had ranged in a fairly narrow band between $1.19 and $1.23. Investor expectations and appraisals of current conditions are shown in the first chart.

Since then, however, the price of oil has spiked up to more than $74 a barrel and the euro has climbed to $1.29. (See the second chart.) The threat to German exports from a higher euro and the impact of higher oil prices on consumer demand have, no doubt, made investors and analysts more cautious.

| Germany: ZEW | May 06 | Apr 06 | May 05 | M/M dif | Y/Y dif | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|---|

| Expectations | 50.0 | 62.7 | 13.9 | -12.7 | 36.1 | 34.8 | 44.6 | 38.4 |

| Current conditions | 8.7 | 2.9 | -69.3 | 5.8 | 78.0 | -61.8 | -67.7 | -92.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates