Global| May 19 2006

Global| May 19 2006Philadelphia Fed Business Activity Up

by:Tom Moeller

|in:Economy in Brief

Summary

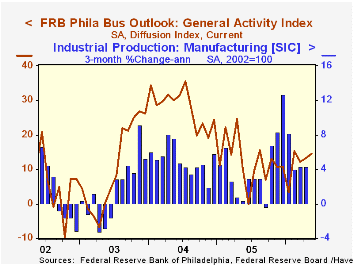

The May Index of General Business Conditions in the manufacturing sector from the Philadelphia Fed rose modestly, for the second month, to 14.4 from an unrevised 13.2 last month. The gain surpassed Consensus expectations for a decline [...]

The May Index of General Business Conditions in the manufacturing sector from the Philadelphia Fed rose modestly, for the second month, to 14.4 from an unrevised 13.2 last month. The gain surpassed Consensus expectations for a decline to 12.5.

During the last ten years there has been a 65% correlation between the level of the Philadelphia Fed Business Conditions Index and three month growth in factory sector industrial production. There has been a 49% correlation with q/q growth in real GDP.

The index reflected improvement in delivery times and inventories. However, declines in other sub indexes were broad based; new orders, shipments and employment each fell to the lowest levels since last Summer. During the last ten years there has been a 75% correlation between the employment index and the three month growth in factory payrolls.

The business conditions index reflects a separate survey question, not the sub indexes.

The prices paid index surged to the highest level since last September. During the last ten years there has been a 76% correlation between the prices paid index and the three month growth in the intermediate goods PPI. There has been an 85% correlation with the change in core intermediate goods prices.

The separate index of expected business conditions in six months fell and reversed roughly half of the improvement in April. Expectations for employment fell sharply to the lowest level since August 2002..

The latest Business Outlook survey from the Philadelphia Federal Reserve Bank can be found here.

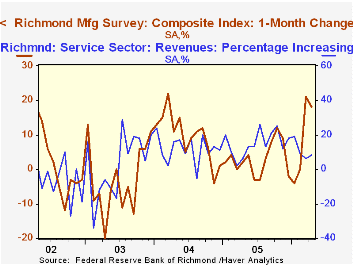

The rise in the Philly Fed index ran counter to the m/m improvement, reported Monday, in the May Empire State Manufacturing index of general business conditions. The Richmond Fed will report its May Mfg. Survey index next week. The reading will follow two months of sharp improvement, notably in orders, shipments and jobs and the figures will be available in the Haver SURVEYS database.

During the last ten years there has been a 57% correlation between the Richmond survey index level and the change in factory sector industrial production, nationally. The latest Richmond Fed Mfg. Survey is available here.

The Richmond Fed also publishes indexes of conditions in the Service Sector and the latest release is available here.

| Philadelphia Fed Business Outlook | May | April | May '05 | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| General Activity Index | 14.4 | 13.2 | 10.3 | 12.4 | 28.0 | 10.5 |

| Prices Paid Index | 55.3 | 29.0 | 32.0 | 43.5 | 51.2 | 16.8 |

by Tom Moeller May 19, 2006

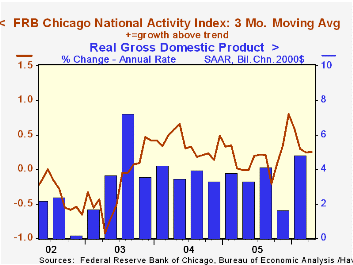

The National Activity Index (CFNAI) from the Federal Reserve Bank of Chicago improved during April on the prior month's recovery. It rose to 0.38 from 0.35 and a 1Q average of 0.24.

The three-month moving average of the CFNAI rose to 0.25 from 0.24 the prior month.

A zero value of the CFNAI indicates that the economy is expanding at its historical trend rate of growth and during the last twenty years there has been a 68% correlation between the level of the CFNAI and q/q growth in real GDP.

The CFNAI is a weighted average of 85 indicators of economic activity. The indicators reflect activity in the following categories: production and income, the labor market, personal consumption and housing, manufacturing and trade sales, and inventories & orders.

The latest CFNAI report is available here.

The Evolving Nature of the Financial System: Financial Crises and the Role of the Central Bank, yesterday's speech from the newly designated Vice Chairman of the Federal Reserve Board Donald L. Kohn, is available here.

| Chicago Fed | April | Mar | April '05 | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| CFNAI | 0.38 | 0.35 | 0.06 | 0.20 | 0.37 | -0.11 |

by Carol Stone May 19, 2006

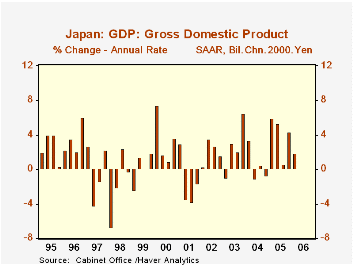

Japan's GDP surprised on the upside for Q1, in data reported today by the Japanese Cabinet Office. It expanded at a 1.9% annual rate. While this was less than Q4's 4.3%, it well exceeded forecasters' views that anticipated about 1.2%. The yen gained briefly on the report.

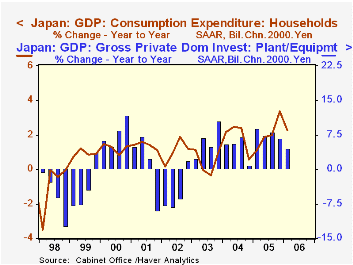

Notably, the driving force in the growth was private domestic demand, led by business investment. This component had fallen in Q4 and rebounded sharply in Q1, at a 5.8% annual rate. That put it 4.6% ahead of a year ago. Household consumption moderated from Q4, increasing at a 1.6% annual pace relative to 2.6% in Q4. Together, private domestic demand grew 3.2% on the quarter (annualized) and was also up 3.2% from a year ago.

Also of significance, growth of exports slowed from Q4's large 16.2% to "just" 11.3%. At the same time, imports switched from a modest decline in Q4 to a 12.6% rate of increase. Exports are substantially larger than imports, so these adverse moves did not keep the net export surplus from increasing, although the rise was very modest: only ¥308 million on a base of ¥18.1 billion.

Markets were encouraged that the domestic economy appears to be picking up steam. The price deflator is still falling, however, although this may be due in the most recent period by the surge in imported energy costs. The deflator for domestic demand is holding just about even with year-earlier levels. With these price signals still mixed, Bank of Japan officials remain skittish about whether the economy could stand higher borrowing costs; when they issued a statement to this effect later today, FX traders pushed the yen back down once again.

| Chain GDP % Chg, Annual Rates* |

Q1 2006 | Q4 2005 | Q3 2005 | Year/ Year | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| GDP | 1.9 | 4.3 | 0.6 | 3.1 | 2.6 | 2.3 | 1.8 |

| Household Consumption | 1.6 | 2.6 | 1.8 | 1.2 | 1.7 | 0.6 | 1.0 |

| Government Consumption | 0.6 | 0.4 | 2.0 | 0.8 | 1.7 | 2.0 | 2.3 |

| Private Plant & Equipment | 5.8 | -0.9 | 5.2 | 4.6 | 7.7 | 4.9 | 5.9 |

| Exports | 11.3 | 16.2 | 12.9 | 13.7 | 7.0 | 13.9 | 9.0 |

| Imports | 12.6 | -2.5 | 13.3 | 8.0 | 6.3 | 8.5 | 3.0 |

| Private Domestic Demand | 3.2 | 3.0 | -0.0 | 3.2 | 3.2 | 2.2 | 1.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates