Global| Apr 30 2019

Global| Apr 30 2019The Great EMU Deceleration Ends?

Summary

Year-over-year GDP growth had decelerated in five consecutive quarters until the Q1 2019 release. And even in 2019, it is not posting a trend-stopping rise, but rather a rate of growth equal to that in the previous quarter when [...]

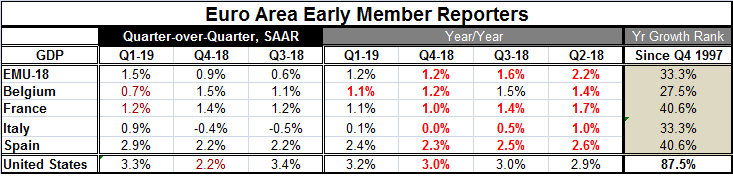

Year-over-year GDP growth had decelerated in five consecutive quarters until the Q1 2019 release. And even in 2019, it is not posting a trend-stopping rise, but rather a rate of growth equal to that in the previous quarter when expressed as a year-over-year rate of growth. Of course, quarter-to-quarter EMU GDP growth did pick up, rising to a 1.5% pace (annualized) in Q1 from a 0.9% pace in Q4. Growth also accelerated quarter-to-quarter in Italy where the recession, a mild two quarter wonder is ended if you deemed two modest quarterly declines in a row a recession in the first place (probably not). France and Belgium each logged GDP rises on a quarterly basis that are weaker than the previous quarter. But France still manages a slight GDP acceleration year-over-year (up to a 1.1% pace from a 1.0% pace in Q4) while Belgium's pace slides again on a year-over-year basis.

Year-over-year GDP growth had decelerated in five consecutive quarters until the Q1 2019 release. And even in 2019, it is not posting a trend-stopping rise, but rather a rate of growth equal to that in the previous quarter when expressed as a year-over-year rate of growth. Of course, quarter-to-quarter EMU GDP growth did pick up, rising to a 1.5% pace (annualized) in Q1 from a 0.9% pace in Q4. Growth also accelerated quarter-to-quarter in Italy where the recession, a mild two quarter wonder is ended if you deemed two modest quarterly declines in a row a recession in the first place (probably not). France and Belgium each logged GDP rises on a quarterly basis that are weaker than the previous quarter. But France still manages a slight GDP acceleration year-over-year (up to a 1.1% pace from a 1.0% pace in Q4) while Belgium's pace slides again on a year-over-year basis.

While the EMU is breaking out of a five quarter deceleration in GDP growth, the U.S. has a 10 quarter streak of year-over-year growth rates either accelerating or holding pace with the previous quarter. Despite the huge-seeming difference in these periods, over that 10 quarter span the U.S. economy advanced by 8.7% in real terms while the EMU advanced by 7.4%.

However, the U.S. is growing much better relative to its historic norm than the EMU, based on the year-over-year growth rates in Q1 2019. The U.S. rate sits in the 87.5 percentile queue of its ordered queue of growth rates over that span. In contrast, the EMU's 1.2% gain stands only in its 33.3 percentile, at the border of the bottom one-third of its historic queue of ranked rates of growth. No other country in the table does much better than Spain and France with their 40th percentile standings. Italy has a 33.3 percentile standing and Belgium has a 27.5 percentile standing. GDP growth in the EMU is positive, but it is still feeble.

The graphic at the top of this report shows that the Markit composite PMI has traced GDP growth rate change relatively well. Its more timely data seem to point to some further weakness in GDP growth and then a period of leveling off if the PMI signal continues to hold where it has been in the last few months.

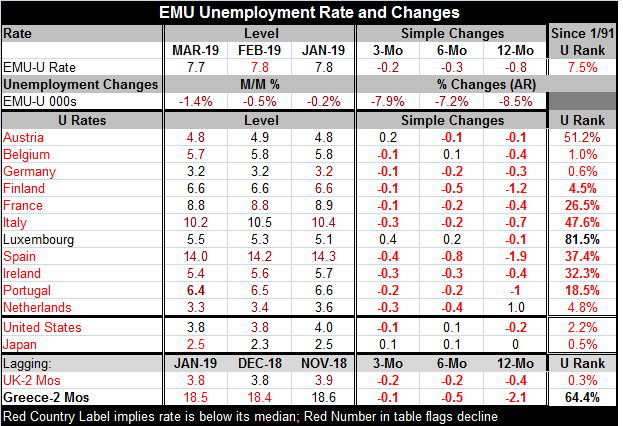

Only two of the topically reporting early EMU members Luxembourg and Greece have unemployment rates above their historic medians. Luxembourg is a financial center and Greece actually is still seeing some relatively rapid unemployment rate drops and its data lag by two months.

Of the 12-reproting EMU members (I include Greece here), the differences in the levels of unemployment are remarkable. Spain's unemployment rate has been this low or lower only 37% of the time and it stands at 14.0% in March. But Ireland's rate stands at 5.4% and it has been this low or lower 32.3% of the time. The two countries have essentially the same relative standings but vastly different levels of unemployment. This is true up and down the line. While the standard deviation for the unemployment rates among this group of countries is as low as it has ever been since 2008, the difference – the structural difference- among the members remains huge.

A correlation on the ranking of countries according to the historic standing of these unemployment rates vs. the absolute levels of unemployment we gets an R-squared of only 0.15; that is the difference in the levels of the unemployment rates only explains about 15% of the differences in the historic standings for each.

This illustrates how rigidities in the euro area persist even after years together in the monetary union and in the customs union where rules have tried to harmonize so much that the U.K. bolted calling the rules too intrusive. And such differences persist even after the discipline imposed on some members by austerity. Clearly, whatever harmonization has wrought, it has fallen short of putting everyone on the same, or on an even, playing field.

Such continuing differences in the unemployment rates tell of poor labor market integration and poor overall economic integration. We know that each worker in each country prefers his or her own culture. But even though many Europeans speak more than one language, too few are willing to live elsewhere to force unemployment rates to a common level. Moreover, such differences in unemployment rates speak of very different levels of labor availability and yet capital does not move to arbitrage away that difference either. Apparently, investment does not move freely enough either.

As a result of such circumstances, we should be mindful always that while the ECB does make a one size fits all monetary policy the actual policy will not be optimal across all members. With this in mind, it explains a lot about why the upcoming Europeans elections are going to be so fractious. Different people want different things from the EU. Many are upset at the choices made by past elected representatives and then foisted on member nations. The EMU and EU many, many, years after their formation remain works in progress.

Meanwhile unemployment progress continues to be made

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates